Test: Introduction To Microeconomics - 3 - CA Foundation MCQ

30 Questions MCQ Test - Test: Introduction To Microeconomics - 3

The capital that is consumed by an economy or a firm in the production process is known as

| 1 Crore+ students have signed up on EduRev. Have you? Download the App |

Who expressed the view that “Economics is neutral between end”?

Which of the following is the best general definition of the study of Economics?

What implications) does resource scarcity have for the satisfaction of wants?

What is the “Fundamental Premise of Economics”?

Which of the following is a normative statement?

Which of the following statements would you consider to be a normative one?

An example of ‘positive’ economic analysis would be :

A study of how increases in the corporate income tax rate will affect the national unemployment rate is an example of

Which of the following does not suggest a macro approach for India?

Economic goods are considered scarce resources because they

From the national point of view which of the following indicates micro approach?

In a free market economy the allocation or resources is determined by

A capitalist economy uses ____________________ as the principal means of allocating resources.

In a free market economy, when consumers increase their purchase of a good and the level of ________________exceeds ______________ then prices tend to rise.

Which of the following would be considered a disadvantage of allocating resources using a market system?

The central problem in economics is that of

If the PPF is linear, i.e., a straight line, which of the following is true?

Periods of less than full employment correspond to

Which of the following would not result in an rightward shift of the PPF?

During presidential election campaigns, candidates often promise both more “gun” and more “butter” if they are elected. Assuming unemployment is not a problem, what possible assumption are they making but not revealing to their audience?

What is one of the future consequences of an increase in the current level of consumption in the India?

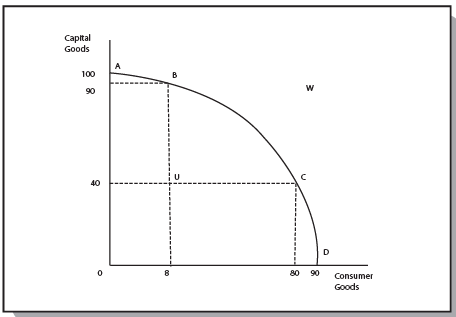

(Direction 27 - 33) Use the figure at right to answer questions.

Q. Which of the following represents the concept of trade-offs?

Q. Which of the following would not move the PPF for this economy closer to point W?

Q. Moving from point A to point D, what happens to the opportunity cost of producing each additional unit of consumer goods?

Q. What is the opportunity cost of moving from point A to point B?

Top Courses for CA Foundation

Important Questions for Introduction To Microeconomics - 3

Introduction To Microeconomics - 3 MCQs with Answers

Online Tests for Introduction To Microeconomics - 3

|

© EduRev

|

Education Revolution

|

|