Test: Market Equilibrium - 2 - Commerce MCQ

20 Questions MCQ Test Economics Class 11 - Test: Market Equilibrium - 2

| 1 Crore+ students have signed up on EduRev. Have you? Download the App |

The factor that causes a change in quantity demanded is

The factor that causes a change in quantity supplied is

A rise in the price of the complementary good leads to

A fall in the price of the good for a seller leads to

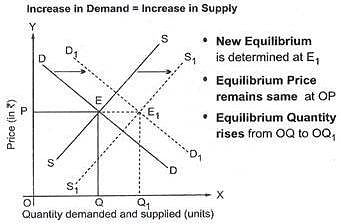

Market for a good is in equilibrium. An increase in demand for the good will

Market for a good is in equilibrium. A decrease in demand for the good will

Market for a good is in equilibrium. An increase in supply for the good will

Market for a good is in equilibrium. A decrease in supply for the good will

Market for a good is in equilibrium. An increase in demand for the good will

Market for a good is in equilibrium. An increase in supply for the good will

Market for a good is in equilibrium. An increase in the price of the good will

Market for a good is in equilibrium. A decrease in price for the good will

|

58 videos|215 docs|44 tests

|

Important Questions for Market Equilibrium - 2

Market Equilibrium - 2 MCQs with Answers

Online Tests for Market Equilibrium - 2 Economics Class 11

|

© EduRev

|

Education Revolution

|

Follow Us

|