Important Questions: Non-competitive Markets | Economics for Grade 11 PDF Download

Q1: Equilibrium price of an essential medicine is too high. What can be done to bring the price down only through market forces? Explain the series of changes that will occur in the market.

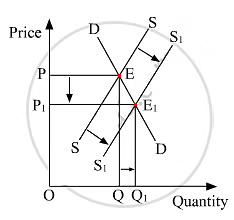

Ans: If the equilibrium price of an essential medicine is too high then the price can be reduced by increasing the supply of the commodity. This can be explained with the help of the following diagram.

In the above diagram, we can see that the demand and supply forces intersect at each other at point E. This is initial the market equilibrium with equilibrium price at P and equilibrium quantity at Q.

Now let us suppose that there is an increase in the supply of the commodity. This increase will shift the supply curve towards right from SS to S1S1 . Holding the demand constant, at the initial price OP, we can observe that there will be an excess supply. This excess supply will increase competition among the producers and consequently they would be willing to sell their output at a lower price. The price now, will continue to fall until it reaches OP1 , where the new supply curve intersects the initial demand curve. This new equilibrium will be established at E1 with the new equilibrium price at OP1. Thus, we can observe that the equilibrium price has fallen from P to OP1.

Q2: Explain the effects of a ‘price ceiling’.

Ans: Black marketing can be defined as a direct result of a price ceiling. It denotes a circumstance in which a commodity subject to the government's control policy is illegally sold at a greater price than that set by the government. It may occur primarily as a result of the presence of consumers who are willing to pay a higher price for the commodity rather than go without it.

Q3: The market for goods is in equilibrium. Demand for the good “increases”. Explain the chain effects of this change.

Ans: ‘Given equilibrium, demand rises,' the following are the chain effects of the change:

- If the price remains constant, excess demand emerges.

- As a result of the increased rivalry among purchasers, prices rise.

- A price increase produces a decrease or contraction in demand and an increase or expansion in supply.

- The price continues to rise until the market returns to equilibrium at a higher price.

Q4: Market for a necessary good is competitive in which the existing firms are earning supernormal profits. How can the policy of liberalisation by the government help in making the market more competitive in the interest of the consumers? Explain.

Ans: The liberalization strategy promotes new enterprises to enter the industry. This boosts the industry's overall output. The total market demand stays steady, and prices begin to fall. As a result, consumers receive things at significantly lower prices. Liberalization policies will remove market barriers such as licensing quotas. As a result, new firms will enter the industry. This will increase market supply and make the market more competitive. Inferring a shift to the right in the market supply curve. Other things being equal, a rightward shift in the market supply curve will result in a decrease in equilibrium price and an increase in equilibrium quantity. Extraordinary profits will eventually be wiped out, and consumers can expect to enjoy a greater quantity at a lower price.

Q5: Explain the effects of a ‘price floor’.

Ans: Buffer stock is an important instrument in the government's arsenal for ensuring a price floor or minimum support price. If the market price is less than what the government believes should be paid to farmers or producers. This will cause them to purchase the product at a higher price from the farmers or producers in order to have stock of the commodity on hand in case of future shortages.

Q6: Distinguish between collusive and non-collusive oligopoly. Explain how the oligopoly firms are interdependent in making price and output decisions.

Ans: The following points focus on the distinction between collusive and non-collusive oligopoly:

There is also a significant degree of interconnectedness between enterprises in an oligopoly. The price and production policy of one firm has a significant impact on the price and output policy of the market's rival enterprises. The reason for this is that there are only a few large corporations. When one company cuts its pricing, competitors may follow suit in order to compete. On the other hand, if one company raises the price of a specific commodity, rival enterprises may make a decision in response. Enterprises always consider the likely reaction of the market's dominant rival companies when making price and output decisions.

There is also a significant degree of interconnectedness between enterprises in an oligopoly. The price and production policy of one firm has a significant impact on the price and output policy of the market's rival enterprises. The reason for this is that there are only a few large corporations. When one company cuts its pricing, competitors may follow suit in order to compete. On the other hand, if one company raises the price of a specific commodity, rival enterprises may make a decision in response. Enterprises always consider the likely reaction of the market's dominant rival companies when making price and output decisions.

Q7: Explain the implications of the following:

(i) Products under monopolistic competition

(ii) Large number of sellers under perfect competition

Ans: (i) When a product is subject to monopolistic competition, this has ramifications. It is a distinguishing trait. A product is frequently differentiated by trade marks or brand name, size, number, and so on. The differentiated products are typically close alternatives for each other. Bagh bakri tea and Tajmahal tea are two examples. Because of product differentiation, each firm can choose its own price policy. As a result, each firm has a limited amount of control on the pricing of its product. This is done to entice buyers from competing companies. Also, because these companies produce in large quantities and their products are unique, they always have some devoted customers who buy these things and just these products.

(ii) When there are a lot of sellers on the market. In an economy, there are always more consumers and sellers. As a result, the size of each economic agent in comparison to the market is so small that they cannot influence the price through their individual actions.

Q8: Explain the implications of the following features of perfect competition.

(i) Homogenous products

(ii) Freedom of entry and exit to firms.

Ans: (i) The ramifications of homogeneous products are significant. This essentially means that the products are the same in terms of nature, quality, size, shape, and color. As a result, no producer is able to demand a different price for the product. The market has consistent pricing. Commodity must always be identical in a totally competitive market. As a result, it gives consumers or buyers no incentive to prefer one seller's product over another.

(ii) Enterprises have the freedom to enter and quit the market. When a company decides to depart or enter a market, it is entirely up to them. In this case, enterprises can only generate regular profits in the long run, with TC=TR, AR=MR, and P=MC. In exceptional circumstances, if typical profits are achieved, new firms will enter the industry, resulting in an increase in market supply. Marek's price will fall, and any extra earnings will be lost. In the event of unusually large losses, some of the existing enterprises will abandon the industry. Marek's supply will be reduced, and the commodity's market price will rise. Extraordinary losses will be erased.

Q9: Explain the implications of the following features of the oligopoly market.

(i) Few firms

(ii) Barriers to the entry of firms

Ans: The implications of the given features of oligopoly market are as follows:

(i) Oligopoly occurs when there are just a few firms in a market. However, each company is so large that it has a monopoly on a specific customer section of the market. It is so significant that the price or production policy of one firm has a direct impact on the price and output policy of competitors. As a result, drawing a precise demand curve for an oligopoly firm is likewise impossible. We have shown that oligopolistic enterprises seek to form trusts and cartels in order to avoid market pricing competition. They benefit from monopoly earnings in this manner. However, this is a very small proportion of the whole market.

(ii) It is usually more when there are barriers to firm admission. These restrictions are nearly identical to those seen in monopolistic circumstances. It is highly difficult, but not impossible, for a new firm to enter the market. These barriers might be natural, such as the need for large amounts of cash or the need to operate at the lowest possible cost, or artificial, such as patent rights. They mostly keep new entrants out of the market.

Q10: Distinguish between perfect competition and monopolistic competition.

Ans: The following are the distinctions between perfect and monopolistic contest:

|

83 videos|288 docs|49 tests

|

|

Dec 25, 2024 Last updated |

|

Explore Courses for Grade 11 exam

|

|

Summary

,MCQs

,Sample Paper

,practice quizzes

,Free

,Extra Questions

,Viva Questions

,shortcuts and tricks

,Important questions

,Important Questions: Non-competitive Markets | Economics for Grade 11

,Important Questions: Non-competitive Markets | Economics for Grade 11

,Previous Year Questions with Solutions

,Important Questions: Non-competitive Markets | Economics for Grade 11

,ppt

,study material

,video lectures

,Semester Notes

,Objective type Questions

,Exam

,past year papers

,mock tests for examination

,

Important Questions: Non-competitive Markets Free PDF Download

Importance of Important Questions: Non-competitive Markets

Important Questions: Non-competitive Markets Notes

Important Questions: Non-competitive Markets Grade 11

Study Important Questions: Non-competitive Markets on the App

|

© EduRev

|

Education Revolution

|

|