Ascertainment of Profits - Insurance Company Accounts, Advanced Corporate Accounting | Advanced Corporate Accounting - B Com PDF Download

Ascertainment of Profit under the Single Entry System!

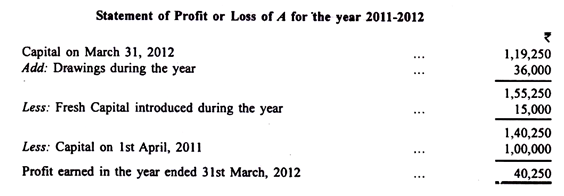

No Trading and Profit and Loss Account can be prepared. Profit, therefore, under the Single Entry System can be ascertained only by comparing capital at the end of the trading period with that in the beginning. Suppose, A finds that his capital on March 31, 2012 was Rs 1, 16,000, whereas it was Rs 80,000 on April 1, 2011, it is safe to conclude that there was a profit of Rs 36,000 during the year—otherwise how could the capital of Rs 80,000 (in the beginning of the year) grow to Rs 1, 16,000 at the end of the year? This is true but for two things.

If A introduced fresh capital during the year, the capital would increase and to that extent there would be no profit. If, in the above example, A introduced a further Rs 15,000 during the year, the profit is, then, not Rs 36,000 but only Rs 21,000 because Rs 15,000 of the increase is due to fresh capital.

Also, if A withdrew some of his capital during the year, then to that extent, the profit would be higher. Had he not been drawn the sum, the capital at the end would have been higher showing that profits are higher than they appear to be. Suppose, to continue the example, A withdrew Rs 20,000 during the year, his profits for 2011-2012 would be Rs 21,000 + Rs 20,000 or Rs 41,000.

Hence, to ascertain profit under the Single Entry System:

To the capital at the end of the year, add drawings during the year; and from this deduct fresh capital introduced during the year and also capital in the beginning of the year.

Capital at any time is found out by deducting liabilities from assets following the accounting equation:

Capital = Assets – Liabilities.

One has, therefore, to prepare a “balance sheet” which, in Single Entry, is called Statement of Affairs. The various assets and liabilities will be estimated as best as one can.

This is illustrated below:

A commenced business on April 1, 2011 with a capital of Rs 1, 00,000. He immediately bought furniture and fixtures for Rs 20,000. On 30th September, 2011, he borrowed Rs 50,000 from his wife at 9% p.a. (interest not yet paid) and introduced a further capital of his own amounting to Rs 15,000 A drew at the rate of Rs 3,000 per month at the end of each month for household expenses.

On 31st March, 2012, his position was as follows:

Cash in hand, Rs 2,000; Cash at Bank, Rs 26,000; Sundry Debtors, Rs 48,000; Stock, Rs 68,000; Bills Receivable, Rs 16,000; Sundry Creditors, Rs 5,000; and owing for Rent, Rs 1,500. Furniture and Fixtures are to be depreciated by 10%. To ascertain the profit or loss of A during 2011-2012, we must find out his capital on March 31, 2012.

Hence:

Illustration 1:

Mr. Z owns a general store in Delhi and does not maintain his accounts on double entry system.

His assets and liabilities on 1st April, 2011 were as follows:

Bills Payable Rs 20,000, Creditors Rs 33,100, Stock Rs 1, 20,000, Debtors Rs 66.000, Cash in hand and at Bank Rs 67,100 and Machine Rs 1, 50,000

His position on 31st March, 2012 was as follows:

Machine Rs 1, 50,000, Debtors Rs 93,200, Motor Cycle Rs 1, 20,000, Cash in hand Rs 30,000, Bank balance as per banks-statement Rs 59,300, Stock Rs 1, 34,000 and Creditors Rs 87,000. During the year, he withdrew Rs 45,000 for household requirements and a motor cycle was purchased for Rs 1, 20,000 for business use. A cheque for Rs 7,000 issued in March, 2012 was not presented to bank up to 31st March, 2012.

Ascertain the amount of profit earned by the trader for the year ended 31st March, 2010 after making the following adjustments:

(a) Write off Rs 4,000 as bad debts and make a provision for doubtful debts @ 5% on the remaining debtors.

(b) Provide for full year depreciation on Machine @ 8% per annum and on Motor Cycle @ 10% per annum on diminishing balance method.

Illustration 2:

The following is the balance sheet of M/s. P.Q. and R as on March 31, 2011:

P. Q, and R share profits in the ratio of 3:2:1 respectively after charging 12% interest on capitals. During 2011-2012, the drawings were P at Rs 8,000 per month; and Q at Rs 6,000 per month and R at Rs 5,000 per month. On 31st March 2012, the various assets were: Cash in hand, Rs 3,000; Sundry Debtors, Rs 86,000; Stock, Rs 2,27,500 at selling price which was fixed at cost plus 25% Furniture and Fittings, Rs 1,08,000; and Machinery and Plant, Rs 2,80,000. Liabilities were; Sundry Creditors, Rs 1,34,000; Bills Payable Rs 1,24,000 and Bank Overdraft, Rs 60,000 as per Pass Book which showed that a cheque of Rs 10,000 deposited had been returned dishonoured. Ascertain the profit or loss made by the firm in 2011-2012 and show the Balance Sheet as on 31st March, 2012.

|

89 videos|52 docs|22 tests

|

FAQs on Ascertainment of Profits - Insurance Company Accounts, Advanced Corporate Accounting - Advanced Corporate Accounting - B Com

| 1. What is the concept of ascertainment of profits in insurance company accounts? |  |

| 2. How is premium income accounted for in insurance company accounts? | |

| 3. What are claims expenses in insurance company accounts? | |

| 4. How is investment income accounted for in insurance company accounts? | |

| 5. What are operating expenses in insurance company accounts? | |

|

1.3K Views |

|

4.83/5 Rating |

|

Nov 15, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

past year papers

,Objective type Questions

,Semester Notes

,Previous Year Questions with Solutions

,Free

,study material

,Ascertainment of Profits - Insurance Company Accounts

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,ppt

,MCQs

,Ascertainment of Profits - Insurance Company Accounts

,Viva Questions

,Sample Paper

,Ascertainment of Profits - Insurance Company Accounts

,video lectures

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,mock tests for examination

,Important questions

,Exam

,Extra Questions

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,Summary

,shortcuts and tricks

,practice quizzes

;

Ascertainment of Profits - Insurance Company Accounts, Advanced Corporate Accounting Free PDF Download

Importance of Ascertainment of Profits - Insurance Company Accounts, Advanced Corporate Accounting

Ascertainment of Profits - Insurance Company Accounts, Advanced Corporate Accounting Notes

Ascertainment of Profits - Insurance Company Accounts, Advanced Corporate Accounting B Com Questions

Study Ascertainment of Profits - Insurance Company Accounts, Advanced Corporate Accounting on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|