Depreciation - (Part - 6) | Accountancy Class 11 - Commerce PDF Download

Page No 14.53:

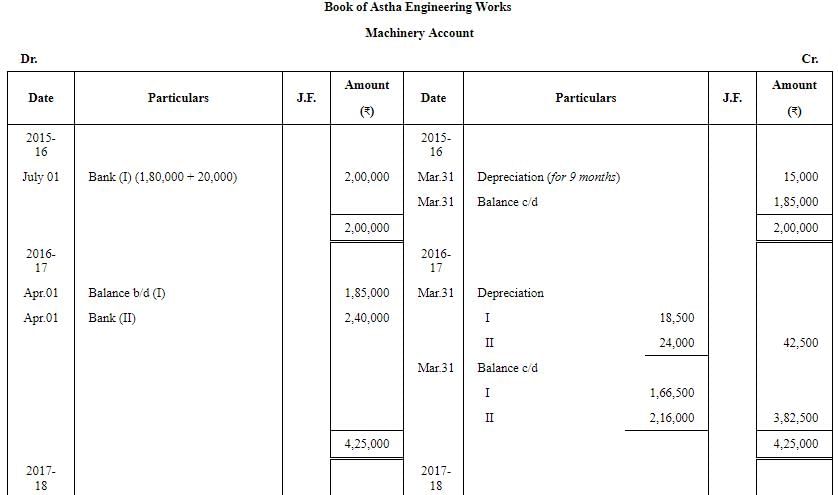

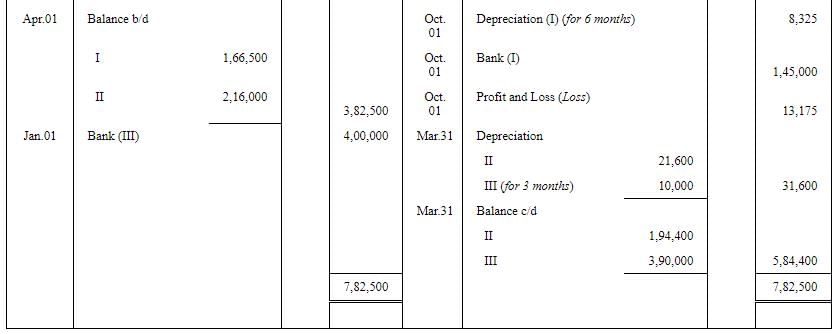

Question 26: Astha Engineering Works purchased a machine on 1st July, 2015 for ₹ 1,80,000 and spent ₹ 20,000 on its installation.

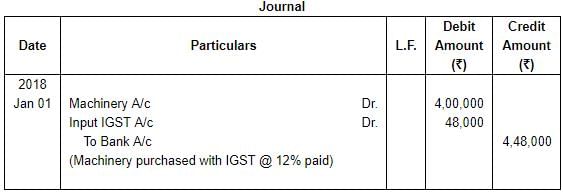

On 1st April, 2016, if purchased another machine for ₹ 2,40,000. On 1st October, 2017, the machine purchased on 1st July, 2015 was sold for ₹ 1,45,000 plus CGST and SGST @ 6% each. On 1st January, 2018, another machine was purchased for ₹ 4,00,000 plus IGST @ 12%.

Prepare the Machinery Account for the years ended 31st March, 2016 to 2018 after charging Depreciation @ 10% p.a. by Diminishing Balance Method. Accounts are closed on 31st March every year.

ANSWER:

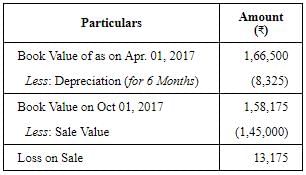

Working Note:

Working Note:

(1) Calculation of profit or loss on sale of Machine I:

(2) Journal entry for purchase with GST

Page No 14.53:

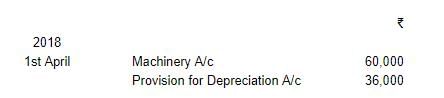

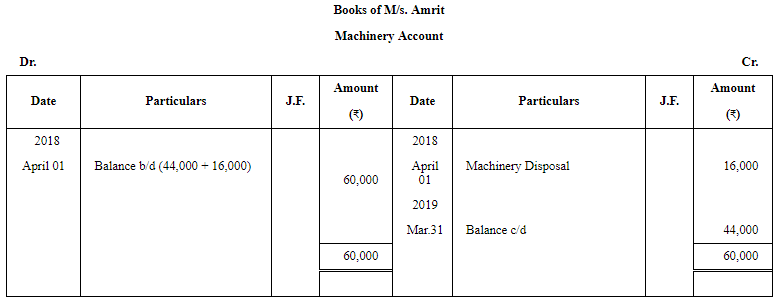

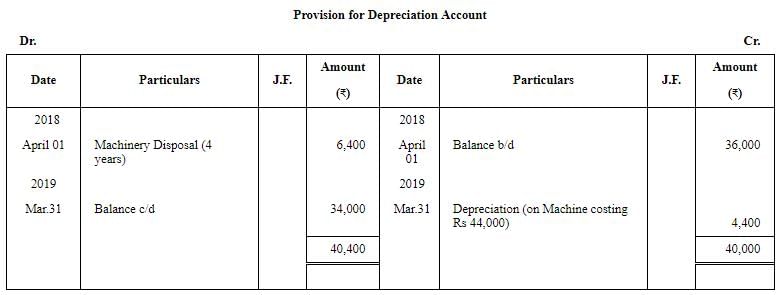

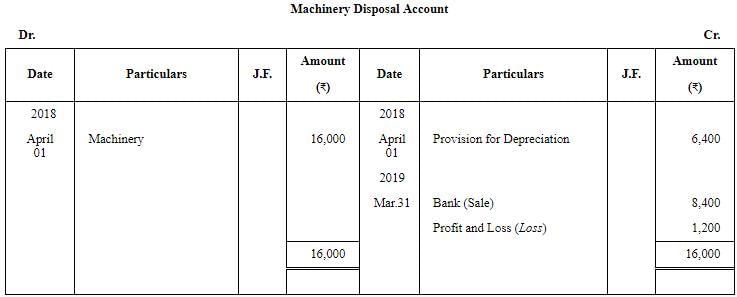

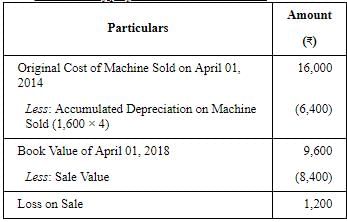

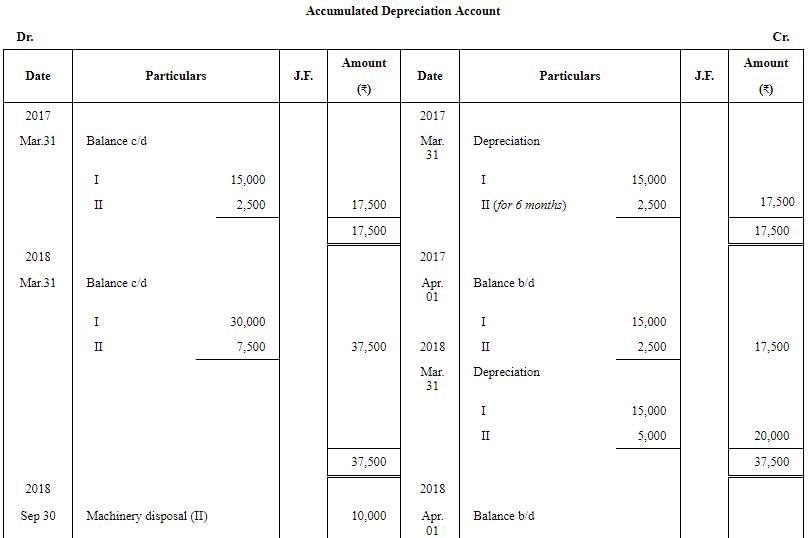

Question 27: Following balances appear in the books of M/s. Amrit as on 1st April, 2018:

On 1st April, 2018, they decided to dispose off a machinery for ₹ 8,400 which was purchased on 1st April, 2014 for ₹ 16,000.

You are required to prepare the Machinery Account, Provision for Depreciation Account and Machinery Disposal Account for the year ended 31st March, 2019. Depreciation was charged at 10% p.a on Cost following Straight Line Method.

ANSWER:

Working Note

1. Calculation of profit or loss on Machine Sold:

Page No 14.54:

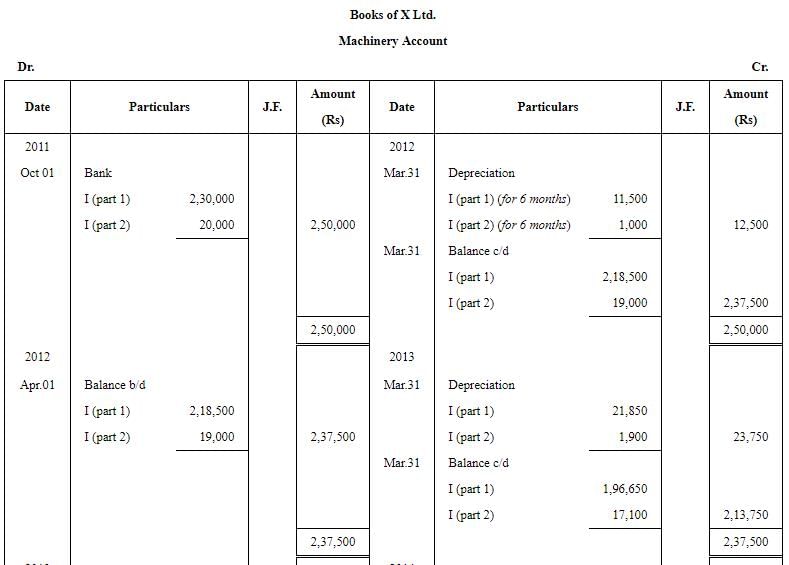

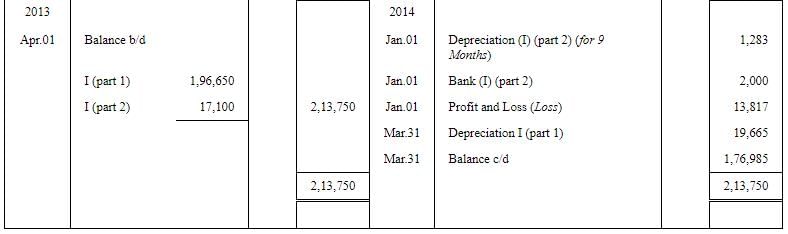

Question 28: On 1st October, 2011, X Ltd. purchased a machinery for ₹ 2,50,000. A part of machinery which was purchased for ₹ 20,000 on 1st October, 2011 became obsolete and was disposed off on 1st January, 2014 (having a book value ₹ 17,100 on 1st April, 2013) for ₹ 2,000. Depreciation is charged @ 10% annually on written down value. Prepare Machinery Disposal Account and also show your workings. The books being closed on 31st March of every year.

ANSWER:

Page No 14.54:

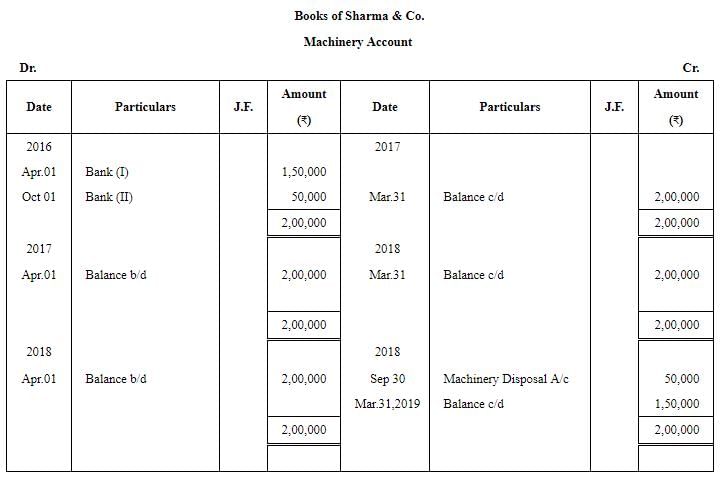

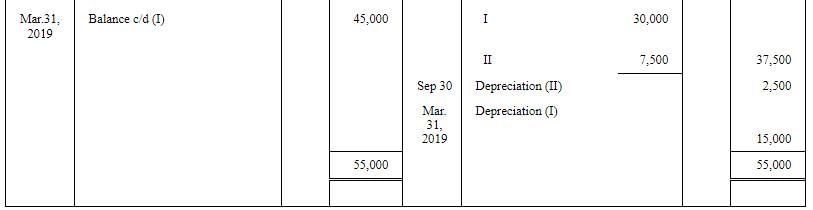

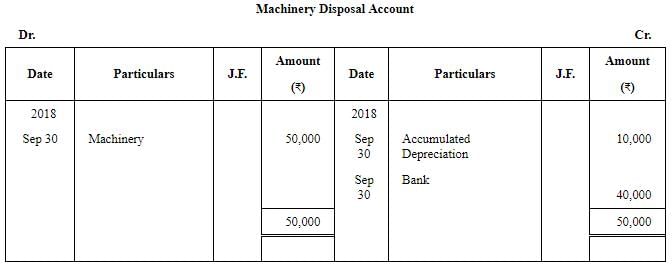

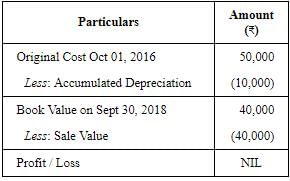

Question 29: Sharma & Co. whose books are closed on 31st March, purchased a machinery for ₹ 1,50,000 on 1st April, 2016, Additional machinery was acquired for ₹ 50,000 on 1st October, 2016. Certain machinery which was purchased for ₹ 50,000 on 1st October, 2016 was sold for ₹ 40,000 on 30th September, 2018.

Prepare the Machinery Account and Accumulated Depreciation Account for all the years up to the year ended 31st March, 2019. Depreciation is charged @ 10% p.a. on Straight Line Method. Also, show the Machinery Disposal Account.

ANSWER:

Working note

1. Calculation of Profit or Loss on sale of Machine II:

|

64 videos|152 docs|35 tests

|

FAQs on Depreciation - (Part - 6) - Accountancy Class 11 - Commerce

| 1. What is depreciation in commerce? |  |

| 2. How is depreciation calculated? | |

| 3. What is the importance of depreciation in accounting? | |

| 4. How does depreciation affect financial statements? | |

| 5. Can depreciation be reversed or reversed? | |

|

4.62/5 Rating |

|

Dec 22, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

Important questions

,Sample Paper

,Objective type Questions

,Exam

,ppt

,mock tests for examination

,MCQs

,past year papers

,Viva Questions

,video lectures

,Depreciation - (Part - 6) | Accountancy Class 11 - Commerce

,Free

,Semester Notes

,Previous Year Questions with Solutions

,Depreciation - (Part - 6) | Accountancy Class 11 - Commerce

,Extra Questions

,practice quizzes

,shortcuts and tricks

,Depreciation - (Part - 6) | Accountancy Class 11 - Commerce

,study material

,Summary

;

Depreciation - (Part - 6) Free PDF Download

Importance of Depreciation - (Part - 6)

Depreciation - (Part - 6) Notes

Depreciation - (Part - 6) Commerce Questions

Study Depreciation - (Part - 6) on the App

|

© EduRev

|

Education Revolution

|

|