NABARD Manager Full Length Mock Test 10 - Bank Exams MCQ

30 Questions MCQ Test Mock Tests for Banking Exams 2024 - NABARD Manager Full Length Mock Test 10

For the two given equations I and II.

I. p2 + 5p + 6 = 0

II. q2 + 3q + 2 = 0

II. q2 + 3q + 2 = 0

For the two given equations I and II.

I. p2 = 4

II. q2 + 4q = - 4

II. q2 + 4q = - 4

| 1 Crore+ students have signed up on EduRev. Have you? Download the App |

Consider a circle with unit radius. There are seven adjacent sectors ,S1,S2,S3 ,.... S1,. in the circle such that their total area is 1818 of the area of the circle .Further ,the area of the jth sector is twice that of the (j-1) th sector ,for j = 2.....7. What is the angle ,in radians, subtented by the arc of S1 at the centre of the circle ?

which is equal to

which is equal to

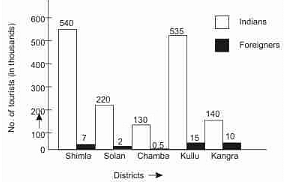

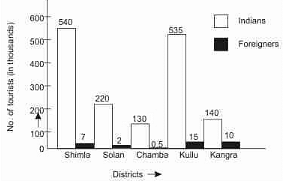

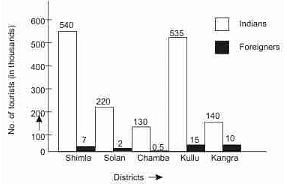

Study the following graph carefuly and answer the questions given below it.

Q. How many districts in Himachal Pradesh were visitedby more than 10% of the total Indian tourists ?

= 156.5 thousand

= 156.5 thousandStudy the following graph carefuly and answer the questions given below it.

Q. By what percentage the Indian tourists visiting Chamba were less than those visiting Shimla ?

Study the following graph carefuly and answer the questions given below it.

Q. Approximately what percentage was shared by total foreign tourists among all the tourists visiting Himachal Pradesh ?

In a mixture of 60 litres, the ratio of milk and water is 2:1. If the ratio of the milk and water is to be 1:2,then the amount of water to be further added is

Choose the correct alternative that will continue the same pattern and fill in the blank.

8, 43, 11, 41, __, 39, 17

Choose the correct alternative that will continue the same pattern and fill in the blank.

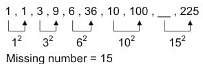

1, 1, 3, 9, 6, 36, 10, 100, (....), 225

Choose the correct alternative that will continue the same pattern and fill in the blank.

3, 8, 13, 24, 41, (....)

A bag contains 600 pens of brand A and 1200 pens of brand B.If 12% of brand A pens and 25% of brand B pens are removed,then what is the approximate percentage of total pens removed from the bag?Options

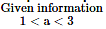

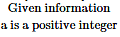

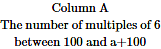

The information and quantities in column-A and column-B are given below.

Compare the quantities.

The information and quantities in column A and column B are given below.

Compare the quantities.

The information and quantities in column-A and column-B are given below.

Compare the quantities.

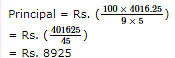

A sum fetched a total simple interest of Rs. 4016.25 at the rate of 9 p.c.p.a. in 5 years. What is the sum?

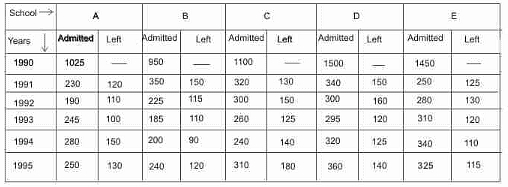

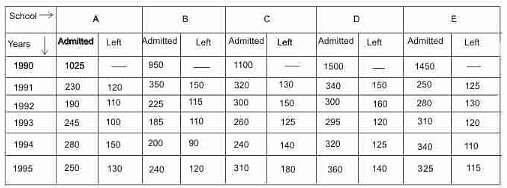

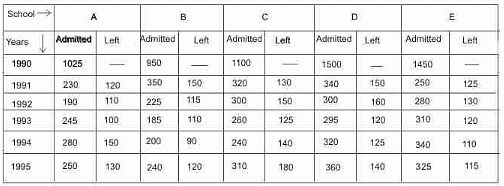

Read the following information carefully and answer the questions based on it.

In 6 educational years, number of students taking admission and leaving from the 5 different school which are founded in 1990 are given below

Q. What is the average number of students studying in all the five schools in 1992 ?

Read the following information carefully and answer the questions based on it.

In 6 educational years, number of students taking admission and leaving from the 5 different school which are founded in 1990 are given below

Q. What was the number of students studying in School B in 1994 ?

Read the following information carefully and answer the questions based on it.

In 6 educational years, number of students taking admission and leaving from the 5 different school which are founded in 1990 are given below

Q. Number of students leaving School C from the year 1990 to 1995 is approximately what percentage of number of students taking admission in the same second and in the same year ?

Three machines, individually, can do a certain job in 4,5 and 6 hours, respectively. What is the greatest part of the job that can be done in one hour by two of the machines working together at their respective rates?

of the job in one hour

of the job in one hourIn a mixture of 60 litres, the ratio of milk and water is 2:1. If the ratio of the milk and water is to be 1:2,then the amount of water to be further added isOptions

In these questions, relationships between different elements is shown in the statements. These statements are followed by two conclusions.

Give answer (1) if only conclusion I follows.

Give answer (2) if only conclusion II follows.

Give answer (3) if either conclusion I or conclusion II follows.

Give answer (4) if neither conclusion I nor conclusion II follows.

Give answer (5) if both conclusions I and II follow.

21. Statements :N ≥ O ≥ P = Q > R

Conclusions :

I. N > R

II. R = N

In these questions, relationships between different elements is shown in the statements. These statements are followed by two conclusions.

Give answer (1) if only conclusion I follows.

Give answer (2) if only conclusion II follows.

Give answer (3) if either conclusion I or conclusion II follows.

Give answer (4) if neither conclusion I nor conclusion II follows.

Give answer (5) if both conclusions I and II follow.

Statements : W ≤ X < Y = Z > A; W < B

Conclusions :

I. B > Z

II. W < A

In these questions, relationships between different elements is shown in the statements. These statements are followed by two conclusions.

Give answer (1) if only conclusion I follows.

Give answer (2) if only conclusion II follows.

Give answer (3) if either conclusion I or conclusion II follows.

Give answer (4) if neither conclusion I nor conclusion II follows.

Give answer (5) if both conclusions I and II follow.

Statements : H > I > J > K; L < M < K

Conclusions :

I. I > M

II. L < H

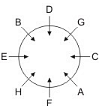

Eight friends A, B, C, D, E, F, G and H are sitting around a circle (not necessarily in the same order) facing the centre.

- B sits third to left of F.

- E is an immediate neighbour of both B and H. Only one person sits between A and H.

- C and G are immediate neighbours of each other. Neither C nor G is an immediate neighbour of B.

- Only one person sits between C and D.

Q. Who amongst the following is an immediate neighbour of both A and H ?

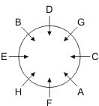

Eight friends A, B, C, D, E, F, G and H are sitting around a circle (not necessarily in the same order) facing the centre.

- B sits third to left of F.

- E is an immediate neighbour of both B and H. Only one person sits between A and H.

- C and G are immediate neighbours of each other. Neither C nor G is an immediate neighbour of B.

- Only one person sits between C and D.

Q. 'F' is related to 'D' in a certain way based on the seating positions in the given arrangement. Similarly 'C' is related to 'E' in the same way. To whom amongst the following is 'H' related to following the same pattern ?

Eight friends A, B, C, D, E, F, G and H are sitting around a circle (not necessarily in the same order) facing the centre.

- B sits third to left of F.

- E is an immediate neighbour of both B and H. Only one person sits between A and H.

- C and G are immediate neighbours of each other. Neither C nor G is an immediate neighbour of B.

- Only one person sits between C and D.

Q. Which of the following represents the correct position of A ?

Each question below consists of two statements numbered I and II . You have to decide whether the data provided in the statements are sufficient to answer the questions.

Give answer (1) if the statement I alone is sufficient to answer the question, but the statement II alone is not sufficient.

Give answer (2) if the statement II alone is sufficient to answer the question, but the statement I alone is not sufficient.

Give answer (3) if both statements I and II together are needed to answer the question.

Give answer (4) if either the statement I alone or statement II alone is sufficient to answer the question.

Give answer (5) if you cannot get the answer from the statement I and II together, but need even more data.

Q. Is the child holding a yellow coloured flower?

I. When the thorn of the flower pricked his finger, the colour of the blood matched that of the flower.

II. The child is carrying a rose in his hand.

Each question below consists of two statements numbered I and II . You have to decide whether the data provided in the statements are sufficient to answer the questions.

Give answer (1) if the statement I alone is sufficient to answer the question, but the statement II alone is not sufficient.

Give answer (2) if the statement II alone is sufficient to answer the question, but the statement I alone is not sufficient.

Give answer (3) if both statements I and II together are needed to answer the question.

Give answer (4) if either the statement I alone or statement II alone is sufficient to answer the question.

Give answer (5) if you cannot get the answer from the statement I and II together, but need even more data.

Q. Who among M, N, P and R is facing North?

I. Only one among the four faces North.

II. M and N face West while P is facing South.

Each question below consists of two statements numbered I and II . You have to decide whether the data provided in the statements are sufficient to answer the questions.

Give answer (1) if the statement I alone is sufficient to answer the question, but the statement II alone is not sufficient.

Give answer (2) if the statement II alone is sufficient to answer the question, but the statement I alone is not sufficient.

Give answer (3) if both statements I and II together are needed to answer the question.

Give answer (4) if either the statement I alone or statement II alone is sufficient to answer the question.

Give answer (5) if you cannot get the answer from the statement I and II together, but need even more data.

Q. Is it afternoon in Delhi?

I. The weather is bright, humid and hot in Delhi.

II. Thirteen hours ago it was midnight in Delhi.

Five girls are sitting on a bench to be photographed. Seema is to the left of Rani and to the right of Bindu. Mary is to the right of Rani. Reeta is between Rani and Mary.

Q. Who is sitting immediate right to Reeta ?

|

160 tests

|

Important Questions for NABARD Manager Full Length Mock Test 10

NABARD Manager Full Length Mock Test 10 MCQs with Answers

Online Tests for NABARD Manager Full Length Mock Test 10 Mock Tests for Banking Exams 2024

|

© EduRev

|

Education Revolution

|

Follow Us

|