Control Over Material, Stock Verification & Inventory - Material Cost, Cost Accounting | Cost Accounting - B Com PDF Download

Control over Material

Control over material is essential for different reasons By and large, materials are the equivalent of cash and therefore pilfering and theft may occur quite often if effective control is not exercised. Prevention of material from deterioration and waste is also necessary. It is also important to eliminate obsolete stocks with the consequence easing of storage space and storage costsMoreover, control over materials is necessary to prevent extra expenditure on excessive purchase of materials and improper use of material. And above all, regular supply of materials to the production departments would help production on schedule. It will also ensure preparation of accurate statements of the value of material consumed by each department/job and final statements prepared according to their needs.

From the accounting point of view, the following are some important requirements of the effective material control;

- That no material is purchased without proper authority.

- That the quantity of material purchased is in factreceived.

- That there are proper storage facilities.

- That no material is issued without proper authorization and the purpose for which the material is required is recorded.

- That the accounts provide a running balance of the value of the materials on hand.

Replenishment of Stock

Materials are received and issued by the storekeeper to different production departments. One important duty of a storekeeper is the restocking of stores in order to ensure efficient functioning of the stores department and steady flow of materials to the production departments. The inflow and outflow of materials has to be regulated in such a manner that neither production is adversely effected due to want of materials nor there unnecessary blocking of capital funds due to overstocking of raw materials.

This implies that there is always a limit to the minimum and maximum quantity of materials or stock in the store. The storekeeper is to requisition for stock for replenishment in time so as to ensure honoring of requisition slips from production departments. Replenishment of stock therefore implies as ‘taking steps for the fresh purchase of those stocks which have been exhausted and for which requisitions are to be honored in future’.

In order to ensure that the optimum quantity of materials is purchased and stock—neither less nor more, the storekeeper applies scientific techniques of materials management. Fixing of certain levels for each item of materials is one of such techniques.

The following levels are generally fixed.

- Order level.

- Maximum level.

- Minimum level.

- Danger level.

Order Level

It is also known as Re-ordering level in relation with an item of stock. It is the point at which it becomes essential to initiate purchase orders for its fresh supplies. Normally, re-ordering level is a point between the maximum and the minimum stock levels. Fresh orders must be placed before the actual stocks touch the minimum level, so as to take care of lapse in time the placing of the order and the receipt of materials in stores. Following are the factors that are taken into account for fixing re-order level.

1. The maximum consumption.

This is the maximum quantity of the material that is expected to be consumed in a day or in a week or in a month time.

2. Lead time

This is the estimated time period in number of days or in weeks or in months, which is necessarily required for placing an order and finally receiving it in the stores. There might be different lead times for different consumptions. For example; more time will be required for maximum consumption comparing with the time required for minimum or average consumption.

3. Economic order quantity.

Details of the economic order quantity will be covered in the next lesson; here this will be sufficient to learn that it is the level where the ordering quantity will be most economical. Although EOQ is not required while calculating the order/re-order level but one must keep in mind the EOQ of the item for determining the order level. Most of the times where purchases are made according to the EOQ, the order level is half or the EOQ.

Formula Order Level/reorder level /Reorder point = Maximum Consumption x Lead Time (maximum)

Maximum Stock Level

The maximum stock level indicates the maximum quantity of an item of material which can be held in stock at any time. The maximum stock level is fixed by taking into consideration the following factors:—

1. Minimum rates of consumption.

This is the minimum quantity of the material that is expected to be consumed in a day or in a week or in a month time.

2. The lead time.

This is the estimated time period in number of days or in weeks or in months, which is necessarily required for placing an order and finally receiving it in the stores. There might be different lead times for different consumptions. For example; more time will be required for maximum consumption comparing with the time required for minimum or average consumption.

3. Economic ordering quantity.

Details of the economic order quantity will be covered in the next lesson; here this will be sufficient to learn that it is the level where the ordering quantity will be most economical.

4. Availability of funds,

5. Availability of storage space.

6. Risk of obsolescence, depletion, evaporation and materialwaste,

7. Future fluctuations of price of materials.

8. Cost of storage and insurance.

9. The nature of material—seasonal supplies etc.

10. Any restrictions imposed by the government or restrictions in respect of import of materials.

The maximum stock can be calculated by applying the following formula.

Formula

Reorder level – (Minimum consumption x Lead time) + EOQ

Putting the formula elements of reorder level over here the result will be like this:

(Maximum consumption x Lead time) – (Minimum consumption x Lead time) + EOQ

[(Maximum consumption - Minimum consumption) Lead time]+ EOQ

Minimum Level;

This represents the quantity below which the stock of any item should not be allowed to fall. In other words, an enterprise must maintain minimum quantity of stock so that the production is not adversely affected due to non-availability of materials.

The minimum stock level is fixed by taking into account:

1. Re-order level.

2. Lead time.

This is the estimated time period in number of days or in weeks or in months, which is necessarily required for placing an order and finally receiving it in the stores. There might be different lead times for different consumptions. For example; more time will be required for maximum consumption comparing with the time required for minimum or average consumption.

3. Average rate of consumption.

This is the minimum quantity of the material that is expected to be consumed in a day or in a week or in a month time.

Formula

Reorder level— (Average consumption x lead time)

Putting the formula elements of reorder level over here the result will be like this:

(Maximum Consumption – Average Consumption) x Lead time

Danger Level

The danger level is below the minimum level and represents a stage where immediate steps are taken for getting stock replenished. When the stock reaches danger level it is indicative that if no emergency steps are taken to restock the materials, the stores will be completely exhausted and normal production stopped. Generally, the danger level of stock is fixed above the minimum level.

The danger stock level is fixed by taking into account:

- Average Consumption.

- Emergency Lead Time.

Formula Average

consumption x Emergency time

Stock Verification

Stock verification is the process of checking/verifying the stock physically held in warehouse in terms of quantity and quality. It is required to provide an audit of existing stock valuation. It is also the source of stock discrepancy information. Stock verification may be performed as an intensive annual check or may be done continuously by means of a cycle count. In short it refers to the process of physically checking the quantities of different items of material available in stock in a warehouse and tallying these physically available quantities with the quantities shown in stores stock records.

Depending on timing of physical check of the quantity in stock, different types of stock verification can be designed. The common types of stock verification systems are as under:

Periodic stock verification: It is done at predetermined periodical intervals, e.g. many businesses do their stock verification just before the financial year end (i.e. March 31) so that the final accounts of the business will reflect the accurate position of stocks. In this system all items in the stock is divided in 12 groups and a particular month is fixed for stock verification of the items in the group. Consequently every item in store gets verified once a year, in different month. It allows the workload of stock verification to be divided evenly throughout the year.

Perpetual stock Verification: In this system the stock of every item is verified every time there is an issue or receipt transaction for the item. This means a much stricter control over physical stock.

Need for Stock Verification:

Stock Verification is the physical counting of stock. Where counting is not possible, measuring or weighing is done. The results of such physical checking are systematically recorded.

Stock verification is necessary because:

(a) It minimizes pilferage and fraudulent practices,

(b) It ensures accuracy and usefulness of documents,

(c) It brings about a reconciliation of the stock records and documents.

(d) It identifies areas for more disciplined document control and

(e) It backs up the balance sheet stock figures Stock verification is the task of the materials audit department. Verification may be continuous or periodical.

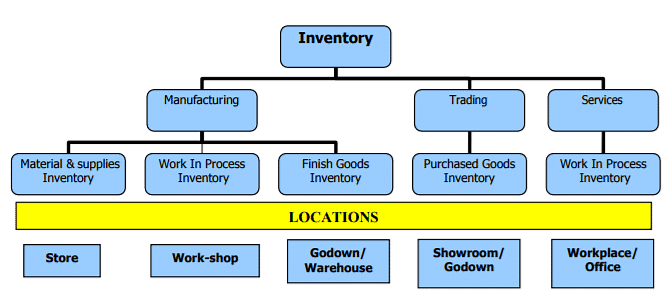

Inventory

It is the cost held in material & supplies, work in process and finished goods that will provide economic benefits in future, it is also known as stock. Adjustment for inventories is pivotal in calculation of cost of goods sold. The basic reason for its adjustment is that profit and loss account is prepared on the basis of accrual concept. Adjustments of opening and closing inventories in the cost of production (for manufacturing entities), cost of purchases (for trading entities) is essential to match the cost with its revenue.

For manufacturing entities inventories are classified into three categories:

- Material and suppliesinventory

- Work in processinventory

- Finished goods inventory

|

106 videos|173 docs|18 tests

|

FAQs on Control Over Material, Stock Verification & Inventory - Material Cost, Cost Accounting - Cost Accounting - B Com

| 1. What is material control and why is it important in inventory management? |  |

| 2. What is stock verification and why is it necessary? | |

| 3. How does inventory management impact material costs? | |

| 4. What is cost accounting and how does it relate to inventory management? | |

| 5. What are some common inventory management techniques used to control material costs? | |

|

15.9K Views |

|

4.90/5 Rating |

|

Dec 19, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Cost Accounting | Cost Accounting - B Com

,Sample Paper

,study material

,Stock Verification & Inventory - Material Cost

,Control Over Material

,Semester Notes

,Extra Questions

,Control Over Material

,past year papers

,Stock Verification & Inventory - Material Cost

,Previous Year Questions with Solutions

,Cost Accounting | Cost Accounting - B Com

,Cost Accounting | Cost Accounting - B Com

,mock tests for examination

,shortcuts and tricks

,Stock Verification & Inventory - Material Cost

,Control Over Material

,Exam

,Summary

,ppt

,MCQs

,Free

,Viva Questions

,Objective type Questions

,practice quizzes

,Important questions

,video lectures

;

Control Over Material, Stock Verification & Inventory - Material Cost, Cost Accounting Free PDF Download

Importance of Control Over Material, Stock Verification & Inventory - Material Cost, Cost Accounting

Control Over Material, Stock Verification & Inventory - Material Cost, Cost Accounting Notes

Control Over Material, Stock Verification & Inventory - Material Cost, Cost Accounting B Com Questions

Study Control Over Material, Stock Verification & Inventory - Material Cost, Cost Accounting on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|