Test: Sale Of Goods On Approval Or Return Basis - 1 - CA Foundation MCQ

30 Questions MCQ Test - Test: Sale Of Goods On Approval Or Return Basis - 1

When a large number of articles are sent on a sale or return basis, It is necessary to maintain:

A sent some goods costing Rs. 3500 at a profit of 25% on sale to B on sale or return basis. B returned goods costing Rs. 800. At the end of year, the remaining goods were neither returned nor were approved by him. The stock on approval will be shown in balance sheet at:

| 1 Crore+ students have signed up on EduRev. Have you? Download the App |

On 31st December, 2011 goods sold at a sale price of Rs. 30,000 were lying with customer, Mohan to whom these goods were sold on ‘approval or return basis’ and recorded as actual sales. Since no consent was received from Mohan, the adjustment entry was made presuming goods were sent on approval at a profit of cost plus 20%. In the balance sheet, the Inventories with customer account will be shown at Rs.

Under sales on return or approval basis, when transactions are few and the seller at the end of the accounting year reverse the sale entry, then what will be the accounting treatment for the goods returned by the customers on a subsequent date?

At what price goods lying with customer’s are valued at year ending under sale of approval basis:

Under sales on return or approval basis, the ownership of goods is passed only

Sale or Return Day Book and Sale or Return Ledger are known as

A company sends its cars to dealers on ‘sale or return’ basis. All such transactions are however treated like actual sales and are passed through the sales day book. Just before the end of the financial year, two cars which had cost Rs. 55,000 each have been sent on ‘sale or return’ and have been debited to customers at Rs. 75,000 each, cost of goods lying with the customers will be

A company sells motor bikes on “Sale or return basis”. All such transactions are however treated like actual sales and are passed through the sales book. Just before the end of the financial year, two motor bikes costing Rs. 55,000 each have been sent on “Sale or Return basis” and have been debited to customers at Rs. 75,000 each, cost of goods lying with the customers will be:

A merchant sends out his goods casually to his dealers on approval basis. All such transactions are, however, recorded as actual sales and are passed through the sales book. On 31-12-2011, it was found that 100 articles at a sale price of 200 each sent on approval basis were recorded as actual sales at that price. The sale price was made at cost plus 25%. The amount of stock on approval will be amounting

When the goods are returned by the customers within the specified time, they are recorded

What is the objective behind selling goods on approval basis:

Cash Sale of Rs. 50,000, Credit Sale of Rs. 3,50,000, Sales Return Rs. 25,000 out of Sales of Rs. 3,50,000, goods costing Rs. 40,000 were sent ton approval for Rs. 50,000 which has not been approved yet. Calculate the net sales:

Sales = Rs. 1,06,000

Sales Return = Rs. 6,000

Out of Rs. 1,06,000 goods costing Rs. 10,000 were sent on approval for Rs. 12,000 which have not been approved yet. Calculate Net Sales.

Mr. X sends the goods costing Rs. 55,000 on approval basis. Goods of Rs. 5,000 were damaged in transit and claim of Rs. 3,000 was received. The amount of goods sent on approval to Mr. Y is :-

A trader has credited certain items of sales on approval aggregating Rs. 60,000 to Sales Account. Of these, goods of the value of Rs. 16,000 have been returned and taken into Inventories at cost Rs. 8,000 though the record of return was omitted in the accounts. In respect of another parcel of Rs. 12,000 (cost being Rs. 6,000) the period of approval did not expire on the closing date. Cost of goods lying with customers should be

Sale or return day book is a :

In case of sale of goods on approval basis, the sale will take place under which of the following cases ?

When a large number of articles are sent frequently on a sale or return basis, it is necessary to maintain

Which method is used for “Sale on Approval” basis when the transactions are few in nature?

Goods costing Rs. 1,00,000 sent to customer on sales or return basis at a price of cost plus 30% . During the year 50% of the good have been accepted. 30% of the goods returned and the balance goods were lying with customer at year end and the specified time limit for approval is yet to expire. Amount of total stock to be shown in the balance sheet would be:

Under sales on return on approval basis, when transactions are few, the seller, while sending the goods, treats them as

Total sales of Star Limited for the year ended 31st March 2008 was Rs. 5,00,000, which includes goods sold to R for Rs. 5,500 at a profit of 10% on cost. Such goods are still lying in the Godown of Star Limited at the buyer’s risk. In the books of Star Limited sales would be shown as :-

Which of the following is not a main column of sales or return journal?

X sent some goods costing Rs. 3,500 at a profit 20% on sales or approval basis. Y returned goods costing Rs. 800. At the end of the year 2013 the remaining goods were neither returned nor approved. The closing stock to be shown in Balance Sheet will be:

12 Memorandum records of sale on approval is a part of :

A sent some goods costing Rs. 3,500 at a profit of 25% on sale to B on sale or return basis. B returned goods costing Rs. 800. At the end of the accounting period i.e. on 31st December, 2011, the remaining goods were neither returned nor were approved by him. The Inventories on approval will be shown in the balance sheet at Rs.

A trader sends out goods is customer on approval and credits them to sales amount. On 31st March, 2011, sundry debtors includes an amount of Rs. 5,000 for goods sent on approval basis for which no confirmation was received till year end. These goods were sent out at a cost +25%. Physical stock taken on 31st March, 2011 amounted to Rs. 50,000. The amount of stock appearing is Balance Sheet would be:

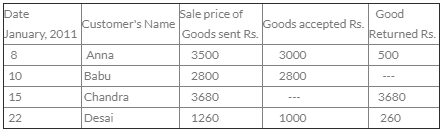

Umesh sends goods on approval basis as follows:

The Inventories of goods sent on approval basis on 31st January will be

Top Courses for CA Foundation

Important Questions for Sale Of Goods On Approval Or Return Basis - 1

Sale Of Goods On Approval Or Return Basis - 1 MCQs with Answers

Online Tests for Sale Of Goods On Approval Or Return Basis - 1

|

© EduRev

|

Education Revolution

|

|