Revenue (Producer Behaviour and Supply), Class 12, Economics Chapter Notes - Commerce PDF Download

Revenue

Revenue:- Money received by a firm from the sale of a given output in the market.

Total Revenue: Total sale receipts or receipts from the sale of given output.

TR = Quantity sold × Price (or) output sold × price

Average Revenue: Revenue or Receipt received per unit of output sold.

- AR = TR / Output sold

- AR and price are the same.

- TR = Quantity sold × price or output sold × price

- AR = (output / quantity × price) / Output/ quantity

- AR= price

AR and demand curve are the same. Shows the various quantities demanded at various prices.

Marginal Revenue: Additional revenue earned by the seller by selling an additional unit of output.

- MRn = TR n - TR n-1

- MR n = Δ TR n / Δ Q

- TR = ∑ MR

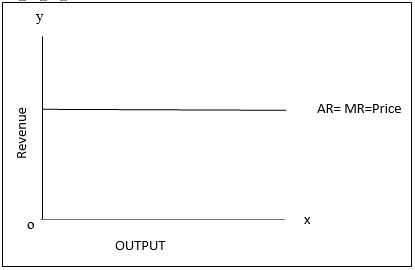

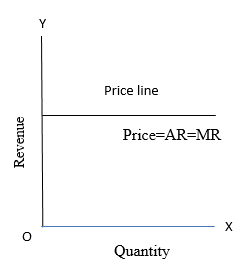

Relationship between AR and MR (when price remains constant or perfect competition)

Under perfect competition, the sellers are price takers. Single price prevails in the market. Since all the goods are homogeneous and are sold at the same price AR = MR. As a result AR and MR curve will be horizontal straight line parallel to OX axis. (When price is constant or perfect competition)

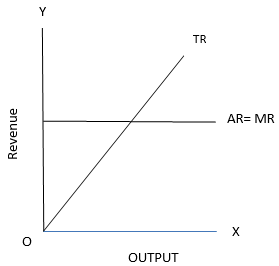

Relation between TR and MR (When price remains constant or in perfect competition)

When there exists single price, the seller can sell any quantity at that price, the total revenue increases at a constant rate (MR is horizontal to X axis)

Relationships between AR and MR under monopoly and monopolistic competition (Price changes or under imperfect competition)

- AR and MR curves will be downward sloping in both the market forms.

- AR lies above MR.

- AR can never be negative.

- AR curve is less elastic in monopoly market form because of no substitutes.

- AR curve is more elastic in monopolistic market because of the presence of substitutes.

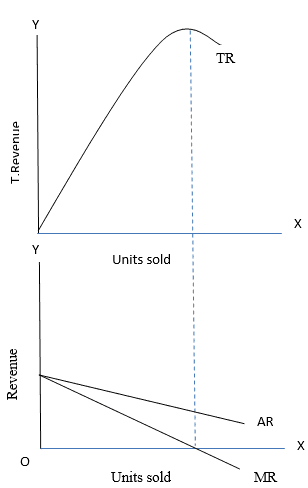

Relationship between TR and MR. (When price falls with the increase in sale of output)

- Under imperfect market AR will be downward sloping – which shows that more units can be sold only at a less price.

- MR falls with every fall in AR / price and lies below AR curve.

- TR increases as long as MR is positive.

- TR falls when MR is negative.

- TR will be maximum when MR is zero.

PRODUCER’S EQUILIBRIUM

It is that situation in which a producer is getting maximum amount of projects.

There are two different approaches to study producer’s equilibrium situation: -

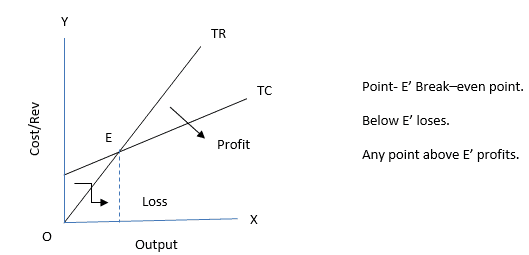

TR and TC approach- Producer is in equilibrium when difference between TR and TC is maximum

MC and MR approach

Marginal Cost and Marginal Revenue approach

à According to this approach the producer will be in equilibrium when the following conditions are satisfied.

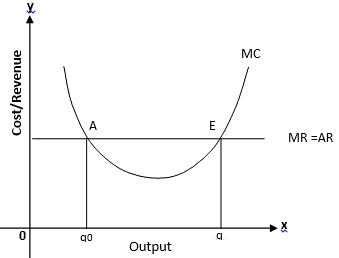

- MC should be rising i.e. MC curve should intersect MR curve from below. MC>MR after the equilibrium point

- MC = MR

From the above given diagram, it is clear that equilibrium is not established at point A. The producer has got still the opportunity to increase the level of output. Thus, equilibrium is established at point E where:

- MC is rising and MC is equal to MR. Therefore the equilibrium level of output determined is oq.

Break-even point: It is that point where TR = TC or AR=AC. Firm will be earning normal profit.

Shut down point : A situation when a firm is able to cover only variable costs or TR = TVC

Formulae at a glance:

- TR = price or AR × Output sold or TR = ∑ MR

- AR (price) = TR ÷ units sold

- MR n = MR n – MR n-1

FAQs on Revenue (Producer Behaviour and Supply), Class 12, Economics Chapter Notes - Commerce

| 1. What is revenue in economics? |  |

| 2. How is total revenue affected by changes in price? | |

| 3. What is the relationship between marginal revenue and total revenue? | |

| 4. How do fixed costs and variable costs affect revenue? | |

| 5. What is the difference between total revenue and profit? | |

practice quizzes

,mock tests for examination

,study material

,Revenue (Producer Behaviour and Supply)

,shortcuts and tricks

,Class 12

,Revenue (Producer Behaviour and Supply)

,video lectures

,Economics Chapter Notes - Commerce

,MCQs

,Extra Questions

,Important questions

,Sample Paper

,Previous Year Questions with Solutions

,Economics Chapter Notes - Commerce

,Semester Notes

,Economics Chapter Notes - Commerce

,Summary

,Free

,past year papers

,Objective type Questions

,Viva Questions

,ppt

,Class 12

,Class 12

,Revenue (Producer Behaviour and Supply)

,Exam

;

Chapter Notes - Revenue (Producer Behaviour and Supply), Class 12, Economics Free PDF Download

Importance of Chapter Notes - Revenue (Producer Behaviour and Supply), Class 12, Economics

Chapter Notes - Revenue (Producer Behaviour and Supply), Class 12, Economics

Chapter Notes - Revenue (Producer Behaviour and Supply), Class 12, Economics Commerce Questions

Study Chapter Notes - Revenue (Producer Behaviour and Supply), Class 12, Economics on the App

|

© EduRev

|

Education Revolution

|

|