Chapter 5 and 6: Money and Banking - Chapter Notes, Macro Economics, class 12 - Commerce PDF Download

Money

C - C ECONOMY :: It refers to economy in which commodities are exchanged for commodities or in which goods are exchanged for goods . C stands for commodity. In other words it refers to barter system of exchange

C stands for commodity. In other words it refers to barter system of exchange

DRAWBACK’S or DIFFICULTY or

LIMITATION OF BARTER SYSTEM OF EXCHANGE

(1) DIFFICULTY OF DOUBLE COINCIDENCE OF WANTS :: Simultaneous fulfillment of mutual wants by buyer and seller is known as double coincidence of wants.

It is a situation where a person having horse have to find a person who wants his horse and at the same time possesses a cow that he wants to buy.Thus sale and purchase has to take place at same point of time . This is a rare occurrence and hence that person either

It is a situation where a person having horse have to find a person who wants his horse and at the same time possesses a cow that he wants to buy.Thus sale and purchase has to take place at same point of time . This is a rare occurrence and hence that person either

have to accept something less desirable than cow

or

has to make some intermediate transaction like sell his horse for camel , then further camel for sheep and sheep for cow.

(2) LACK OF COMMON UNIT OF VALUE :: Since there is no common measurement for goods ,it means if there are 1000 goods in the market ,value of each would have to be expressed in terms of 999 others.

And also under such system value of a good say car would be expressed in

terms of horses , cows or buffaloes.Thus there can be no ACCOUNTING STANDARDS

and difficulty in keeping accounts on double entry system

LACK OF DIVISIBILITY :: There are many goods which are not divisible . Lack of

divisibility makes barter exchange impossible . For example , the value of horse is 1000 kg

wheat but the other person has only 500 kg wheat . In such a situation the horse cannot be

divided into two pieces.

(3) LACK OF SYSTEM FOR FUTURE PAYMENT OR CONTRACTUAL PAYMENT :: It refers to problem of paying a worker for hiring his services or paying interest on borrowing as there is no standard method of calculating and payment is to be made in terms of rice or wheat or chair or table or other specific good.Thus it is very difficult to make payment in terms of goods due to following problems

(a) Problem of Knowing market value of goods in relation of other goods

(b) Problem of quality of goods specified

(c) Problem of choice of goods to be paid in future

(4) LACK OF SYSTEM FOR STORAGE OF VALUE :: Because of lack of money in the C.C economy wealth is stored in terms of goods and services which is subject to problem like

(a) cost of storage

(b) loss of value

(c) difficulty in quick disposition

There is also problem of transfer of saving in form of goods as it has to be carried from

one place to other.

TRADING COST IN C.C ECONOMY

(1) SEARCH COST :: It is the cost of finding the person whose want coincides with yours.It is basically a opportunity cost in terms of WASTAGE OF TIME in finding the other person who want to buy your product and possesses what you want to buy

(2) DISUTILITY OF WAITING :: Waiting for the person to satisfy double coincidence of wants involves discomfort and disutility.It is a type of REAL COST as longer the person spend searching , the greater will be the

search cost.

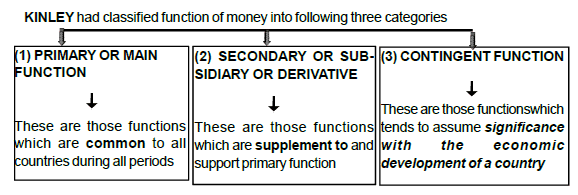

FUNCTION’S OF MONEY

STATIC FUNCTION :: It refers to conventional functions of money . Such functions only help to regulate the economic system , they donot stimulate the economic system to a higher level of growth and development.These basically INCLUDES PRIMARY & SECONDRY FUNCTIONS of money like medium of exchange , measure of value and standard for deffered payments

DYNAMIC FUNCTIONS :: It refers to those functions of money which impart stability to the economy and push an economy to a higher level of growth and development.

EXAMPLE :: It is by expanding the supply of money ( or purchasing power ) that the government all over the world have tried to control the recession , or by transferring saving into investment

PRIMARY FUNCTION

(1) MEDIUM OF EXCHANGE :: It means that money acts as an intermediate in an exchange transaction and it can be used to make payment for all transaction of goods and servicesIt has removed the major difficulty of double coincidence of wants in the Barter System.

In the monetary system act of sale and purchase is separated from each other. If one wants to buy goods, he can do so with money and if one wants to sell goods he can do so with money.That is a person can buy anything without selling at the same time and sell anything without buying at the same time .

It has also given freedom of choice or bearer of option as the owner of horse need not buy cow from person to whom horse is sold.Thus money provides generalised purchasing power to buy things from those who offer best bargain . As a result exchange has become convenient as well as simple and lot of time and efforts is saved.

Money thus facilitates multilateral trade and offer economic freedom to people

(2) MEASURE OF VALUE OR UNIT OF VALUE :: Money serves as a measure of value in terms of unit of account which means value of each and every good/services can be expressed in monetary unit. This helps in

(a) DETERMINING THE RELATIVE PRICE between different goods and show their mutual exchange values e.g if ghee is expressed as 10 /kg and sugar is 2/kg Then their exchange value is 1 kg Ghee = 5 kg of sugar.

(b) DETERMINING PURCHASING POWER OR VALUE OF MONEY :: The same method can be used to calculate the value of money itself with respect to other commodities.

Example :: A rupee is worth

1/10 = .1 Kg / ghee or

1/2 = .5 kg / sugar.

Thus if price of all commodities has increases , the value of money ( purchasing power ) in terms of any commodity will decrease

(c) ACCOUNTING BECOMES SIMPLE AND EASY as values of assets and liabilities can be easily expressed in terms of money .It is also convenient to ascertain cost, revenue ,profit and losses.Accordingly measurement of National income ,per capita income andother macro- variable is also facilitated.

SECONDARY / SUBSIDIARY FUNCTIONS

(3) STANDARD OF DEFERRED PAYMENT :: Deferred payment refers to those payment which are made in future.Money has made easy to return principal amount with interest on loan as calculation can be easily done and repayment can be made in same money in which it was borrowedUnder Barter system of exchange this was difficult to make such transaction in terms of goods and services e.g if somebody takes loan in form of wheat then at the time of returning it is not possible to return wheat of same quality and also of calculation of how much to be returned.Money is the link which connects the value of today with those of the future . Thus money has resulted in higher borrowing for consumption and investment which results in higher level of economic developmentIt has also facilitates sale and purchase of share , debenture ,bonds etc. and thus has resulted in growth of money market and capital market and thus there is more capital formation

(4) STORE OF VALUE :: Money acts as store of value which means acts as a store of wealth which means money can be used to transfer purchasing power from present to future .

This store of wealth is used for future investment and results in higher level of economic activity.It is convenient to store value in terms of money because

(a) Money is generally acceptable that is it can be easily exchange for good at any time

(b) value of it remains stable

(c) It is more durable and doesn’t require much space .

Newlyn calls it as ASSET FUNCTION OF MONEY.

This desire of people to save part of their wealth in the form of money is known as LIQUIDITY PREFERENCE

(5) TRANSFER OF VALUE :: Money in this regard helps to transfer capital from one person to another and from one place to another.Money can effect such transfer easily,quickly and efficiently . e.g it is impossible to take house from Delhi to Lucknow but it is possible to sell off the house in Delhi, get money and construct or purchase a new house in Lucknow.Thus this increases mobility of Capital which is necessary to quicken the process of growth across all region of the country.

CONTINGENT FUNCTION

(6) BASIS OF CREDIT CREATION :: Money serves as the basis of all credit instrument like cheque ,draft ,bills receivables.Bank creates credits only on the basis of money deposit kept by the people in the banking structure of the country.

(7) DISTRIBUTION OF NATIONAL INCOME :: With introduction of money it is possible to measure and distribute National Income among different factor of production in form of rent, interest, wages and profit .

(8) GUARANTEE OF SOLVENCY :: A firm or individual is declared bankrupt when it fails to fulfil monetary liabilities,even when their total asset is greater than total liabilities.With a view to retaining its solvency every individual,firm,bank,or insurance company prefers to keep some money in cash which would serve as a guarantee against insolvency.

(9) MEASUREMENT OF MAX SATISFACTION :: A consumer maximises his satisfaction when the Marginal Utilities from different goods is equal to their respective prices. Study of such relationship has become possible only with Money

(10) BEARER OF OPTION :: It implies that while accumulating wealth in form of money, the decision regarding the purchase of goods and services can be changed. Suppose a person has saved money for the purchase of Car. But it need money for his wife’s illness. He can without any difficulty change his decision and thus have freedom of action .

______________________________________

CHECK YOUR CONCEPT

(Q1) Identify the function of money highlighted in the given statement.

(i) This function has led to capital formation and economic development of the economy.

(ii) This function has separated the acts of sale and purchase.

(iii) This function of money facilitates transfer of purchasing power from present to future.

(iv) It works as a common denomination, in which values of all goods and services are expressed.

(v) This function of money is also termed as ‘Asset Function’ of money.

(vi) This function has simplified the borrowing and lending operations.

(vii) This function helps to find out exchange ratios between various goods and services.

(viii) This function has removed the difficulty of lack of double coincidence of wants.

(ix) This function helps to make payments for all transactions of goods and services.

(Q2) Explain how introduction of money has led to the expansion of markets.

Ans. (i) By removing the problem of double coincidence of wants and seperating the act of

sale and purchase and thus giving multi - lateral trade option

(ii) It has led to the emergence of money market and capital market

(iii) It has led to creation of Financial intermediates like Banks , PFI which ensure avilability

of funds both for consumption and investment

(iv) Expansion of global market by way of foreign investment , Export and Import.

__________________________________

SUPPLY OF MONEY :: It refers to total stock of money of all types (currency , paper notes and coins) held by the public or by those who demand money.

However it doesn’t include suppliers / producer of money i.e. stock of money held by

(a) The Government of the country

(b) The Banking system of the country both central and commercial BanksIt is a stock concept and is measured at a given point of time .

SPECIAL PIONT :: Total stock of money differs from total supply of money

IDEAL SUPPLY OF MONEY :: It is that supply of money which matches the market value of flow of goods and services in the economy so that all goods and services can be purchased and there is no deficient or excess demand and thus no inflation or deflation.

[Intext question]

COMPONENTS OR MEASUREMENT OF MONEY SUPPLY IN INDIA

In India ,RBI employs four alternatives measure of Money supply M1 M2 M3 and M4 which are

based on DECREASING ORDER OF LIQUIDITY

M1 = It is the most liquid concept of money supply. It is also known as “Transaction Money”

M1 = C + DD + OD where

C refers to currency , paper notes and coins held only by the publicDD refers to demand deposit of people with the commercial banks which can be withdrawn by cheque or otherwise on demand.

Only Net Demand Deposits are included :: It must be noted that inter-bank deposits are

excluded. Inter-bank deposits are the deposits held by banks on behalf of other bank.

OD refers to other deposit with RBI of

(a) Financial institutional like IDBI

(b) International financial institutional like IMF ,World Bank

(c) Foreign central bank and of Foreign Central govt.

However OD doesnot include deposit of Indian Govt. and Commercial bank with RBIThis OD constitues very small proportion of M1 and hence donot have much significance

CURRENCY COMPONENT (C) :: It consists of coins and paper currency.

(1) COINS :: Coins are made up of metal. The metallic coins are issued by the monetary authority of the country, i.e., central bank with the central government of the country.

The metal used in coins has no significance and these coins are used as token coins since their face value is much higher than their intrinsic value. In India, today coins of 50 paise, Rs 1, Rs 2 , Rs.5 and Rs 10 are in use.

(2) PAPER CURRENCY :: Paper currency or currency notes are the most important part of the money supply. The central bank in every country has monopoly right of issuing currency notes.

In India, one rupee note is issued by the Ministry of Finance, GOI, while the remaining notes of higher denominations or coins are issued by the central bank, i.e., RBIIn our country, RBI has to keep reserve of Rs. 200 crores in which there is gold bullion of Rs. 115 crores and foreign securities of Rs. 85 crores.The present monetary system in India is managed and controlled by RBI and is also known as “INCONVERTIBLE PAPER CURRENCY SYSTEM ”

DEFINITION’s OF MONEY

MEANING OF MONEY :: “ Money may be defined as anything that is generally accepted as a mean of exchange and at the same time acts as a measure and as a store of value” - CROWTHER

____________________

“ Money is matter of functions four ”

A medium , a measure , a standard , a store ”

_______________________

LEGAL or FIAT MONEY :: It refers to money which is backed by govt. authority/ order and thus is proclaimed by Law as medium of exchange.They are called legal tenders as they cannot be refused by any citizen of the country for settlement of any kind of transaction

FIDUCIARY MONEY :: It refers to money which is backed by trust or consent between payer and payee . It is also known as ORIGINAL MONEY

E.g cheque are accepted as a mean of payment on the basis of trust but not as legal tenders as it can be refused as a mode of payment

FUNCTIONAL MONEY :: It refers to money as anything that perform four basic functions

(1) Serve as medium of exchange

(2) Serve as unit of value

(3) Serve as deferred payment

(4) Serve as store of value

Thus it is a NARROW DEFINITION of money

NARROW DEFINITION OF MONEY :: Functional definition of money is narrow definition.It includes only notes, coins and demand deposits (chequable deposits).

M1 is a measure of narrow money .It is also called MONEY ASSETS that is referring to assets which function as money

BROAD DEFINITION OF MONEY :: In this definition of money time deposits / fixed deposits with the bank and post office are also included.

Thus it is sum of both MONEY ASSET AND NEAR MONEY ASSET that is referring to assets which can be converted into money on a short notice

HIGH POWERED MONEY :: The Total Liability of monetary authority of country (RBI) is called the monetary base or High powered Money.High powered money serves as th basis of bank money therefore it is also called “ Base Money” or “ Monetary Base” . Thus it determines the total flow of money in economy

It consists of

(a) CURRENCY NOTES AND COINS IN CIRCULATION with the public and vault cash of Commercial bank. If the member of public produces a currency note to RBI, then RBI must pay for value equal to figure printed on the note

(b) DEPOSIT HELD BY GOI or COMMERCIAL BANK WITH RBI as these deposits are refundable by RBI on demand from these deposit-holders

DIFFERENCE BETWEEN ‘MONEY’ AND ‘HIGH POWERED MONEY’

Money = C + DD + OD

High Powered Money = C + R + OD

C : Currency with the public (notes + coins)

R : Cash reserves of banks.

Broadly, the difference between ‘money’ and ‘high powered money’ lies in the inclusion of

“ Reserves (R) ” which is the actual base of demand deposit

CLASSIFICATION OF MONEY

(A) ON THE BASIS OF LIQUIDITY :: Liquidity of an asset refers to its convertibility into money / cash without loss of time and value.Faster an assets can be converted into cash more liquid it is. On basis of this there is

(1) MONEY :: It refers to notes,coins and currency and instrument like cheque which are commonly accepted as payment for goods and services or settlement of debts.These are highly liquid almost 100 %

(2) NEAR -MONEY :: It refers to less liquid assets and it includes all such financial instrument like Kisan Vikas Patra ,time deposits /fixed deposits with the bank and post office,Equity share , Bonds .These items can be converted into demand deposit (chequable deposit )on short notice and hence are NEAR - MONEY ASSET

(B) ON BASIS OF MARKET VALUE (MV) // FACE VALUE &

COMMODITY VALUE OF MONEY(CV) // INTRINSIC VALUE

(1) FULL BODIED MONEY :: It refers to money in terms of coins where MV=CV of money. In other words the facve value is equal to intrinsic value

E.g a rupee coin during Bristish period in India was made of silver of value of Rs.1(2) REPRESENTATIVE FULL BODIED MONEY :: It refers to paper notes as representative of full bodied money. Such paper notes are like receipt issued by govt. for full bodied money and thus can be converted by holder into bullion.After conversion

MV of notes = CV of notes = Market value of bullion

____________________________________

It is accepted as money as it can be conveniently used for carrying out transactions.Such a type of paper money is 100 % backed by metallic reserve of gold or silver and is redeemable at the option of the holder.

Example :: U.S Gold certificates prior to 1933 , fully backed by gold

____________________________________

(3) CREDIT MONEY :: It refers to modern day currency where MV of money is greater than CV of money i.e value at which currency will be exchanged in the market { face value } in more than value of material used to make currency { intrinsic value } . It includes

(1) Token coin like rupee coin or 50 paise coin

(2) Representative token coin or paper notes (circulating warehouse receipt)

(3) Promissory Note like Rs.500 or Rs.1000 paper note

(4) Demand deposit at bank

Banking

COMMERCIAL BANK :: A Commercial bank is that financial institution which

accepts deposits from the people andgives loan for the purpose of consumption and investment.

Besides, it also performs many agency function and provides general utility services

________________________

According to Indian Banking Companies Act “ Banking company is one which transacts the business of banking which means the accepting for the purpose of lending or investment of deposit of money from the public repayable on demand or otherwise and withdrawable by cheque , draft , order or otherwise ”

___________________________

_________________________

(Ques) Any business dealing in money matters can be labelled as Banking ? Comment

“All banks are financial institution but all financial institution are not bank”.Discuss

There are two essential functions that makes a Bank

(a) Accepting chequable deposit

(b) Providing loan or advances.

If any financial institution fails to satisfy any one of the function ,it cannot be labelled as a bank

even it deals in money matters E.g

(1) LIC is a financial institution as it lends to others but it is not a bank as it donot accept

chequable deposits from the public

(2) Post offices are also not banks even though they accept deposits from the public

because they donot offer loans

________________________________

CENTRAL BANK :: It is apex bank which is responsible for controlling the entire banking system of a country and also for monetary policy of the country to maintain price stability for economic growth.In India RESERVE BANK operate as central bank of the country

SAMUELSON “Every Central Bank has one function. It operates to control economy,

supply of money and credit”

FUNCTIONS OF CENTRAL BANK

(1) CURRENCY AUTHORITY OR ISSUING OF NOTES :: Central bank has exclusive authority to issue notes in every country of the world. All the currency issued by the Central bank is its monetary liability which means for every value of currency issued central bank has to back it with rupee reserve of gold coin or gold bullion or foreign securities.

Thus

If 100 cr of currency printing = 100 cr Gold or bullion backeds

This monopoly right of Central bank to issue notes has following merits :

(a) It provides with uniformity to monetary system

(b) People confidence in the currency grows as it is backed by government support

(c) Supply of money can be increased or decreased easily and thus it provides elasticity to monetary system and helps in stabilisation of internal and external value of currency.

(d) It enables the government to have supervision and control over the central bank with respect to issue of notes.

____________________________

DEFICIT FINANCING OR MONETISATION OF BUDGET DEFICIT :: When the central government EXPENDITURE EXCEEDS GOVT. REVENUE , then it borrows money from the RBI by selling security bills to RBI. For this purpose RBI creates new currency notes and thus this is known as deficit financing or monetisation of budget deficit

Monetizing the government’s debt (called public debt) is the process of converting its debt

(whether existing or new) which is a non-monetary liability into Central BanK currency,

which is a monetary liability.

________________________________

(2) CONTROL OF CREDIT :: It controls the credit activities of the commercial banks which means it regulates increase or decrease of credit money in accordance with the monetary requirement of the country. This supply of credit within reasonable limits causes stability in price level and helps to remove problem of inflation and deflation.For this purpose Central bank often uses instruments like Bank Rate , Cash Reserve Ratio, Open Market Operation , Margin Requirement

(3) BANKER’S BANK :: As the banker to banks, the central Bank lends commercial bankshort term fundsrediscount their Billsprovides them with centralised clearing and remittances facilities andperforms all the function and have same relation which the commercial bank has

with its customers.

Commercial banks are required to keep part of their cash deposit with Central bank which is

used for

(a) Meeting liabilities of commercial bank in times of crises - Lender of Last Resort

(b) Exercising control over banking system of the country - Supervision of the Bank

(c) Settlement of mutual claim between banks - Clearing House Function

(4) SUPERVISION OF THE BANKS :: Central bank supervises and regulates the commercial banks by periodically inspection of banks and the return filed by them.The control may be related to

(a) Licensing of the commercial banks

(b) Expansion of banks i.e opening of branches in different parts of the country

(c) Merger and amalgamation of different banks

(d) Liquidation of the banks

(5) LENDER OF LAST RESORT ::The bank in temporary need of funds first approach other source of fund like call money market and if they fails to get financial accommodation from anywhere, it approaches central bank as a last resort.Central Bank advances loan to such bank against approved securities.

PROCESS :: If all the account holder of all the commercial bank in the country wants their deposit back at same time, the bank will not have enough means to satisfy the need of every account holder and thus there will be bank failure.In such cases RBI comes to help as a Guarantor and extends loan to ensure that Bank remains solvent. It is this system of Guarantee that assure individual account holder that their bank will be able to pay their money back in case of a crises and there is no need to fear. This role of Monetary authority is

known as Lender of Last resort

(6) CLEARING HOUSE FUNCTION :: Central bank acts as a clearing house for transfer

and settlement of mutual claims of the commercial banks on each other.

Since the commercial banks keep their cash reserves with the central bank, it is easier, convenient, time saving and economical to clear and settle claims between different banks by making transfer entries in their account maintained with the Central bank.

Suppose PNB receives a cheque of Rs 10000 drawn on HDFC bank and HDFC bank received a cheque of Rs 14000 drawn on PNB. The most convenient method is to debit balance of PNB with Rs 4000 and credit balance of HDFC bank.

(7) BANKERS TO THE GOVERNMENT : It acts as a banker, agent and financial

advisor

(a) As a BANKER it perform the same function for govt. which commercial banks perform for their customers.

(i) It keeps cash balances of both State and Central govt. on current account and

maintains government treasuries. Thus all government’s receipts and expenditures are recorded by the central bank.

(ii) Central bank advances temporary loans to the government that is short- term loans without any interest

(iii) Central bank carries out government transactions involving purchases or sales of foreign currencies.

(b) As a AGENTit transfers govt. fundsbuys and sells govt.securities and treasury bill on behalf of govt.It manages public debt and thus issues new loans on behalf of govt. , receives subscription , pay interest and finally repay these loansIt enforces exchange control provisions on behalf of the government.

(c) As a ADVISORIt advises govt. on economical , financial and monetary matters andIt helps govt. in formulation of policies such as those for control of inflation or deflation, foreign trade policy, devaluation or revaluation of currency

(8) CUSTODIAN OF THE NATION’S RESERVE OF FOREIGN EXCHANGE :: It is responsibility of Central bank

(a) to keep the external value of country’s currency stable , and

(b) to have a coordinated policy towards the BOP situation of the country

In order to achieve this two objectiveCentral banks maintain reserves of foreign currency .All foreign exchange transaction are routed through Central Bank.

Thus it control both receipt and payment of foreign exchange

_______________________

Besides, it represent the country in International Conferences like IMF,World Bank.Thus it helps

in promoting international trade

________________________

(9) STERILISATION BY RBI :: RBI uses its instrument of money creation for stabilising the stock of money in an economy from external shocks .

Suppose due to future growth prospect in India, foreign investors increases there investment in Indian bonds. The seller of these bonds will exchange these foreign currency for Indian rupee at Commercial Bank. The bank will further deposit these foreign currency with RBI.

This will result in

(a) Increase in RBI’s foreign exchange holding ( that is increase in assets )

(b) Increase of Commercial bank deposit with RBI by equal amount ( Increase in Liability of RBI)

However with the money multiplier , the result is increased in money supply in economy and this cause inflation

RBI will interfere to control situation by selling govt. securities through Open Market of

an amount equal to amount of foreign exchange inflow. This helps to keep

(a) the stock of high powered money and

(b) total money supply unchanged.

Thus RBI stabilises the economy against adverse external shock. This operation of

RBI is known as Sterilisation

DIFFERENCE BETWEEN CENTRAL AND COMMERCIAL BANK

CREDIT CREATION OR CREATION OF DEPOSIT MONEY

_________________

NEWLYN “ Credit creation refers to the power of commercial banks to expand secondary

deposits either

- through the process of making loans or

- through investment in securities ”

_________________________

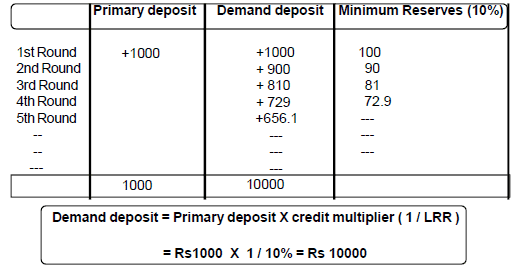

(1) PRIMARY OR CASH DEPOSITS :: The amount deposited in cash or cheque by the public in banks is called cash or primary deposits. It is also called PASSIVE DEPOSITS because in its creation bank has no contribution.Primary deposits causes an increase in both the banker’s assets as well as in

their liabilities.

(2) DERIVATIVE OR SECONDARY DEPOSITS :: Whenever a person approaches a bank for loan he is not given this loan in cash rather an account is opened in his name and he is allowed to withdraw the required amount by issuing a cheque. Such a deposit is called secondary or derivative deposit. Thus, every loan advanced by the bank creates new deposit.

Thus, it increases the total stock of money available to the community.

(3) CREDIT MULTIPLIER // MONEY MULTIPLIER // DEPOSIT EXPANSION

FORMULA :: Credit multiplier refers to the ratio of increase in total deposits to increase in primary deposits. Thus it measures the amount of money that the banks are able to create in the form of deposits with every unit of money it keeps as reserves

The inverse relation between credit multiplier and legal reserve ratio can be shown in following equation:

PROCESS OF CREDIT CREATION

(a) Let us assume that the entire commercial banking system is one unit. Let us call this one unit simply ‘’banks’.

(b) Let us also assume that all receipts and payments in the economy are routed through the banks. One who makes payment does it by writing cheque. The one who receives payment deposits the same in his deposit account.

(c) Let us suppose, the bank in our economy receives a public deposit of Rs 1000 . This is primary deposits.

(d) The banks use this money for giving loans. But the banks cannot use the whole of deposit for this purpose. It is legally compulsory for the banks to keep a certain minimum fraction of these deposits as cash and liquid assets . The fraction is called the Legal Reserve Ratio(LRR). The LRR is fixed by the central bank . Let us assume LRR = 10%

Now with public deposit the Bank need to keep a reserve equal to Rs 100 only to meet any demands arising out of its liabilities to its depositors. The bank has an excess reserve of Rs900. This sum can be extended in the form of loans and advances to the borrowers.The borrower gets a demand deposit of Rs 900 out of which bank has to keep reserve of Rs 90 and has an excess reserve of Rs 810. This sum can be further extended in the form of loans and advances to another borrowers .

This process will continue as shown

LIMITATIONS OF CREDIT CREATION :: Banks cannot create unlimited amount of credit. There are many limitations on the credit creating capacity of commercial banks.

These are as under:

(1) LEGAL RESERVE RATIO :: Capacity to create depends largely on reserve ratio.

(2) AMOUNT OF PRIMARY DEPOSITS :: There is a direct relation between the two. If the amount of Primary deposits is large, credit creation will also be large and if the amount of primary deposits is small credit will also be small

P = Rs 1000 ; r = 10 % ; D = Rs 10,000

P = Rs 2000; r = 10 % ; D = Rs 20,000

(3) CREDIT POLICY OF THE CENTRAL BANK :: Power of the commercial banks to create credit also depends on the credit policy of the central bank of the country.If the central bank pursues cheap money policy ( credit expansion policy ) then the capacity of the commercial banks to create credit is increased.On the contrary, If the central bank pursues dear money policy ( credit contraction policy ) then the power of the commercial banks to create credit is decreased.

(4) POLICY OF OTHER BANKS :: Power of one bank to create credit is very much dependent on the credit policy pursued by the other banks. If all banks function in unison they will have more power to credit . If, however, one bank expands credit and other banks do not cooperate with him, the process of credit creation will be constrained.

___________________________

SPECIAL CONCEPT’S

(Q1) Money creation by Commercial Banks raises the National Income ? How

Ans :: Commercial banks in the process of credit creation lend money mainly to investors. The rise in investment in the economy leads to rise in NY through the multiplier effect .

(Q2) What is LRR ?

Ans :: LRR has two components.

(1) CRR :: A part of the LRR is to be kept with the Central bank in form of cash and is called the Cash Reserve Ratio.

Thus under this system , banks are required to deposit with Central Bank a certain % of their net demand and time deposit.

(2) SLR :: The other part is kept by the banks themselves in form of liquid assets and is called the Statutory Liquidity Ratio.

Thus under this system , banks are required to maintain certain % of their net demand and

time deposit in form of designated liquid assets

While estimating CRR , inter - bank loans are not included in total deposit of bank where

as in SLR , these are included .Since both are determined by RBI individually , therefore each or both MAY be called

as Legal reserve ratio but mostly LRR represent CRR in India

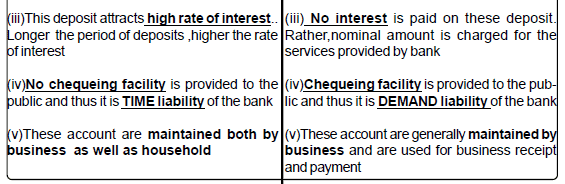

(Q3) Distinguish between time deposits and demand deposits

FAQs on Chapter 5 and 6: Money and Banking - Chapter Notes, Macro Economics, class 12 - Commerce

| 1. What is money and its functions? |  |

| 2. What are the different types of money? | |

| 3. What is the central bank and its functions? | |

| 4. What are the different types of banks? | |

| 5. What is the role of banks in the economy? | |

|

14.6K Views |

|

4.91/5 Rating |

|

Nov 15, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

Macro Economics

,mock tests for examination

,Chapter 5 and 6: Money and Banking - Chapter Notes

,Previous Year Questions with Solutions

,ppt

,practice quizzes

,Objective type Questions

,Free

,shortcuts and tricks

,class 12 - Commerce

,Extra Questions

,Macro Economics

,Sample Paper

,past year papers

,class 12 - Commerce

,video lectures

,study material

,Chapter 5 and 6: Money and Banking - Chapter Notes

,Macro Economics

,Important questions

,MCQs

,Semester Notes

,Summary

,Exam

,Chapter 5 and 6: Money and Banking - Chapter Notes

,class 12 - Commerce

,Viva Questions

;

Chapter 5 and 6: Money and Banking - Chapter Notes, Macro Economics, class 12 Free PDF Download

Importance of Chapter 5 and 6: Money and Banking - Chapter Notes, Macro Economics, class 12

Chapter 5 and 6: Money and Banking - Chapter Notes, Macro Economics, class 12

Chapter 5 and 6: Money and Banking - Chapter Notes, Macro Economics, class 12 Commerce Questions

Study Chapter 5 and 6: Money and Banking - Chapter Notes, Macro Economics, class 12 on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|