Test: Production and Costs- Match Based Type Questions - Commerce MCQ

15 Questions MCQ Test Economics Class 11 - Test: Production and Costs- Match Based Type Questions

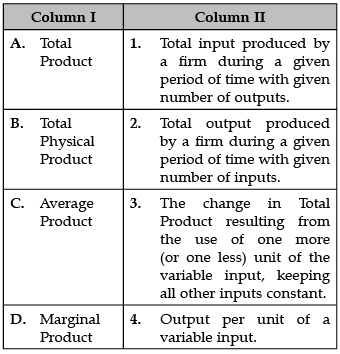

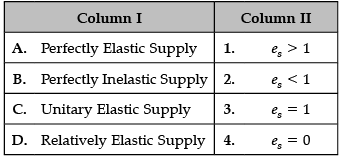

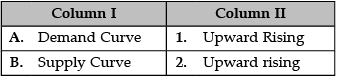

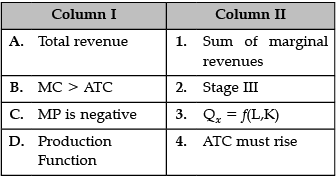

Identify the correct pair of items from the following Columns I and II:

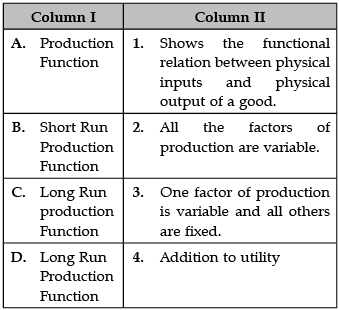

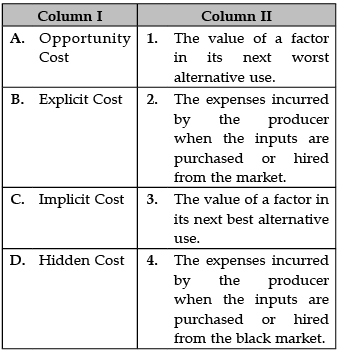

Identify the correct pair of terms and definitions from the following Columns I and II:

| 1 Crore+ students have signed up on EduRev. Have you? Download the App |

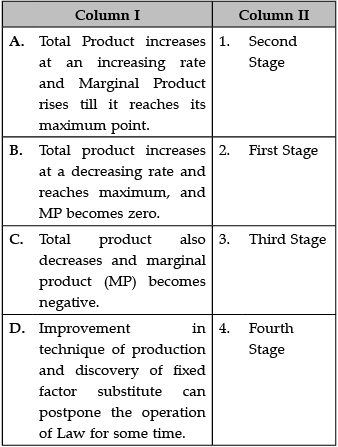

Identify the correct pair of from the following Columns I and II:

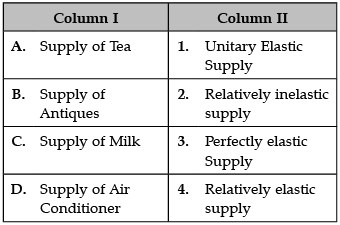

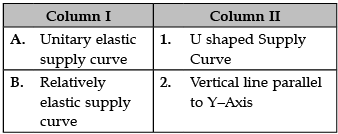

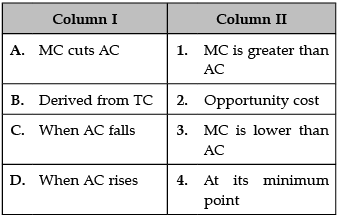

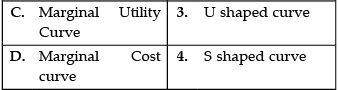

Identify the correct pair of items from the following Columns I and II:

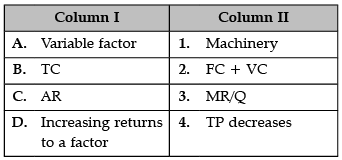

Identify the correct pair of items from the following Columns I and II:

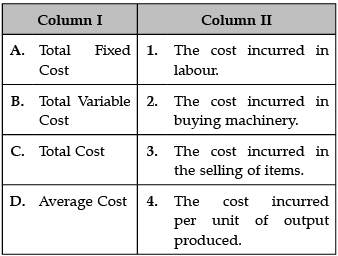

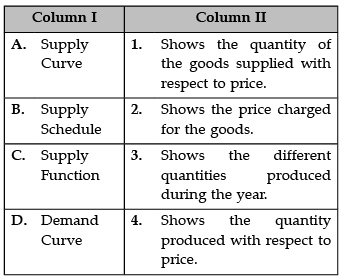

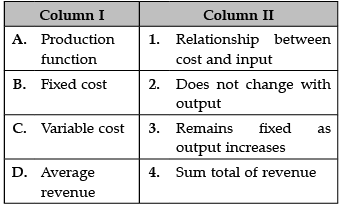

Identify the correct pair of items from the following Columns I and II:

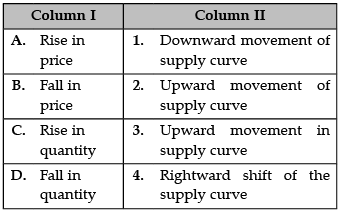

Identify the correct pair of items from the following Columns I and II:

Identify the correct pair of items from the following Columns I and II:

Identify the correct pair of items from the following Columns I and II:

Identify the correct pair of items from the following Columns I and II:

Identify the correct pair of items from the following Columns I and II:

Identify the correct pair of items from the following Columns I and II:

Identify the correctly matched items from Column I to that of Column II:

Identify the correctly matched items from Column I to that of Column II:

Identify the correctly matched statements from Column I to that of Column II:

|

58 videos|215 docs|44 tests

|

Important Questions for Production and Costs- Match Based Type Questions

Production and Costs- Match Based Type Questions MCQs with Answers

Online Tests for Production and Costs- Match Based Type Questions Economics Class 11

|

© EduRev

|

Education Revolution

|

Follow Us

|