Market Equilibrium - 2 - Free MCQ Practice Test with solutions, UPSC Indian

MCQ Practice Test & Solutions: Test: Market Equilibrium - 2 (20 Questions)

You can prepare effectively for UPSC Indian Economy for UPSC CSE with this dedicated MCQ Practice Test (available with solutions) on the important topic of "Test: Market Equilibrium - 2". These 20 questions have been designed by the experts with the latest curriculum of UPSC 2026, to help you master the concept.

Test Highlights:

- - Format: Multiple Choice Questions (MCQ)

- - Duration: 20 minutes

- - Number of Questions: 20

Sign up on EduRev for free to attempt this test and track your preparation progress.

Detailed Solution: Question 1

The factor that causes a change in quantity demanded is

The factor that causes a change in quantity supplied is

Detailed Solution: Question 8

A rise in the price of the complementary good leads to

Detailed Solution: Question 9

Detailed Solution: Question 10

A fall in the price of the good for a seller leads to

Detailed Solution: Question 11

Detailed Solution: Question 12

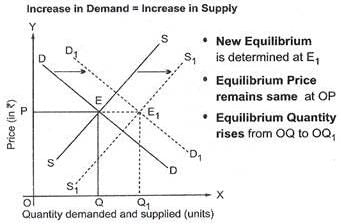

Market for a good is in equilibrium. An increase in demand for the good will

Detailed Solution: Question 13

Market for a good is in equilibrium. A decrease in demand for the good will

Market for a good is in equilibrium. An increase in supply for the good will

Detailed Solution: Question 15

Market for a good is in equilibrium. A decrease in supply for the good will

Detailed Solution: Question 16

Market for a good is in equilibrium. An increase in demand for the good will

Detailed Solution: Question 17

Market for a good is in equilibrium. An increase in supply for the good will

Market for a good is in equilibrium. An increase in the price of the good will

Detailed Solution: Question 19

Market for a good is in equilibrium. A decrease in price for the good will

Detailed Solution: Question 20

136 videos|428 docs|127 tests |