Test: Meaning And Scope Of Accounting - 1 - Commerce MCQ

30 Questions MCQ Test Accountancy Class 11 - Test: Meaning And Scope Of Accounting - 1

Interpreting Financial Statements means:

Net Profit or Loss will be derived at ________ stage of accounting.

| 1 Crore+ students have signed up on EduRev. Have you? Download the App |

On January 1, Sohan paid rent Rs. 5,000. This can be classified as

Accounting has universal application for recording _______ and events and presenting suitable information for decision making

Double Accounting System owes its origin to :

Purposes of an accounting system include all the following except

If owner’s capital is Rs. 50,000 liability is Rs. 30,000 and fixed assets is Rs. 70,000, then what is the value of current assets?

Users of accounting information include

Rs. 5,000 paid as rent of office premises in an/a _________

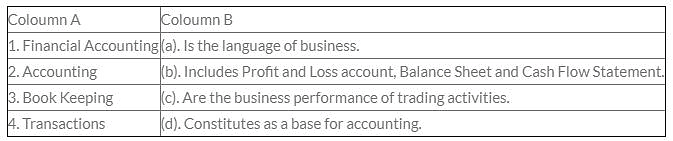

Match the following items from column A with column B.

Which of the following is correct? Owner’s Equity is :

The direct advantage of accounting do not include:

On March 31, 2011 after sale of goods worth Rs. 2,000, he is left with the closing inventory of Rs. 10,000. This is

The main objectives of Book- Keeping are :

________ of American Institute of Certified Public Accountants enumerated the functions of Accounting:

Match the following items from column A with column B.

Financial position of the business is ascertained on the basis of

Financial accounting information is characterized by all of the following except

The objective of wealth maximization takes into account

All of the following are functions of Accounting except

Which of these is not available in the Financial Statements of Company?

On 31st December, 2005, Ashok Ltd. purchased a machine from Mohan Ltd. for Rs. 1,75,000. This is : (year end : 31st December)

A system in which accounting entries are made on the basis of amounts having become due for payment or receipt is called

Gross Book Value of a fixed assets is its

|

64 videos|153 docs|35 tests

|

|

64 videos|153 docs|35 tests

|

Top Courses for Commerce

Important Questions for Meaning And Scope Of Accounting - 1

Meaning And Scope Of Accounting - 1 MCQs with Answers

Online Tests for Meaning And Scope Of Accounting - 1 Accountancy Class 11

|

© EduRev

|

Education Revolution

|

Follow Us

|