|  Evolution and Constitutional Background of GST in India 50 Flashcards |  Start |

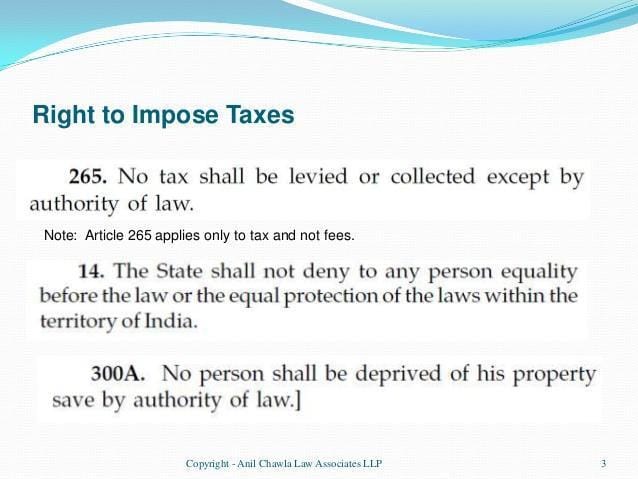

| Article 265 of the Constitution prohibits arbitrary tax collection, stating that ___ shall be levied or collected except by authority of law. |  Card: 1 / 50 |

| No tax | Card: 2 / 50 |

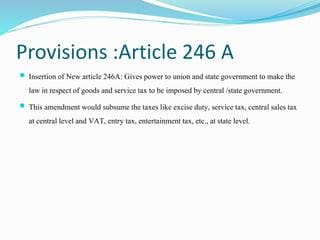

| True or False: The power to levy Goods and Services Tax (GST) is exclusively granted to the Centre according to Article 246A. | Card: 3 / 50 |

| False. The power to levy GST is granted to both the Centre and the States. | Card: 4 / 50 |

| Fill in the blank: If any tax law does not align with the Constitution, it is considered ___ and deemed illegal. | Card: 5 / 50 |

| Ultra vires | Card: 6 / 50 |

| What does the term 'authority of law' imply in the context of Article 265? | Card: 7 / 50 |

| It implies that the tax must be within the legislative competence of the body imposing it.  | Card: 8 / 50 |

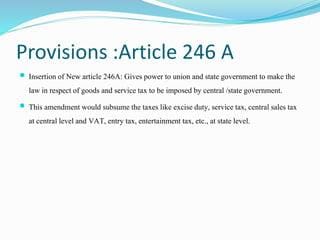

| According to Article 246A, the power to levy GST was introduced by the ___ Amendment Act of 2016. | Card: 9 / 50 |

| 101st | Card: 10 / 50 |

| True or False: Article 246A allows only the States to impose GST. | Card: 11 / 50 |

| False. Article 246A allows both the Centre and the States to impose GST. | Card: 12 / 50 |

| Fill in the blank: The powers of taxation, whether direct or indirect, stem from the ___ of India. | Card: 13 / 50 |

| Constitution | Card: 14 / 50 |

| What is the legal consequence if a tax law is found to be ultra vires? | Card: 15 / 50 |

| It is deemed illegal and void. | Card: 16 / 50 |

| The Constitution (101st Amendment) Act, 2016 was enacted to empower both the Centre and the States to levy and collect ___. | Card: 17 / 50 |

| Goods and Services Tax (GST)  | Card: 18 / 50 |

| True or False: The Centre exclusively levied taxes on services before the introduction of GST. | Card: 19 / 50 |

| True | Card: 20 / 50 |

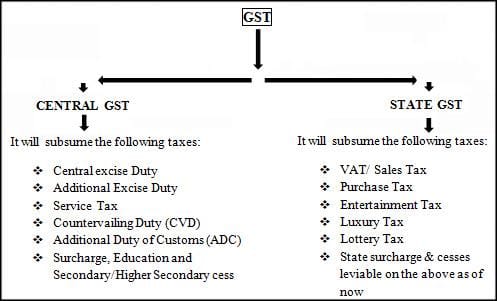

| Before GST, the Centre imposed excise duty on goods produced in India, while the States levied ___ once goods entered the stream of trade. | Card: 21 / 50 |

| Value Added Tax (VAT)  | Card: 22 / 50 |

| What necessitated the constitutional amendment for the GST implementation? | Card: 23 / 50 |

| The need to integrate various taxes into a unified Goods and Services Tax.  | Card: 24 / 50 |

| Fill in the blank: For inter-State sales, the Centre could levy Central Sales Tax, but the revenue was entirely retained by ___. | Card: 25 / 50 |

|  Unlock all Flashcards with EduRev Infinity Plan Starting from @ ₹99 only | |

| The States | Card: 26 / 50 |

| True or False: The introduction of GST removed the ability of States to levy any form of tax on goods. | Card: 27 / 50 |

| False. The introduction of GST allowed both the Centre and the States to levy and collect a unified tax. | Card: 28 / 50 |

| Short Answer: What type of tax did the Centre impose on all goods produced or manufactured in India prior to GST? | Card: 29 / 50 |

| Excise duty  | Card: 30 / 50 |

| Fill in the blank: The introduction of GST integrated various taxes, including excise duty and ___. | Card: 31 / 50 |

| Central Sales Tax  | Card: 32 / 50 |

| Article 246A of the Constitution of India grants power to which entities regarding Goods and Services Tax? | Card: 33 / 50 |

| It grants power to both the Centre and State Governments to make laws regarding GST.  | Card: 34 / 50 |

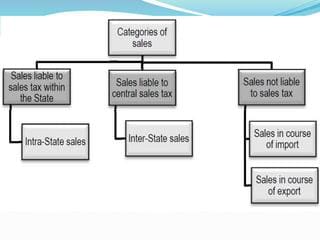

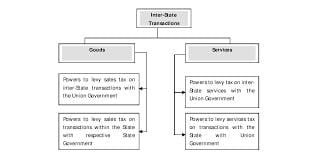

| True or False: The Centre has exclusive power to legislate on GST for intra-State supply of goods and/or services. | Card: 35 / 50 |

| False. The Centre has exclusive power to legislate on GST for inter-State supply of goods and/or services.  | Card: 36 / 50 |

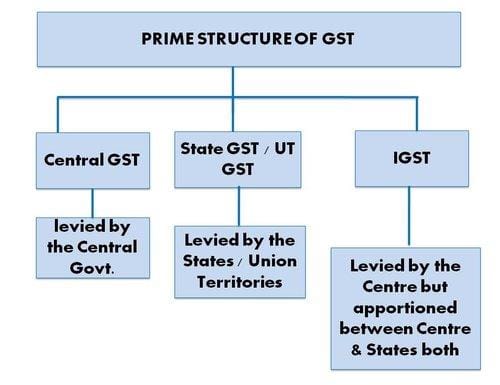

| GST on inter-State supplies is levied and collected by which government? | Card: 37 / 50 |

| GST on inter-State supplies is levied and collected by the Government of India.  | Card: 38 / 50 |

| Fill in the blank: The collected GST tax is apportioned between the Union and the States as per the law made by Parliament on the recommendations of the ___ . | Card: 39 / 50 |

| Goods and Services Tax Council.  | Card: 40 / 50 |

| According to Article 366, what does 'goods' include? | Card: 41 / 50 |

| 'Goods' includes all materials, commodities, and articles as defined under Article 366. | Card: 42 / 50 |

| Fill in the blank: The term 'services' encompasses anything other than ___ . | Card: 43 / 50 |

| Goods. | Card: 44 / 50 |

| True or False: The import of goods or services into India is considered as supply in the course of inter-State trade or commerce. | Card: 45 / 50 |

| True.  | Card: 46 / 50 |

| What is excluded from the definition of 'goods and services tax' as per Article 366? | Card: 47 / 50 |

| Taxes on the supply of alcoholic liquor for human consumption are excluded. | Card: 48 / 50 |

| What is the primary purpose of the Goods and Services Tax (GST) Council as established by Article 279A? | Card: 49 / 50 |

| The primary purpose of the GST Council is to recommend important issues such as tax rates, exemptions, threshold limits, and dispute resolution to the Union and the States. | Card: 50 / 50 |

| Completed! Keep practicing to master all of them. |  Restart |