Final accounts of life Insurance Companies - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com PDF Download

The insurance companies are required to prepare their financial statements i. e. Revenue Account, Profit and Loss Account and Balance Sheet according to the Insurance Regulatory and Development Authority (Preparation of Financial Statements and Auditors’ Report of Insurance Companies) Regulations, 2002.

Insurers carrying on Life Insurance Business should comply with the requirements of Schedule A of the Regulations which among other things, gives the following Forms:

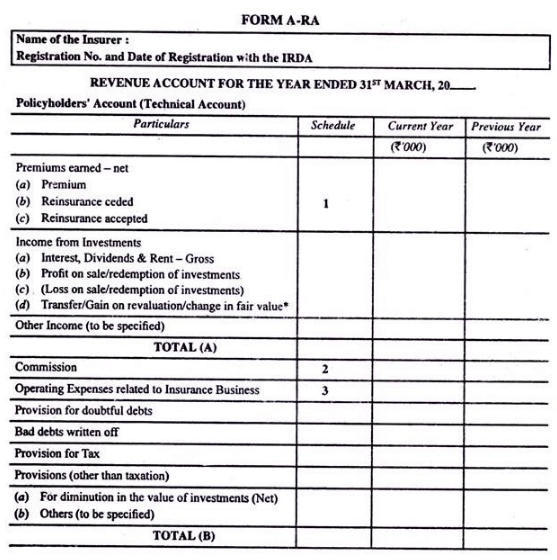

Revenue Account – Form A – RA

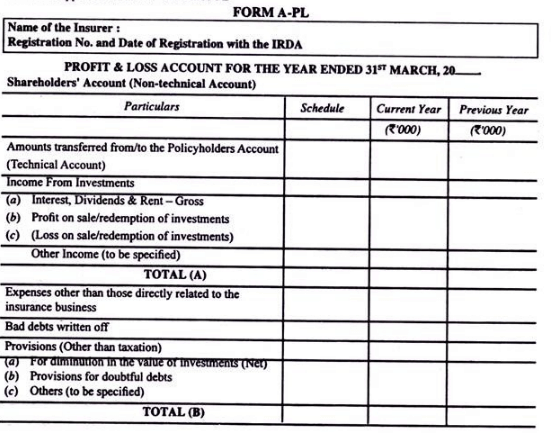

Profit and Loss Account – Form A – PL

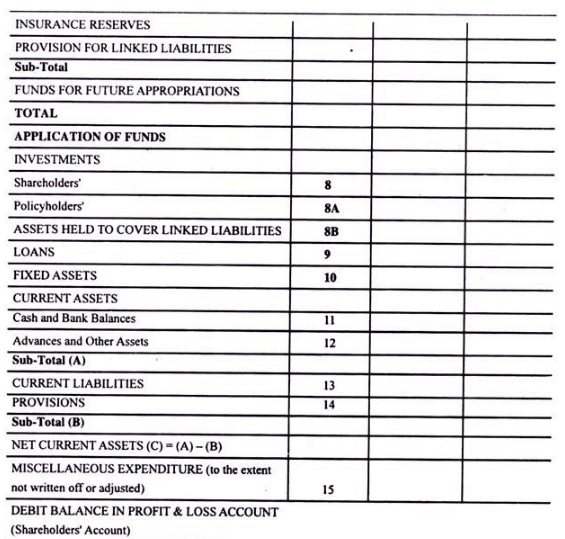

Balance Sheet – Form A-BS

Insurers doing General Insurance Business should comply with requirements of Schedule B of the Regulations which among other things, gives the following Forms:

Revenue Account – Form B – RA

Profit and Loss Account – From B – PL

Balance Sheet – From B – BS

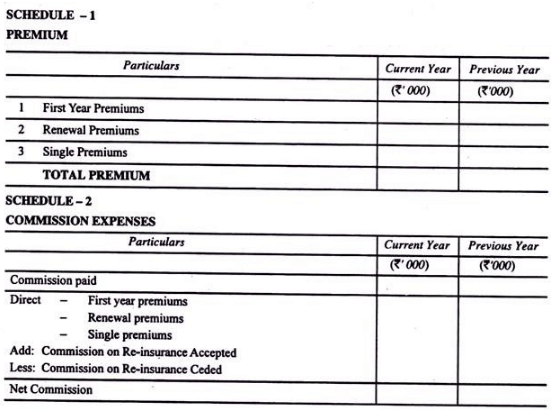

In both cases, Revenue Account and Balance Sheet are given in summary form. There are 15 Schedules in each case, the first four schedules relate to Revenue Account and the remaining eleven schedules relate to Balance Sheet which give details of the summary heads. In both Schedules A and B, Profit and Loss Appropriation Account is dispensed with and appropriations are accommodated in the Profit and Loss Account.

Life Insurance Business:

The chief peculiarity of the life insurance business is that the life insurance contracts are for a long term and that, on a particular date, the future implications of a contract must be considered before profit can be ascertained. Under an annuity contract, the life insurance office does not receive any amount after the initial payment but has to go on paying till the annuitant dies.

On a particular date, therefore, there is a liability in respect of future payments to be made.

Under a life insurance policy, also, there is liability because against a policy, the premiums expected to be received in future will generally be much less than the amount payable by way of the claim. Suppose, A took out a policy for Rs 10,000 on 5th July, 1987 for twenty years, the premium being Rs 500 per annum.

On 31st March, 2003, the life insurance company is faced with the position that only four premiums (in 2003-04, 2004-05, 2005-06, 2006-07) can be expected, amounting in all to Rs 2,000. The company will have to pay Rs 10,000 latest, on 5th July, 2008.

There is a gap of Rs 8,000 In terms of 31st March, 2003 the gap is slightly less because of interest. The possibility of A’s death must be kept in mind because death means stoppage of payment of premium and hastening the payment of the claim leading to loss of interest.

The chief point to remember is that in respect of policies already issued and still in force, there is a deficiency of claims that are expected to arise over premiums that are expected to be received. This deficiency is known as “net liability”. A company cannot be said to have made profits unless it has reserves equal to the net liability.

The calculation is made only by actuaries, mathematicians well versed in the intricacies of life insurance. The valuation has to be got done by the insurance company every year.

In case of life insurance, Revenue Account (Policyholders’ Account), Profit and Loss Account (Shareholders’ Account) and Balance Sheet are prepared as per Form A-RA, Form A-PL and Form A-BS respectively.

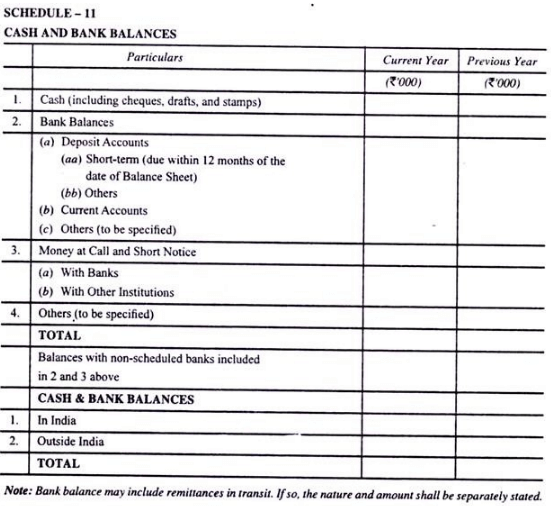

Notes: (applicable to Schedules 8 and 8A & 8B):

(a) Investments in subsidiary/holding companies, joint ventures and associates shall be separately disclosed, at cost.

(i) Holding company and subsidiary shall be construed as defined in the Companies Act, 1956:

(ii) Joint Venture is a contractual arrangement whereby two or more parties undertake an economic activity, which is subject to joint control.

(iii) Joint control is the contractually agreed sharing of power to govern the financial and operating policies of an economic activity to obtain benefits from it.

(iv) Associate is an enterprise in which the company has significant influence and which is neither a subsidiary nor a joint venture of the company.

(v) Significant influence (for the purpose of this schedule) – means participation in the financial and operating policy decisions of a company, but not control of those policies. Significant influence may be exercised in several ways, for example, by representation on the board of directors, participation in the policy making process, material intercompany transactions, interchange of managerial personnel or dependence on technical information.

Significant influence may be gained by share ownership statute or agreement. As regards share ownership, if an investor holds, directly or indirectly through subsidiaries, 20 percent or more of the voting power of the investee, it is presumed that the investor does have significant influence, unless it can be clearly demonstrated that this is not the case.

Conversely, if the investor holds, directly or indirectly through subsidiaries, less than 20 percent of the voting power of the investee, it is presumed that the investor does not have significant influence, unless such influence is clearly demonstrated. A substantial or majority ownership by another investor does not necessarily preclude an investor from having significant influence.

(b) Aggregate amount of company’s investments other than listed equity securities and derivative instruments and also the market value thereof shall be disclosed.

(c) Investment made out of Catastrophe Reserve should be shown separately.

(d) Debt securities will be considered as “held to maturity” securities and will be measured at historical costs subject to amortisation,

(e) Investment Property means a property [land or building or part of a building or both] held to earn rental income or for capital appreciation or for both, rather than for use in services or for administrative purposes.

(f) Investments maturing within twelve months from balance sheet date and investments made with the specific intention to dispose them of within twelve months from balance sheet date shall be classified as short-term investments.

Notes:

(a) No item shall be included under the head “Miscellaneous Expenditure” and carried forward unless:

1. some benefit from the expenditure can reasonably be expected to be received in future, and

2. the amount of such benefit is reasonably determinable.

(b) The amount to be carried forward in respect of any item included under the head “Miscellaneous Expenditure” shall not exceed the expected future revenue/other benefits related to the expenditure.

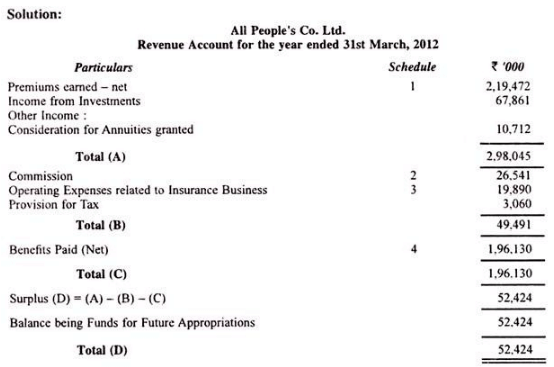

Illustration 1:

The under-mentioned balances form part of the Trial Balance of the All People’s Assurance Co. Ltd., as on 31st March, 2012:—

Amount of Life Assurance Fund at the beginning of the year, Rs 14,70,562 thousand; claims by death Rs 76,980 thousand; claims by maturity, Rs 56,420 thousand; premiums, Rs 2,10,572 thousand; expenses of management, Rs 19,890 thousand; commission, Rs 26,541 thousand; consideration for annuities granted Rs 10,712 thousand; interests, dividends and rents, Rs 52,461 thousand; income tax paid on profits Rs 13,060 thousand; surrenders, Rs 21,860 thousand; annuities, Rs 29,420 thousand; bonus paid in cash, Rs 9,450 thousand; bonus paid in reduction of premiums, Rs 2,500 thousand; preliminary expenses balance, 1600 thousand; claims admitted but not paid at the end of year, Rs 10,034 thousand; annuities due but not paid, Rs 2,380 thousand; capital paid up, Rs 14,00,000 thousand; Government securities, 124,90,890 thousand; Sundry Fixed Assets, Rs 4,19,110 thousand.

Prepare Revenue Account and the Balance Sheet after taking into account the following:—

Illustration 2:

The following balances appeared in the books of the Happy Life-Assurance Co. Ltd, as on 31st March, 2012:

|

89 videos|52 docs|22 tests

|

FAQs on Final accounts of life Insurance Companies - Advanced Corporate Accounting - Advanced Corporate Accounting - B Com

| 1. What are final accounts of Life Insurance Companies? |  |

| 2. What is the purpose of preparing final accounts of Life Insurance Companies? | |

| 3. What are the components of the final accounts of Life Insurance Companies? | |

| 4. How are final accounts of Life Insurance Companies different from final accounts of other companies? | |

| 5. What is the importance of disclosing the final accounts of Life Insurance Companies? | |

|

14.8K Views |

|

4.69/5 Rating |

|

Nov 15, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Final accounts of life Insurance Companies - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,ppt

,Sample Paper

,mock tests for examination

,Previous Year Questions with Solutions

,Free

,video lectures

,shortcuts and tricks

,Viva Questions

,practice quizzes

,Exam

,past year papers

,Final accounts of life Insurance Companies - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,Semester Notes

,study material

,Objective type Questions

,Final accounts of life Insurance Companies - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,MCQs

,Extra Questions

,Important questions

,Summary

,

Final accounts of life Insurance Companies - Advanced Corporate Accounting Free PDF Download

Importance of Final accounts of life Insurance Companies - Advanced Corporate Accounting

Final accounts of life Insurance Companies - Advanced Corporate Accounting Notes

Final accounts of life Insurance Companies - Advanced Corporate Accounting B Com Questions

Study Final accounts of life Insurance Companies - Advanced Corporate Accounting on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|