Accounts From Incomplete Records Single Entry System (Part - 3) | Accountancy Class 11 - Commerce PDF Download

Page No 20.43:

Question 20:

A firm sells goods at a Gross profit of 25% of sales. On 1st April, 2018 the Stock was ₹ 40,000; Purchases were ₹ 1,10,000 and the Stock on 31st March, 2019 was ₹ 30,000. What was the value of Sales?

ANSWER:

Cost of Goods Sold = Net Sales – Gross Profit

Cost of Goods Sold = Opening Stock + Purchases – Closing Stock

Cost of Goods Sold = 40,000 + 1,10,000 – 30,000 = ₹ 1,20,000

Gross Profit = 25% of Sales or 33.33% of COGS

Gross Profit = ₹ 40,000

Net Sales = Cost of Goods Sold + Gross Profit

Net Sales = 1,20,000 + 40,000 = ₹ 1,60,000

Question 21:

A firm sells goods at Cost plus 25%. Sales to credit customers (3/4 of total) was ₹ 1,80,000. His Opening and Closing Stocks were ₹ 20,000 and ₹ 15,000 respectively. Find out the value of Purchases.

ANSWER:

Credit Sales = ₹ 1,80,000 (3/4 of Total Sales)

Total Sales = ₹ 2,40,000

Gross Profit = 25% of Cost or 20% of Sales

Gross Profit = ₹ 48,000

Cost of Goods Sold = Net Sales – Gross Profit

Cost of Goods Sold = 2,40,000 – 48,000 = ₹ 1,92,000

Cost of Goods Sold = Opening Stock + Purchases – Closing Stock

1,92,000 = 20,000 + Purchases – 15,000

Purchases = ₹ 1,87,000

Question 22:

Calculate Stock in the beginning:

ANSWER:

Let cost be Rs 100

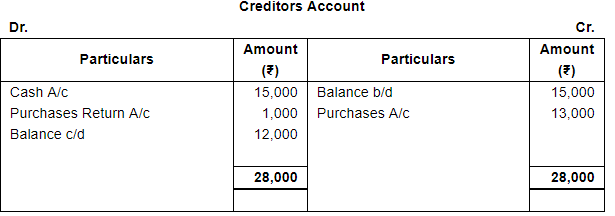

Loss = ₹ 16.67 (1/6 of 100)

Sale = ₹ 83.33 (100 – 16.67)

% Loss on Sale = 20% (16.67/83.33)

Loss on Sale = ₹ 16,000 (20% of 80,000)

Cost of Goods Sold = Net Sales + Loss on Sale

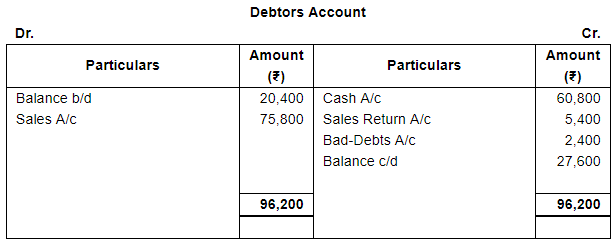

Cost of Goods Sold = 80,000 + 16,000 = ₹ 96,000

Cost of Goods Sold = Opening Stock + Purchases – Closing Stock

96,000 = Opening Stock + 60,000 – 8,000

Opening Stock = ₹ 44,000

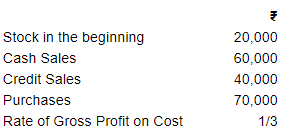

Question 23:

Calculate the Stock at the end:

ANSWER:

Rate of Gross Profit on Cost = 1/3

Rate of Gross Profit on Sale = 1/4

Total Sales = Cash Sales + Credit Sales

Total Sales = 60,000 + 40,000 = 1,00,000

Gross Profit = ₹ 25,000 (1/4 of 1,00,000)

Cost of Goods Sold = Net Sales – Gross Profit

Cost of Goods Sold = 1,00,000 – 25,000 = ₹ 75,000

Cost of Goods Sold = Opening Stock + Purchases – Closing Stock

75,000 = 20,000 + 70,000 – Closing Stock

Closing Stock = ₹ 15,000

Page No 20.44:

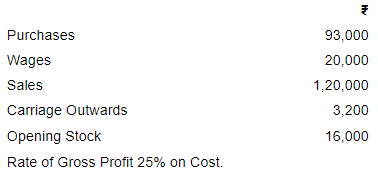

Question 24:

Calculate the value of Closing Stock from the following information:

ANSWER:

Rate of Gross Profit on Cost = 1/4

Rate of Gross Profit on Sale = 1/5

Gross Profit = ₹ 24,000 (1/5 of 1,20,000)

Cost of Goods Sold = Net Sales – Gross Profit

Cost of Goods Sold = 1,20,000 – 24,000 = ₹ 96,000

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

96,000 = 16,000 + 93,000 + 20,000 – Closing Stock

Closing Stock = ₹ 33,000

Question 25:

Calculate Purchases:

ANSWER:

Question 26:

Calculate Sales:

ANSWER:

Rate of Gross Profit on Sale = 1/5

Rate of Gross Profit on Cost = 1/4

Gross Profit = ₹ 50,000 (1/4 of 2,00,000)

Sales = Cost of Goods Sold + Gross Profit

Sales = 2,00,000 + 50,000 = ₹ 2,50,000

Question 27:

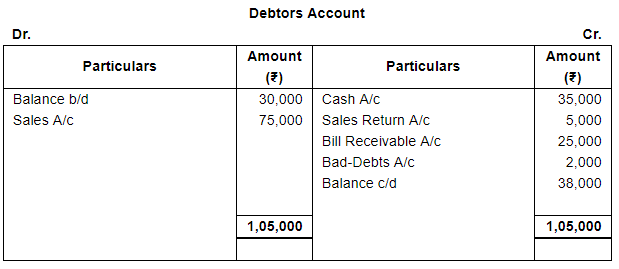

Debtors in the beginning of the year were ₹ 30,000, Sales on credit during the year were ₹ 75,000, Cash received from the Debtors during the year was ₹ 35,000, Returns Inward (regarding credit sales) were ₹ 5,000 and Bills Receivable drawn during the year were ₹ 25,000. Find the balance of Debtors at th end of the year, assuming that there were Bad Debts during the year of ₹ 2,000.

ANSWER:

Question 28:

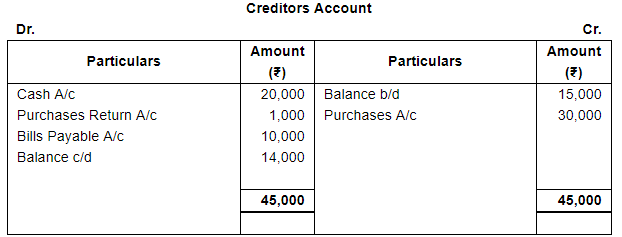

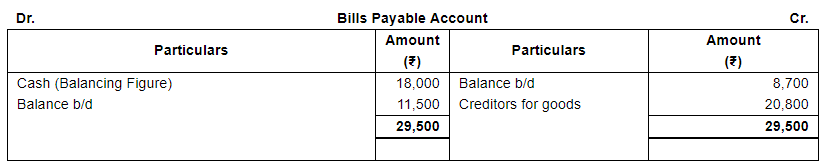

Creditors on 1st April, 2018 were ₹ 15,000, Purchases on credit were ₹ 30,000, Cash paid to Creditors during 2018-19 was ₹ 20,000, Returns Outward (regarding credit purchases) were ₹ 1,000 and Bills Payable accepted during the year were ₹ 10,000. Find the balance of Creditors on 31st March, 2019.

ANSWER:

Page No 20.44:

Question 29:

Following information is given of an accounting year:

Opening Creditors ₹ 15,000; Cash paid to creditors ₹ 15,000; Returns Outward ₹ 1,000 and Closing creditors ₹ 12,000.

Calculate Credit Purchases during the year.

ANSWER:

Question 30:

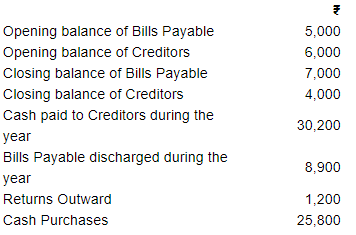

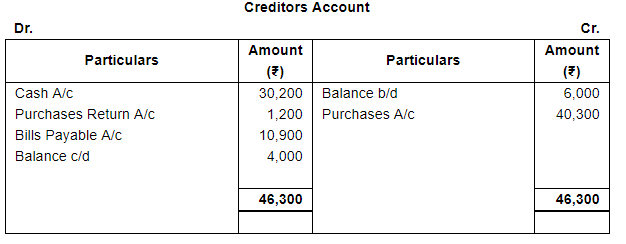

From the following information supplied by Rohit, who keeps his books on Single Entry System, you are required to calculate Total Purchases:

Total Purchases = Cash Purchases + Credit Purchases

Total Purchases = 25,800 + 40,300 = ₹ 66,100

Question 31:

Cash sales of a business in a year were ₹ 85,000, the Cost of Goods Sold (including direct expenses) was ₹ 97,000 and Gross Profit as shown by the Trading Account for the year was ₹ 1,29,000. Calculate Credit Sales during the year.

ANSWER:

Gross Profit = Net Sales – Cost of Goods Sold

1,29,000 = Net Sales – 97,000

Net Sales = ₹ 2,26,000

Credit Sales = Total Net Sales – Cash Sales

Credit Sales = 2,26,000 – 85,000 = ₹ 1,41,000

Page No 20.45:

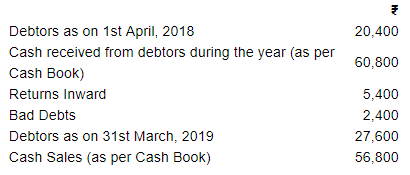

Question 32:

From the following information, calculate Total Sales made during the period:

ANSWER:

Total Sales = Cash Sales + Credit Sales

Total Sales = 56,800 + 75,800 = ₹ 1,32,600

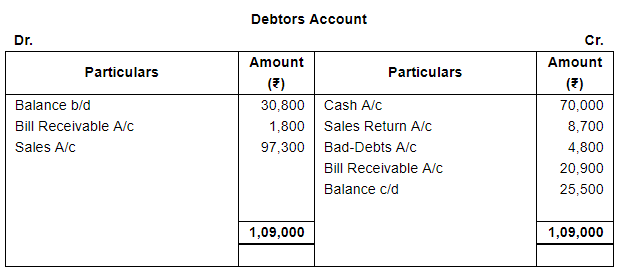

Question 33:

Calculate Total Sales from the following information:

ANSWER:

Total Sales = Cash Sales + Credit Sales

Total Sales = 15,900 + 97,300 = ₹ 1,13,200

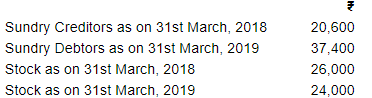

Question 34:

From the following information, ascertain the opening balance of Sundry Debtors and the closing balance of Sundry Creditors:

Page No 20.45:

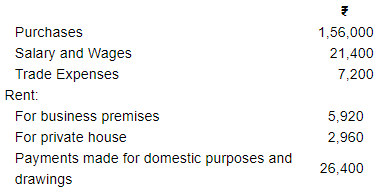

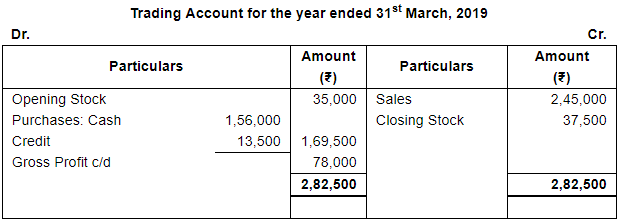

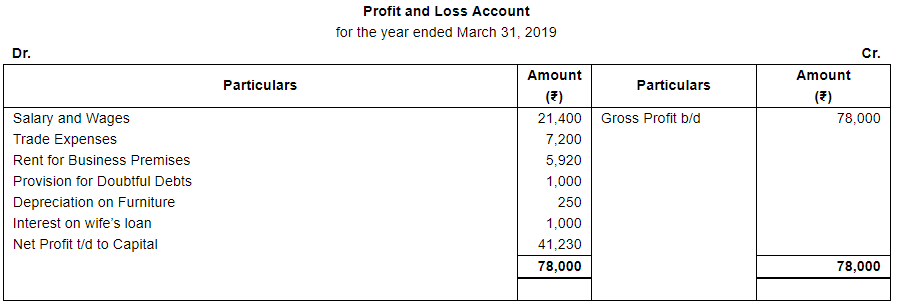

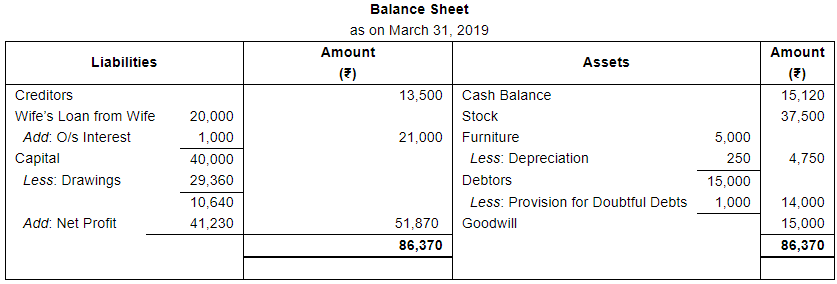

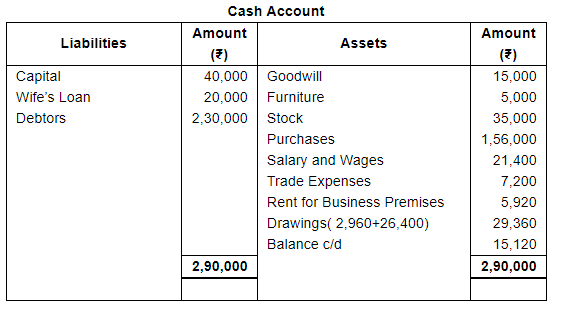

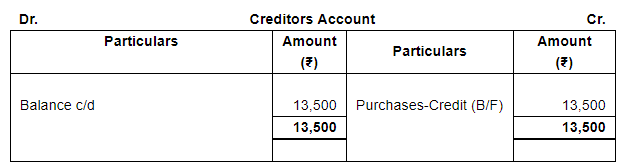

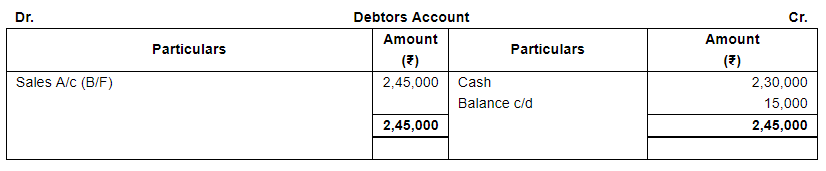

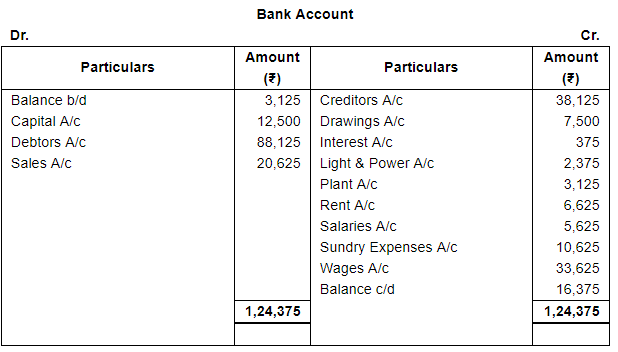

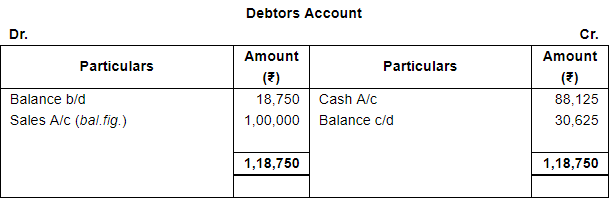

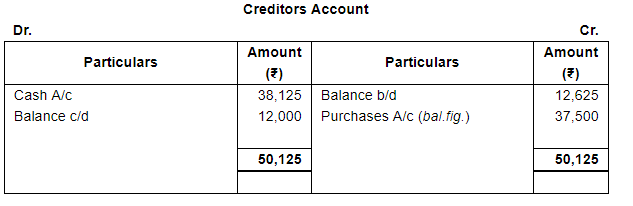

Question 35:

Roshan, whose accounts are maintained by Single Entry System, acquired a retail business on 1st April, 2018. He had ₹ 40,000 of his own and he borrowed ₹ 20,000 from his wife. He paid ₹ 15,000 for Goodwill, ₹ 5,000 for Furniture and ₹ 35,000 for Stock.

Total cash received by him during the financial year from the Debtors was ₹ 2,30,000. His payments were:

At the end of the year, the Stock was ₹ 37,500. He owed ₹ 13,500 to Creditors for goods and his customers owed to him ₹ 15,000. Provide 5% for Depreciation on Furniture, Interest at 5% on wife's Loan and ₹ 1,000 for Doubtful Debts.

Prepare the Cash Account, the Profit and Loss Account for the year ended 31st March, 2019 and the Balance Sheet at the close of the year.

ANSWER:

Working Notes

Page No 20.46:

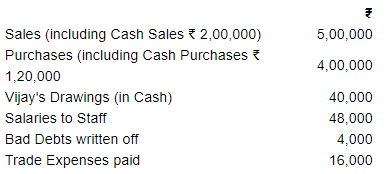

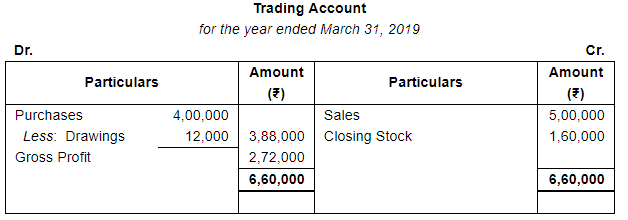

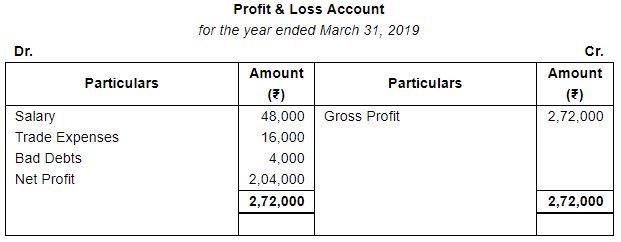

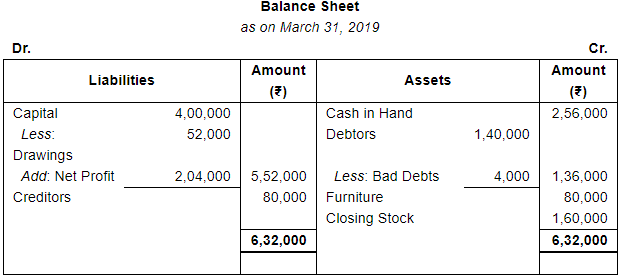

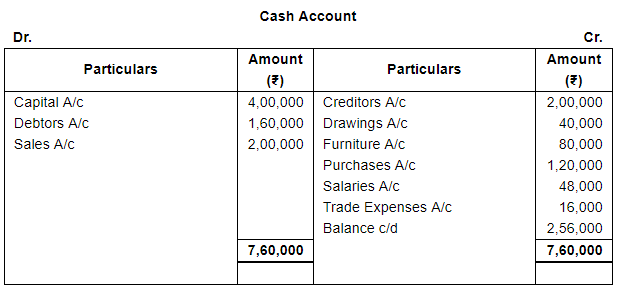

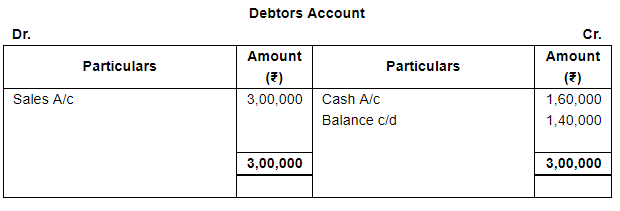

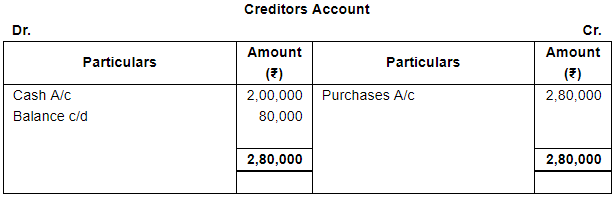

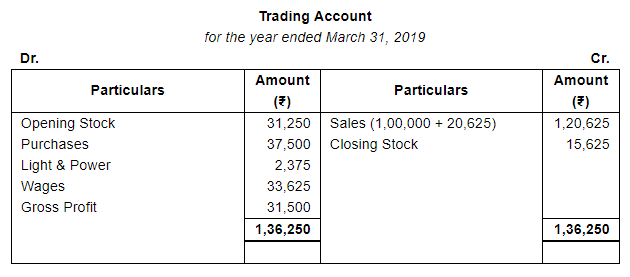

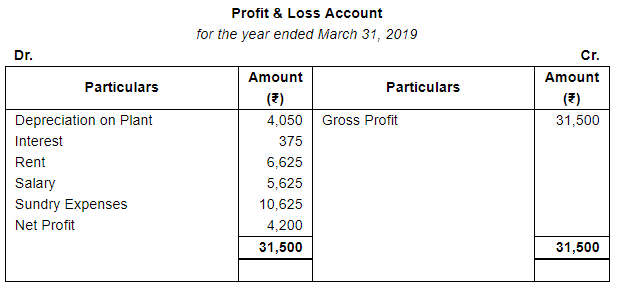

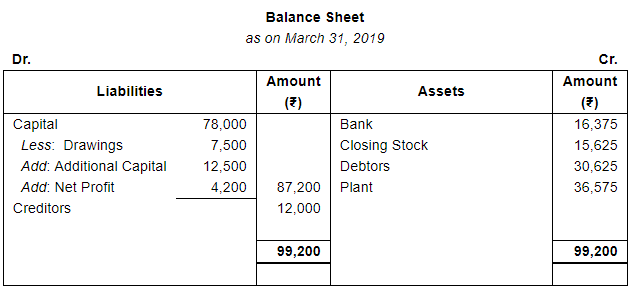

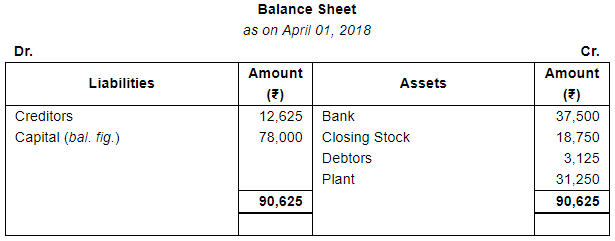

Question 36:

Vijay commenced business as food grains merchant on 1st April, 2018 with a capital of ₹ 4,00,000. On the same day, he purchased furniture for ₹ 80,000. From the following particulars obtained from his books which do not conform to Double Entry principles, you are required to prepare the Trading and Profit and Loss Account for the year ended 31st March, 2019 and the Balance Sheet as on that date:

Vijay used goods of ₹ 12,000 for personal purposes during the year. On 31st March, 2019, his Debtors amounted to ₹ 1,40,000 and Creditors ₹ 80,000. Stock-in-Trade on that date was ₹ 1,60,000.

ANSWER:

Page No 20.46:

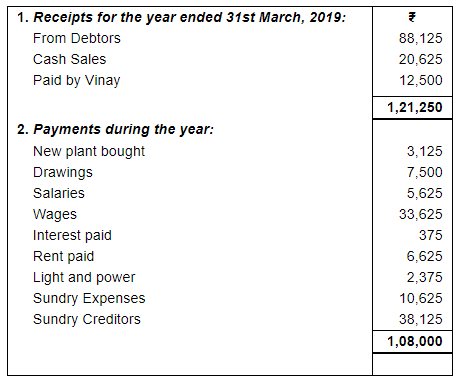

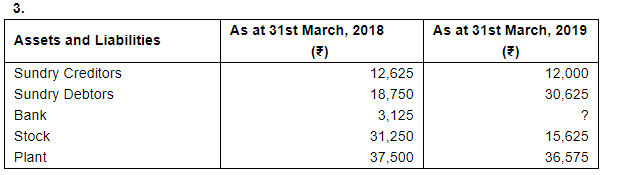

Question 37:

Following information is obtained from the books of Vinay, who maintained his books of account under Single Entry System:

Vinay banks all receipts and makes payments by means of cheque.

From the above information, prepare Trading and Profit and Loss Account for the year ended 31st March, 2019 and Balance Sheet as on that date.

ANSWER:

Page No 20.47:

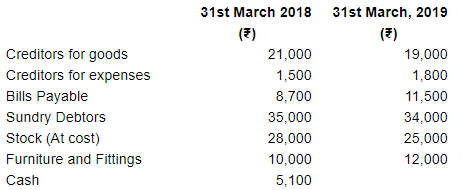

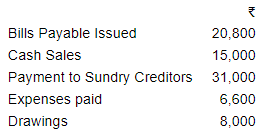

Question 38:

Surya does not keep a systematic record of his transactions. He is able to give you the following information regarding his assets and liabilities:

Following additional information is also available for the year ended 31st March, 2019:

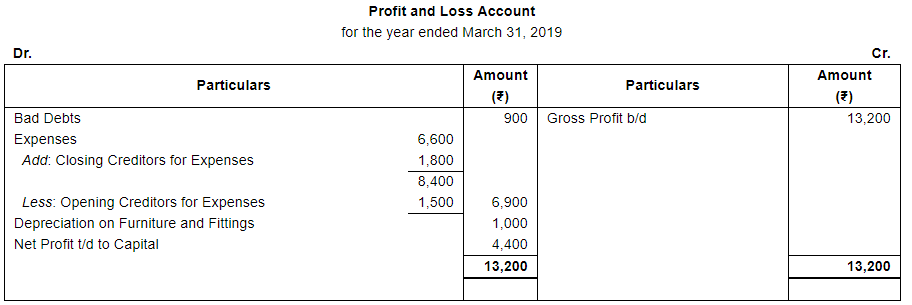

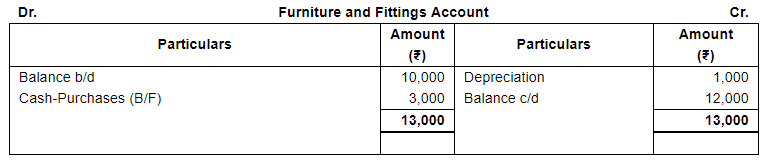

Bad Debts during the year were ₹ 900. As regards sale, Surya tells you that he always sells goods at Cost plus 25%. Furniture and Fittings are to be depreciated at 10% of the value in the beginning of the year.

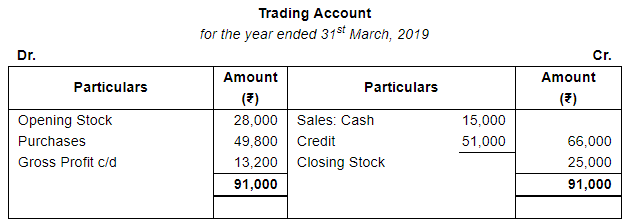

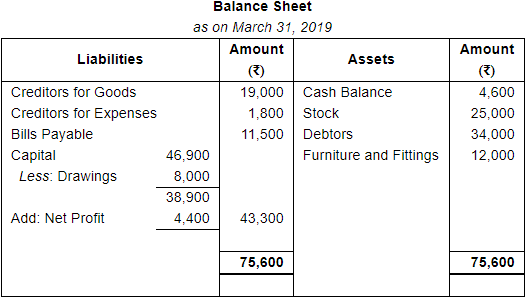

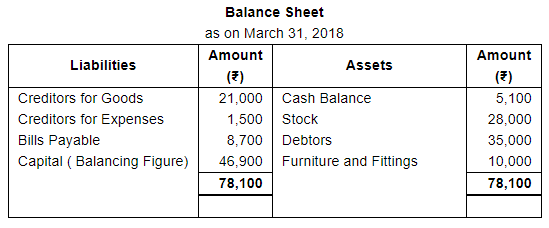

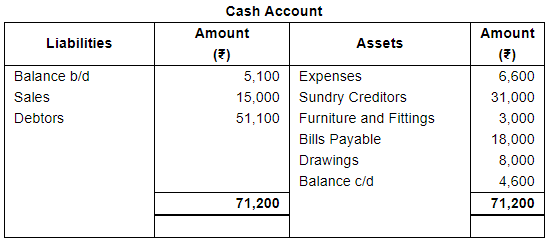

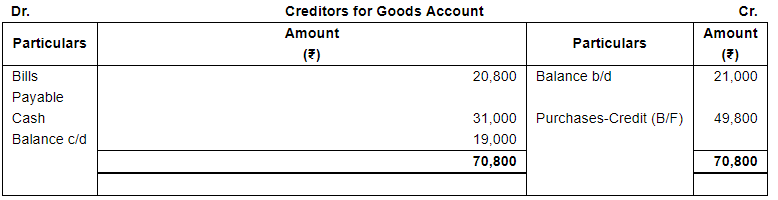

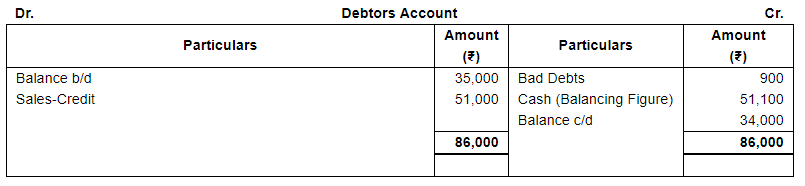

Prepare Surya's Trading and Profit and Loss Account for the year ended 31st March, 2019 and his Balance Sheet on that date.

ANSWER:

Working Notes

Computation of Cost of Goods Sold and Credit Sales

COGS = Opening. Stock + Purchases – closing. Stock = 28,000 + 49,800 – 25,000 = 52,800

Gross Profit = 52,800 × 25/100= 13,200

Total Sales = COGS + Gross Profit = 52,800 + 13,200 = 66,000 Credit Sales = Total Sales – Cash Sales= 66,000 – 15,000 = 51,000

Note: It has been assumed that a Drawings in cash of Amount ₹ 8,000 has been made by Surya during the year.

|

64 videos|153 docs|35 tests

|

FAQs on Accounts From Incomplete Records Single Entry System (Part - 3) - Accountancy Class 11 - Commerce

| 1. What is the single entry system in accounting? |  |

| 2. How does the single entry system differ from the double-entry system? | |

| 3. Can the single entry system provide an accurate financial position of a business? | |

| 4. What are the limitations of the single entry system? | |

| 5. When is the single entry system commonly used? | |

|

1.5K Views |

|

4.87/5 Rating |

|

Dec 22, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

ppt

,Accounts From Incomplete Records Single Entry System (Part - 3) | Accountancy Class 11 - Commerce

,Accounts From Incomplete Records Single Entry System (Part - 3) | Accountancy Class 11 - Commerce

,past year papers

,Exam

,video lectures

,Free

,Summary

,Extra Questions

,MCQs

,Previous Year Questions with Solutions

,Accounts From Incomplete Records Single Entry System (Part - 3) | Accountancy Class 11 - Commerce

,Semester Notes

,Sample Paper

,Important questions

,Viva Questions

,mock tests for examination

,shortcuts and tricks

,practice quizzes

,Objective type Questions

,study material

;

Accounts From Incomplete Records Single Entry System (Part - 3) Free PDF Download

Importance of Accounts From Incomplete Records Single Entry System (Part - 3)

Accounts From Incomplete Records Single Entry System (Part - 3) Notes

Accounts From Incomplete Records Single Entry System (Part - 3) Commerce Questions

Study Accounts From Incomplete Records Single Entry System (Part - 3) on the App

|

© EduRev

|

Education Revolution

|

|