Forfeiture and Reissue of Shares - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com PDF Download

Reissue - Meaning and Issue Price of Shares

Shares are forfeited because only a part of the due amount of such shares is received and the balance remains unpaid. On forfeiture the membership of the original allottee is cancelled. He/she cannot be asked to make payment of the remaining amount. Such shares become the property of the company. Therefore company may sell these shares. Such sale of shares is called ‘reissue of shares’. Thus reissue of shares means issue of forfeited shares.

Once the Board of directors has forfeited the shares, the defaulting share holder is asked to return the share certificate which is cancelled thereafter. The board of directors passes a resolution allotting the forfeited shares to the new purchaser/purchasers of such shares.

In case of reissue of shares neither a prospectus is issued nor any offer is otherwise made to the general public. Though the amount of such shares may be called in more than one instalment but usually the entire amount is called in one instalment i.e. lumpsum.

The board of directors of the company while reissuing the shares decide the price of reissue. These shares can be reissued at par, at premium or at discount. Generally, these shares are reissued at a discount i.e. at a price which is less than its nominal value. The amount of discount allowed at the time of reissue in no case should be more than the amount forfeited on such shares.

Question arises at what price the forfeited shares can be reissued? There is no limit of the price at which it can be reissued if price charged is more than the price of issue at the time of their forfeiture. But then there is a limit below which price cannot be charged or we can say that there is a minimum price below which the company cannot reissue its forfeited shares. We can look at it from another angle i.e. the company cannot give discount more than a particular amount while reissuing the forfeited shares.

The maximum permissible discount at the time of reissue of forfeited shares is ascertained in different situations in the following manner:

(i) Shares originally issued at par : When the shares are originally issued at par, the maximum permissible discount for reissue of shares is equal to the amount forfeited on such shares

(ii) Shares originally issued at premium : In case of shares originally issued at premium, there can be two situations : (a) premium has not been received on the forfeited shares, and (b) premium has been received on such shares. The amount forfeited is the amount that has been received including the amount of premium if it has been received and the maximum discount that can be allowed on reissue of such shares is the amount so forfeited.

(iii) Shares originally issued at discount : In this case the actual amount received becomes the forfeited amount. But the maximum permissible discount on reissue of shares will be equal to the amount forfeited plus the amount of discount initially allowed on these shares at the time of their original issue.

Recording of Reissue of Shares

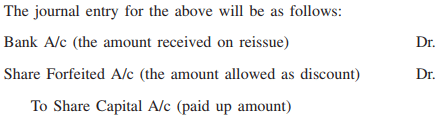

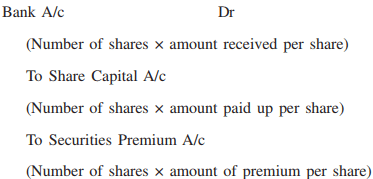

Reissue of forfeited shares at a discount : When the shares forfeited are reissued at discount, Bank account is debited by the amount received and Share capital account is credited by the paid up amount. The amount of discount allowed is debited to Share Forfeited Account. This is for adjusting the amount of discount so allowed from the amount forfeited at the time of forfeiture.

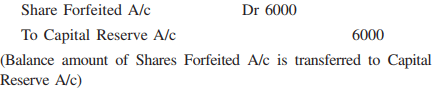

As stated earlier the amount of discount allowed on reissue of shares at the most can be equal to the forfeited amount on such shares. In that case the share forfeited account after reissue will show a zero balance. But in case, this amount of discount is less than the amount forfeited, the remaining forfeited amount will be profit for the company. This profit is a capital gain to the company and is transferred to Capital Reserve account. Journal entry of the same will be as follows :

(Transfer of surplus share forfeited amount to capital reserve A/c) If all the forfeited shares are reissued, the Share Forfeited A/c will show a zero balance because whole of the amount of this account after adjusting the amount of discount allowed on reissue will be transferred to capital reserve account. But in case, only a part of the forfeited shares are reissued and others remain cancelled, the amount forfeited on forfeited shares not reissued will remain in the Shares Forfeited Account. For adjustment of forfeited amount on share reissued will be calculated as :

Amount to be adjusted

Accounting Treatment of Reissue of forfeited shares

There can be four situations of reissue of forfeited shares. These are:

(i) Reissue of forfeited shares at discount originally issued at par

(ii) Reissue of shares at par or at premium, originally issued at par

(iii) Reissue of forfeited shares at par, at discount and at premium originally issued at premium.

(iv) Reissue of forfeited shares at par, at discount and at premium, originally issued at discount.

Accounting treatment in each of the above cases is discussed hereafter :

1. Reissue of forfeited shares issued at discount, originally issued at par

In this case the maximum discount that can be given on reissue of forfeited shares is the amount that has been received on these shares and is debited to share forfeited account.

Illustration 1

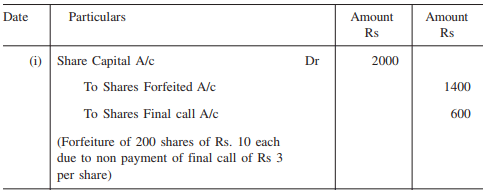

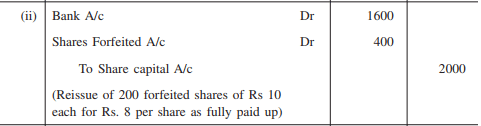

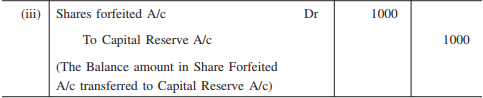

X company Ltd. forfeited 200 shares of Rs 10 each, fully called up on which Rs. 7 have been received and final call of Rs. 3 per share remains unpaid. These shares were later on reissued for Rs. 8 per share fully paid up. Make journal entry for recording the forfeiture and reissue of shares

Solution

Journal Entries.

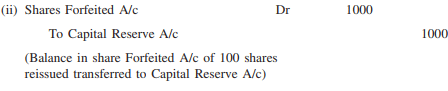

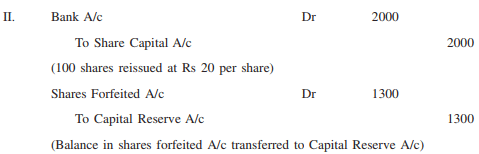

2. Reissue of forfeited shares at premium and at par, originally issued at par

In this case the whole of the amount that has been credited to Shares Forfeited A/c is transferred to Capital Reserve A/c on the reissue of such shares.

Illustration 2

Y Ltd. forfeited 400 shares of Rs. 20 each, on which Rs 15 per share have been received and balance remains due but not paid. These shares were reissued

(a) at the rate of Rs 20 per share i.e. at par

(b) at the rate of Rs. 24 per share i.e. at premium

Make necessary journal entries for reissue of the shares

Solution

Journal Entries

Case (a)

Case (b)

In the above two illustrated cases, total amount forfeited on shares reissued is transferred to capital reserve because no discount has been given on reissue of these shares. Therefore, the whole of the amount forfeited is a gain for the company.

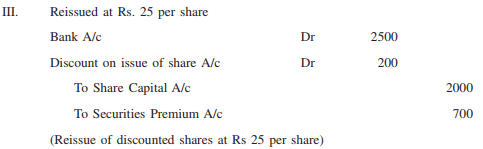

3. Reissue of forfeited shares at par, at discount and at premium, originally issued at premium :

If the shares were originally issued at premium, it is not necessary that their reissue after forfeiture is to be at premium. Such shares can be reissued at par, at discount or at premium.

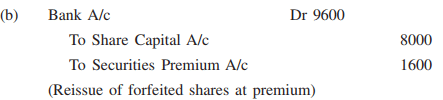

If such shares are reissued at premium the premium received should be credited to Securities Premium A/c. Journal entry will be

If such shares are reissued at par the amount that has been received and has been credited to share forfeited A/c will be credited to capital reserve A/c

If such shares are reissued at discount, the amount of discount allowed will be adjusted towards the amount credited to share forfeited A/c the balance amount of Share Forfeited A/c will be transferred to Capital Reserve A/c

Illustration 3

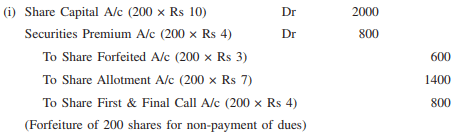

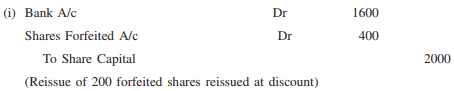

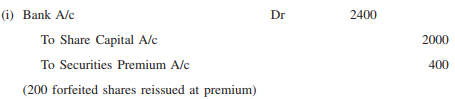

AZ Ltd. forfeited 200 shares of Rs 10 each originally issued at a premium of Rs 4 per share, the holder of which paid Rs 3 per share on application but did not pay the allotment money of Rs 7 per share (including premium) and call of Rs. 4 per share. Make necessary journal entries for the forfeiture and for reissue of these shares if :

I. Reissued at Rs 10 per share i.e. at par

II. Reissued at Rs 8 per share i.e. at discount

III. Reissued at Rs 12 per share i.e. at premium

Solution :

Journal entries

Case I.

Case II

At the time of reissue of forfeited shares a discount of Rs 2 per share is allowed so the total amount of discount of Rs 400 is adjusted from the forfeited amount of Rs 600 and the balance amount of Rs 200 is transferred to Capital Reserve A/c being a capital gain.

Case III

(Balance amout of Share Forfeited A/c transferred to Capital Reserve). As the forfeited shares have been issued at a premium so no amount of discount is there to be adjusted from the forfeited amount hence the total forfeited amount of Rs 600 is transferred to capital Reserve A/c as capital gain of the company.

4. Reissue of forfeited shares at par, premium and discount, originally issued at discount

When the forfeited shares originally issued at discount are reissued, the discount allowed at the time of original issue of such shares which was written back at the time of their forfeiture is again allowed. Thus on forfeiture shares Discount A/c is credited by the amount of discount allowed at the time of issue because its effect is to be cancelled out when shares were forfeited. When the same shares are reissued, discount on issue of shares A/c is again debited by the original amount of discount.

Illustration 4

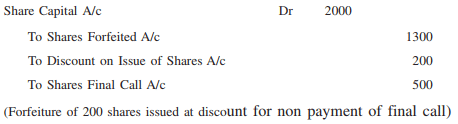

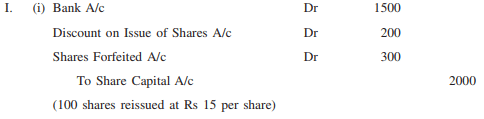

India infrastructure Ltd. has issued its shares of Rs. 20 each at a discount of Rs 2 per share. Mahima holding 100 shares did not pay final call of Rs 5 per share. Her shares were forfeited. Later on the company reissued 100 shares of these forfeited shares at (I) Rs. 15 per share (II) Rs. 20 per share, and (III) Rs. 25 per share

Make journal entries for the forfeiture and reissue of the shares in the books of company.

Solution :

Journal Entries

Reissue of shares: Reissued at Rs 15 per share

Reissue of a part of the forfeited shares

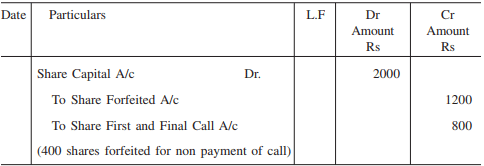

Sometimes all the forfeited shares are not reissued but a part of them are reissued. The accounting treatment is explained by the following illuatration.

Illustration 5

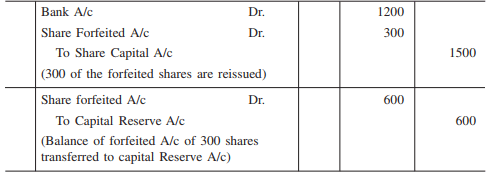

A company forfeited 400 shares of Rs 50 each on which only application money of Rs 10 per share and Rs 20 on allotment were received. Final call of the Rs 20 per share is not received. 300 of these shares are reissued at Rs 40 per share. Make journal entries for forfeiture and Reissue of shares.

Solution :

Journal entries

|

89 videos|52 docs|22 tests

|

FAQs on Forfeiture and Reissue of Shares - Advanced Corporate Accounting - Advanced Corporate Accounting - B Com

| 1. What is forfeiture and reissue of shares? |  |

| 2. What are the reasons for the forfeiture of shares? | |

| 3. How does the forfeiture of shares affect the shareholders? | |

| 4. What is the process of reissuing forfeited shares? | |

| 5. How does the reissue of shares impact the company's financial statements? | |

|

2.2K Views |

|

4.94/5 Rating |

|

Dec 23, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

ppt

,Forfeiture and Reissue of Shares - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,Forfeiture and Reissue of Shares - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,Important questions

,study material

,Summary

,Previous Year Questions with Solutions

,past year papers

,Forfeiture and Reissue of Shares - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,Objective type Questions

,practice quizzes

,MCQs

,shortcuts and tricks

,Viva Questions

,Extra Questions

,Sample Paper

,Exam

,video lectures

,mock tests for examination

,Free

,Semester Notes

;

Forfeiture and Reissue of Shares - Advanced Corporate Accounting Free PDF Download

Importance of Forfeiture and Reissue of Shares - Advanced Corporate Accounting

Forfeiture and Reissue of Shares - Advanced Corporate Accounting Notes

Forfeiture and Reissue of Shares - Advanced Corporate Accounting B Com Questions

Study Forfeiture and Reissue of Shares - Advanced Corporate Accounting on the App

|

© EduRev

|

Education Revolution

|

|