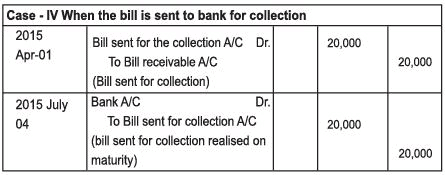

Accounting for Bills of Exchange Chapter Notes | SSC CGL Tier 2 - Study Material, Online Tests, Previous Year PDF Download

ACCOUNTING FOR BILLS OF EXCHANGE

LEARNING OBJECTIVES

After studying this chapter, students shall be able to:

- Understand the concept of Bill of Exchange and Promissory Note

- Distinguish between Bill of Exchange and Promissory

Note.

- Define Important terms of Bill Exchange and Promissory Note. Record the Accounting Treatment of Bill of Exchange under different circumstances.

- Develop the skill of identification and location of errors.

- Develop the skill of rectification and preparation of suspense A/C.

Suggested Methodology :-Illustration-cum-Explanation Method.

A Bill of Exchange and Promissory Note both are legal Instruments which facilitate the credit sale of goods by assuring the seller that the amount will be recovered after a certain period of time. Both of these are legal instruments underthe Negotiable Instruments Act, 1881.

BILL OF EXCHANGE

"A Bill of Exchange is an instrument in writing containing an unconditional order signed by the maker, directing a certain person to pay a certain sum of money only to, or the order of, a certain person or to the bearer of the instruments". Section 5 of the Negotiable instrument Act, 1881 Features of a Bill Exchange are

1. A bill of exchange must be in writing.

2. It must contain an order (and not a request) to make payment.

3. The order of payment must be unconditional.

4. The amount of bill of exchange must be certain.

5. The date of payment should be certain.

6. It must be signed by the drawer of bill.

7. It must be accepted by the drawee by signing on it.

8. The amount specified in the bill exchange in payable either on demand or on the expiry of a fixed period.

9. The amount specified in the bill is payable either to certain person or to his order or to the bearer of the bill.

10. It must be stamped as per legal requirement.

Parties to a bill exchange

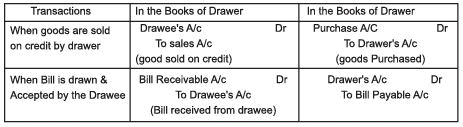

1. Drawer or maker :- Drawer is the person who makes or writes the bill of exchange. Drawer is a person who has sold goods on credit or granted credit to the person on whom the bill of exchange is drawn. The drawer is entitled to received money from the drawee (acceptor).

2. Drawee or Acceptor :- Drawee is the person on whom the bill of exchange is drawn for acceptance. Drawee is the person who purchase goods on credit or to whom credit has been granted by drawer. The drawee is liable to pay money to the creditor/drawer.

3. Payee:- Payee is the person who receives the payment from the drawee. Usually the Drawer and the payee is the same person. In the following cases, drawer and payee are two different persons.

(i) When the bill is discounted by the drawer from his bank- payee in the bank.

(ii) When the bill is endorsed by the drawer to his creditors, payee is the endorsee.

Kinds of Bills of Exchange

1) Trade Bills : Those bills that are written because of business transactions are called trade bills.

2) Accomodation Bill : Those bills that the business writes for mutual help are called accomodation bill.

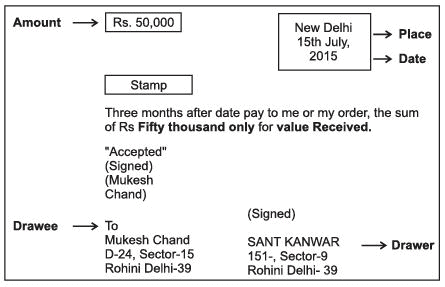

Specimen of Bill of Exchange

Note: Value Received means the bill has been issued in exchange of some consideration. These words are very important because law does not consider those agreements which have been made without consideration.

PROMISSORY NOTE

A Promissory note is an instrument in writting (not beings a bank note or a currency note) containing an unconditional undertaking signed by the maker to pay a certain sum of money only for the order of a certain person orto be the bearer of the instrument

Features of promissory note

1. There must be an unconditional promise to pay a certain sum of money on a certain date.

2. It must be signed by the maker.

3. The name of the payee must be mentioned on it.

4. It must be stamped according to its value.

PARTIES TO PROMISSORY NOTE

1. The maker: The maker is the person who makes the promise to pay the amount on a certain date. Maker of a bill must sign the promissory note before giving to the payee. 2. The payee: The payee is the person who is entitied to get the payment from the maker of promissory note. Payee is the person who has granted the credit.

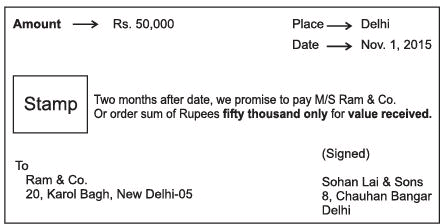

Specimen of Promissory Note

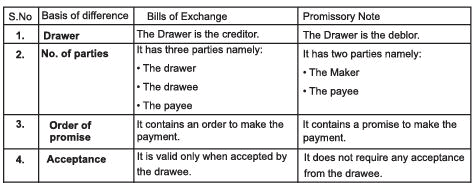

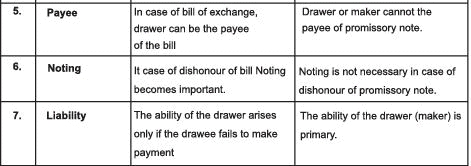

Distinction between Bills of Exchange and Promissory Note :

Important terms

1. Term of Bill :- The period intervening between the date on which a bill is drawn and the date on which it becomes due for payment is called "Term of Bill".

2. Due Date : Due date is the date on which the payment of the bill is due.

(i) In case of 'Bill at Sight':- Due date is the date on which a bill is presented for the payment

(ii) In case of'Bill afterdate':- Due Date = Date of Drawing + Term of Bill.

(iii) ln case of 'Bill after sight’ :- Due date = Date of Acceptance + Term of Bill.

3. Days of Grace: Drawee is allowed three extra days after the due date of bill for making payments. Such 3 days are known as 'Days of Grace'. It is a custom to add the days of grace.

4. Date of Maturity: The date which comes after adding three days of grace to the due date of a bill is called "Date of Maturity".

Illustration 1: A bill of exchange for Rs. 25,000 is drawn by A on B on 1 st April, 2013 for 3 Months, B accepted the bill on 10th April, 2013. Find the DUE DATE and DATE OF MATURITY if

Cash I : The bill is Bill After date.

Cash II : The bill is Bill After Sight.

Solution:

Due Date Date of Maturity

Case I- When the Bill is "Bill After date”. 1 st July 2013 4th july, 2013 Case II- When the Bill i s " Bill After Sight". 10th July 201313th July, 2013 5. Discounting of Bill: When the bill is encashed from the bank before the due date, it is known as discounting of bill. Bank deducts its charges from the amount of bill and it disburses the balance amount.

Illustration 2 : Ram sold goods to shyam for Rs. 30,000 at credit on 1 st April, 2015 and draw a bill for same, accepted by Shyam. Ram discounts the bill with his bank on 4th May 2013 @ 9% per annum find out. If maturity date is 1st July 2013.

(i) The amount of discounting charges.

(ii) The amount that Ram will receives from his bank at the time of discounting the Bill.

Solution: (i) Discounting Charges = Amount of Bill Discounted

(ii) Ram will receive from his bank Rs. 29,550 (i.e Rs. 30,000-Rs. 450) at the time of discounting the bill.

6. Endorsement of Bill : Endorsement of bill means the process by which drawer or holder of bill transfer the title of bill in favour of his/her creditors. The person transferring the title is called "Endorser" and the person to whom the bill is transferred called "Endorsee1. Endorsement is executed by putting the signature at the back of the bill.

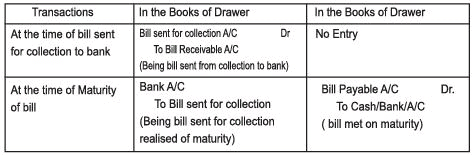

7. Bill sent for collection: It is a process when the bill is sent to back with instruction to keep the bill till maturity and collect its amount from the acceptor on the date if maturity.

8. Dishonour of Bill: When the drawee (or acceptor) of the bill fails to make payment of the bill on the date of maturity, it is called DishonourofBill.

9. Noting of Bill: To obtain the proof of dishonour of a bill, it is re-sent to the drawee through a legally authorized persons called Notary public who charges a small fee for providing this service known as Noting charges.

10. Retirement of a Bill: When the drawee makes the payment of the bill before its due date it is called 'Retirement of a bill'.

11. Renewal of a Bill: Sometimes drawee is not in the position to pay the amount of the bill on maturity. Thus drawee request to the drawer to cancel the old bill & write a new bill with interest and if drawer agree, new bill is drawn with new maturity date. This process is called the 'Renewal of Bill'. The interest may be paid in cash or may be added in the amount of the new bill.

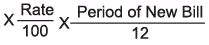

Illustration 3 : A requests B to renew his acceptance for Rs. 25,000 for 3 month together with interest @ 18% p.a. Calculate the amount of new bill drawn on A.

Solution: Interest = Amount Outstanding

= 1,125

Amount of New Bill = Rs. 25,000 + Rs. 1,125 = Rs. 26,125

Amount Outstanding = Amount of Bill cancelled - any part payment made cash at the time of renewal of bill.

ACCOUNTING TREATMENT OF BILL TRANSACTIONS

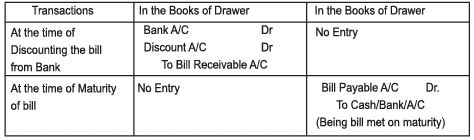

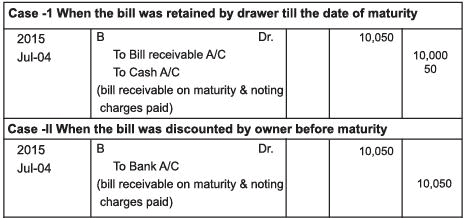

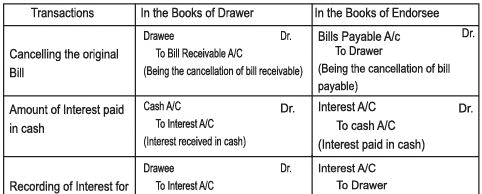

A. On the Due Date bill is Honoured:-

Note:- First Two entires are common in all the cases which we are going to discuss below.

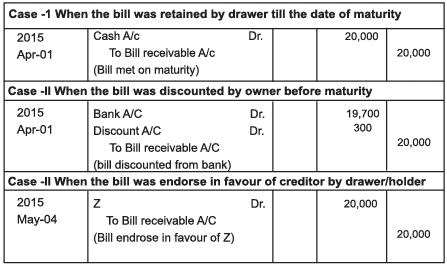

Case -1 When the bill was retained by drawer till maturity

Case -II When the bill was discounted from the bank by owner before maturity.

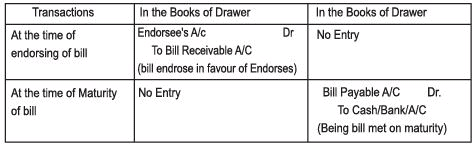

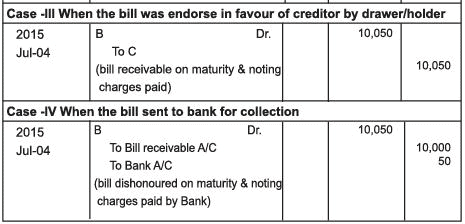

Case -III When the bill was endrose in favour of creditor by drawer/holder

Note :- In this case one additional book may be asked to maintained i.e. Endrosee Book

Case -IV When the bill is sent to bank for collection

Note:

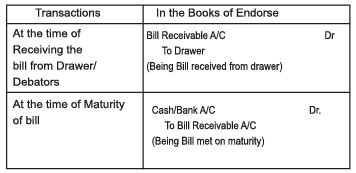

- There will be no effect in the books of Drawee either the bill is discounted from the bank or endorsed to a creditor or sent to the bank for collection. The drawee makes the payment in normal manner.

- It is only in the books of drawer where an additional entry is passed to record the effect of the above transaction.

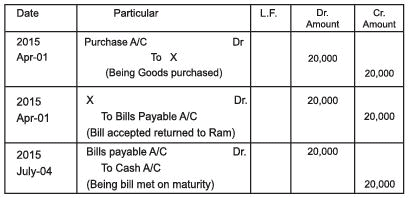

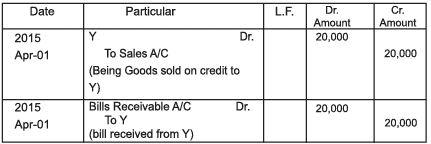

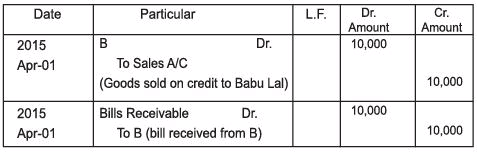

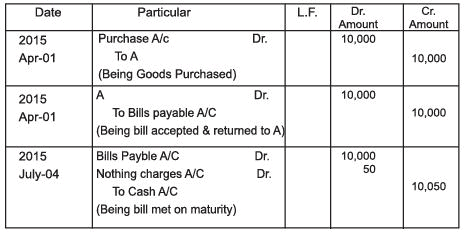

Illustration 4: X sold goods to Y on 1st April, 2015 for Rs. 20,000 on credit and drew upon him a bill for the same amount payable after 3 months. Y accepted the bill and returned it to X. On the date of maturity bill was presented to Y for the payment and he honoured it.

Pass the journal Entries in the books of both the parties when:

Case I : Bill is retained by the X till the date of maturity.

Case II : Bill is discounted by X from his bank on 4th April @ 6% per annum.

Case III: Bill is sent to Bank for collection on 1st July, 2013.

Also record the Journal Entries in the books of Z (Case-Ill) In the Book of Y (Drawee)

Note: In the books of drawee these three entries remains same in all the cases

In the Book of (X)

1. First two entries passed on April 1,2013 will be same in the books of X (Drawer) in all the 4 cases.

In the Book of Z (Endorsee)

NO ENTRY is passed on the date of maturity in the books of drawer if.

- Bill is discounted from the bank; or

- Bill is endorsed in favour of creditor.

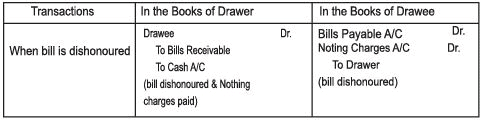

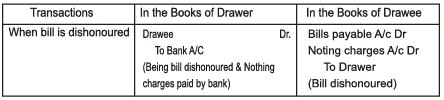

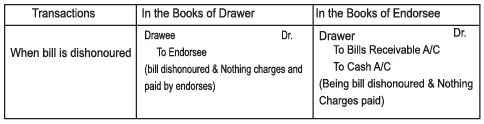

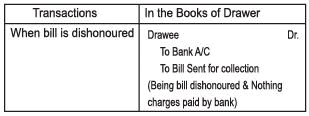

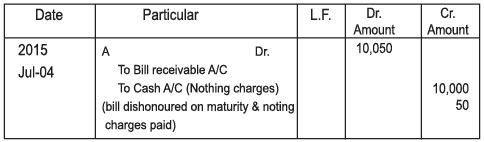

B. When Bill is dishonoured on the date of maturity.

Case I: Bill is retained by the drawertill the date of maturity.

Note: Entry passed in the book of Drawee will be SAME in all cases.

Case I : When the bill was discounted by owner before maturity

Case III: When the bill was entered in favour of creditor by drawer/holder

Case IV When the bill is sent to bank for collection

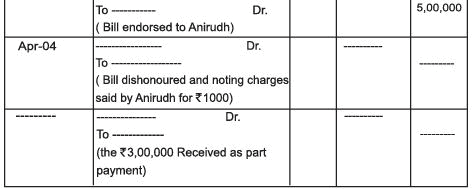

Illustration 5 : A sold good to B on April 1,2013 for Rs. 20,000 oncred it and drew upon him a bill for the same amount payable after 3 months. B accepted the bill and returned it to A. On the due date bill was dishonoured.

Case I : Bill is retained by A till the date of maturity.

Case II : Bill is discounted by A from his bank on 4th April, 2013 @ 6% perannum

Case III: Bill is endorsed in favour of C on April, 4th, 2013

Case IV : Bill is spent to bank for collection on July 1,2013

( Note : Nothing charges paid 150 in each case)

Solution

In the Book of A (Drawer)

Note: 1. First two entries passed on April 1,2015 will be same in the books of X (Drawer) in all 4 Cases

In the Book of C (Endorsee)

Note: In the books of drawee following three entries remains same in all the cases.

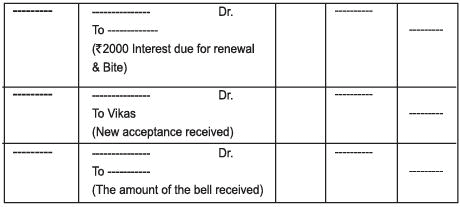

C. Renewal of a Bill

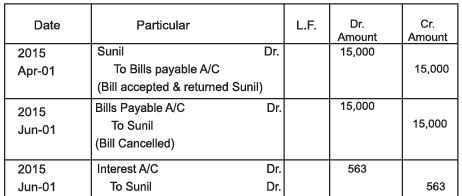

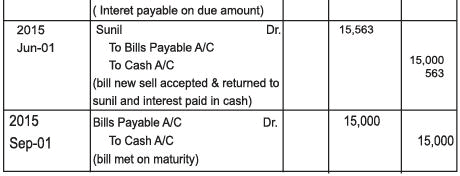

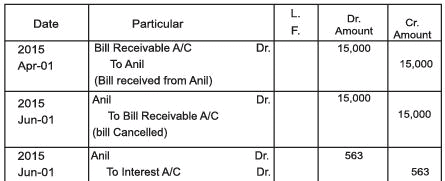

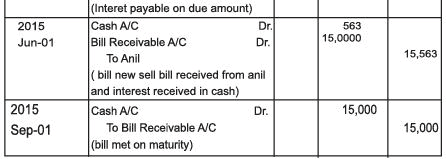

Illustration 6: On 1st April,2015 Anil accepts a bill drawn by Sunil for 2 months for Rs. 15,000 in payment of a debt. Before the date of maturity Anil request sunil that he is not in the position to pay the due amount, so kindly cancel the bill & draw a new bill for the amount due 3 months Sunil agreed to draw a new bill for 3 months but he charged interest @ 15% per annum in cash. This bill is duly met on the maturity. Pass Journal entires in the books of both the parties.

Solution: In the Book of Anil (Drawee)

In the Book of Sunil (Drawer)

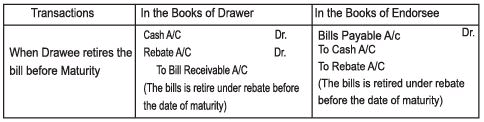

D. Retiring a bill under Rebate

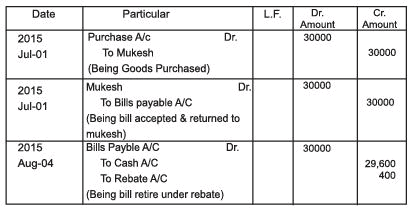

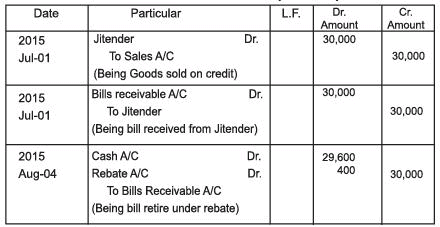

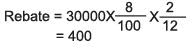

Illustration 7: Mukesh sold goods to Jitender on July 1,2015 for Rs. 30,000 and drew a bill for the same amount for 3 months. Jitender accepted the bill and returned it to Mukesh, Jitender retired his acceptance on 4th August, 2015 under rebate of 8% per annum. Give Journal entries in the books of Mukesh and Jitender.

Solution: In the Book of JITENDER (Drawee)

In the Book of Mukesh (Drawer)

POINTS TO REMEMBER

1. While calculating Date of Maturity the following point must be considered:

(i) In case "Bill at Sight" or "Bill on demand" 3 days of grace are NOT allowed.

(ii) When the term of bill is mentioned in no. of days, then

- Date of drawing the bill is not included.

- Date of payment is included in determining date of maturity.

- If date of maturity falls on a day which is public holiday; the maturity date of the bill shall be "PRECEEDING DAY'.

- If maturity date is on an emergent holiday declared under the Negotiable Installment Act. 1881, the next working day immediately after the holiday will be considered as the date of maturity.

2. When the period is stated in months the date of maturity shall be calculated in terms of calender months ignoring the no. of days in a month.

EXCERSICE

Q. No.:-1 Asold goods to B on 1 st May 2015 for Rs. 20,000 and drew 3 bills on B for

(i) 7,000 payable 1 months

(ii) 7,500 payable after 2 months and

(iii) 5,500 payable after 3 months. All the bills duly accepted. The first bill is retained by A till maturity. The second bill is endorsed to C (A Creditor of A) immediately after receiving and third bill was discounted from bank for Rs. 5,250 on 5th May 2015. All the 3 bills were duly met on maturity. Pass entires in the books of Aand B.

Q.No. 2 A sold goods to B on May 1 st, 2015 for Rs. 30,000 on credit and drew upon him a bill for the same amount payable after 2 months. B accepted the bill and returned it to A. On date of maturity, B fails to make payment of bill. Noting charges amounted to Rs. 100. Pass Journal Entires in the books of Aand B if.

Case 1: A retains the bill till the date of maturity and also paid the noting charges.

Case 2: A discounts the bill from his bank on 4th june @ 12% per annum. Noting charges has been paid by bank.

Case 3: A endorses the bill in favour of C on June 1 ,C paid the noting charges.

Case 4: A sent the bill to his bank for collection on July 1, Bank and paid the noting charges.

Q.No.:-3 P sold goods to Q for Rs. 10,000 on Janauary 1,2015 and on the same day draws a bill on Q for the same amount for three months. Q accept it and returns it to P, who discounts it on 10th January, 2015 with his bank for Rs, 9850. The acceptance is dishonoured on the due date and the Noting charges were paid by bank being Rs.50. On 4th April, Q paid Rs. 2,050 (including Nothing charges) in cash and accepted new bill at 3 months for the amount togetherwith interest@ 12% per annum. Make Journal Entries in the books of P and Q to record transaction.

Q.No.:-4 Rajiv sold goods to Pankaj for Rs. 40,000 on January 1st, 2015. On the same date Rajiv drew a bill of the same amount for 3 months on Pankaj. The bill was accepted by Pankaj. Rajiv discounted the bill with his bank on 4th February, 2015 @ 12% per annum. On date of maturity, the bill was dishonoured and Noting charges amounted Rs. 200. Pankaj agreed to Pay Rs. 10,200 and accepted another bill for the remaining amount for 3 months together with inte rest @ 9 % perannum . On due date Pankaj make the payment.

Give Journal Entries in the books of Rajiv and Pankaj.

Q.No.:-5 On 1st March 2015, Amit drew three bills of exchange on his debtor Shyam. First for Rs. Rs. 7000 for 1 month, second for Rs. 8,000 for two months and third for Rs. 10,000 for 4 months. Shyam accepted these bills.

Amit endorsed the first bill to his creditor, Ram in full settlement of his account Rs. 7,100. This bill was met on maturity on 1st April, amit discounted the second bill from his bank for Rs. 7,800. This bill was dishonoured on due date and bank paid Rs. 100 towards noting charges. Amit drew another bill on shyam for the amount due along with Rs. 200 towards interest for 2 months for which shyam agreed.

The third bill was paid by shyam under rebate of 12% p.a. One month prior to date of maturity. The fourth bill was lodged with bank for collection and it was duly met. Pass neccessary Journal entries in the books of amit and shyam.

Q.No. 6: What Journal Entry will be passed in the banks of drawer & drawee at the time of dishonour of bill in the following cases:-

(i) It bill of ? 10,000 was discounted from bank and noting charges paid by the bank were? 100.

(ii) If B/R of ? 10,000 was endorsed in favour of C. Noting charges paid by the C were ? 100.

(iii) If B/R is retained with retained with drawer and noting charges were ? 100.

Q.No7: Journalise the following in the books of Mohan under following circumstances:-

(i) A bill of ? 4500 is drawn by Mohan & co. on Ram & Co. and accepted by later.

(ii) If bill is retained till the date and realised on maturity.

(iii) He discounted the bill with Bank of Baroda for ? 4380.

Q. No8: Ashok sold goods to Susheem for ? 2,00,000 on 1st July 2015. Susheem immediately accepted the bill for? 1,20,000 only for the 3 month and send the balance by a Cheque. A discounted the bill with his bank on 4 August 2015 at 5% p.a. On the due date, the bill was dishonoured, bank paying ? 500 as noting charges. Susheem paid cash ? 40,000 and accepted another bill for the due amount for the further period of 2 months together with interest at 10% p.a. On due date bill was honoured. Give journal Entries in the books of Ashok & Susheem.

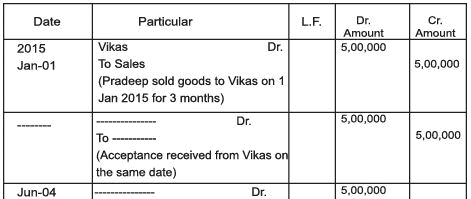

Q .No 9 : Journal of ----------

|

1334 videos|1437 docs|834 tests

|

FAQs on Accounting for Bills of Exchange Chapter Notes - SSC CGL Tier 2 - Study Material, Online Tests, Previous Year

| 1. What is a bill of exchange? |  |

| 2. How is a bill of exchange accounted for? | |

| 3. How does discounting a bill of exchange work? | |

| 4. What is the difference between a bill of exchange and a promissory note? | |

| 5. What are some advantages of using bills of exchange in international trade? | |

Viva Questions

,Online Tests

,Accounting for Bills of Exchange Chapter Notes | SSC CGL Tier 2 - Study Material

,Exam

,Important questions

,Previous Year

,Semester Notes

,Summary

,Previous Year

,shortcuts and tricks

,Online Tests

,Online Tests

,past year papers

,practice quizzes

,Accounting for Bills of Exchange Chapter Notes | SSC CGL Tier 2 - Study Material

,Free

,Previous Year

,study material

,mock tests for examination

,video lectures

,ppt

,Extra Questions

,Objective type Questions

,Previous Year Questions with Solutions

,Accounting for Bills of Exchange Chapter Notes | SSC CGL Tier 2 - Study Material

,Sample Paper

,MCQs

;

Chapter Notes - Accounting for Bills of Exchange Free PDF Download

Importance of Chapter Notes - Accounting for Bills of Exchange

Chapter Notes - Accounting for Bills of Exchange

Chapter Notes - Accounting for Bills of Exchange SSC CGL Questions

Study Chapter Notes - Accounting for Bills of Exchange on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!