Introduction - Double Entry System

Double entry System

Meaning of double entry system:

As per this system every business transactions affects two accounts in opposite directions i.e. if one account will debited, the other will be credited.

Principles of double entry system:

1. Every business transaction affects two accounts.

2. Records both the personal and impersonal aspect.

3. Recording is made as per specified rules.

4. Preparation of Trial balance.

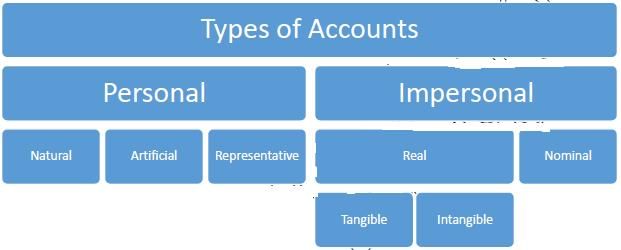

1. Personal accounts:

- The accounts which relates to the individual, firm, Company or an institution is called as personal

- Ex: mohan a/c, dps a/c, capital a/c or drawings a/c

- Rule: Debit the receiver, credit the giver.

Types of personal accounts

a. Natural personal account:

Accounts of natural persons, means accounts of

b. Artificial personal account:

These are the accounts on the name of the firms or institutions, they do not have any physical existence but they act like the human beings. Ex: dps a/c, reliance a/c, icici bank a/c.

c. Representative personal account:

When an account represents a particular person or a group of persons it is called as representative personal account. Ex: outstanding salaries (represents those group of persons to whom salary is due and not paid).

2. Real account:

- The accounts of all the assets or those things which are valuable to the business are called as real account.

- Rule: Debit what comes in, credit what goes out.

Types of Real account

a. Tangible Real account:

It includes all the tangible assets (assets which can be seen, felt, touch and seen.) Ex: land, plant.

b. In-Tangible Real account:

It includes all the intangible assets (assets which cannot be seen, felt, touch and seen.) Ex: goodwill, pate.

3. Nominal accounts:

- It includes all the expenses, losses and incomes & gains. Ex: interest, salary, commission received and bad debts.

- Rule: Debit all the expenses& losses, credit all incomes & gains

-Whenever any word(prefix or suffix) is fixed with the nominal account it becomes a personal account.

| Nominal account | Personal account |

| 1. Rent account | Outstanding rent, prepaid rent. |

| 2. Salary account | Outstanding Salary, prepaid Salary |

| 3. Commission account | Outstanding Commission, unearned commission or accrued commission |

| 4. Interest account | Interest Outstanding, Interest accrued |

Stages of double entry system:

1. Recording in the books of original entry(journal or subsidiary books)

2. Classification into ledger.

3. Summary (preparation of trial balance, financial statements{trading and profit and loss account})

Advantages of double entry system:

1. Scientific system.

2. Complete record of every business transactions

3. Preparation of trial balance.

4.Preparation of trading and profit and loss a/c.

5. Lesser possibility of fraud.

6. Legal approval.

Disadvantages of double entry system:

1. Expensive(as a number of books are maintained )

2. It is difficult to apply the rules of debit and credit.

3. Affected by errors: error of omission, commission and principles.

1. Classify the following Accounts into Personal, Real or Nominal Accounts :

1. Capital; _________________________________

2. Drawings; _________________________________

3. Cash paid; _________________________________

4. Cash received; _________________________________

5. Commission paid-. _________________________________

6. Commission received; _________________________________

7. Purchases A/c; _________________________________

8. Sales A/c; _________________________________

9. Furniture A/c; _________________________________

10. Cash A/c: _________________________________

11. Bank A/c; _________________________________

12. Bank Overdraft A/c; _________________________________

13. Debtors A./c; _________________________________

14. Creditors A/c: _________________________________

15, Travelling Expenses; _________________________________

16. Goodwill; _________________________________

17. Patents; _________________________________

18. Salary A/c; _________________________________

19. Salary, _________________________________

20. Outstanding Insurance A/c; _________________________________

21. Insurance Prepaid A/c; _________________________________

22. Bad Debts written off; _________________________________

23. Bad Debts recovered. _________________________________

Q2. Classify the following accounts into Personal, Real or Nominal accounts : -

I. Machinery VII. Drawings

II. Capital VIII. Salary

III. Stock IX. Outstanding Salary

IV. Bad Debts X. Insurance

V. Goodwill XI. Prepaid Insurance

VI. Sales XII. Interest Received

[Ans:]

Personal Accounts II, VII, IX, XI

Real Accounts I, III, V

Nominal Accounts IV, VI, VIII, X, XII. ]

Q3. State to which class of accounts does each of the following relate:-

I. Cash V. Creditors

II. Bank VI. Commission Received

III. Trade Marks VII. Accrued Commission

IV. Debtors VIII. Commission Received in Advance

[Ans:]

Personal Accounts II, IV, V, VII, VIII.

Real Accounts I,III.

Nominal Accounts VI. ]

Q4. Classify the following accounts under personal, real or nominal accounts:

(i) Commission paid

(ii) Commission received

(iii) Commission Accrued

(iv) Prepaid salaries

(v) Leasehold property A/c

(vi) Discount allowed

(vii) Carriage inwards A/c

(viii) Discount allowed

(ix) Drawings A/c

(x) Rent Received in advance

(xi) Debtors

(xii) Sales A/c

(xiii) Rent paid in advance

(xiv) Bank overdraft

[Ans:]

Personal accounts : (iii), (iv), (viii), (ix), (xi), (xiii), (xiv)

Real Accounts : (v)

Nominal Accounts : (i), (ii), (vi), (vii), (xii)]

FAQs on Introduction - Double Entry System

| 1. What is the double entry system and why do we need it in accounting? |  |

| 2. How do debits and credits work differently in the double entry bookkeeping method? | |

| 3. What's the difference between single entry and double entry accounting systems? | |

| 4. Can I understand the golden rules of accounting without knowing the double entry system first? | |

| 5. Why do trial balance and final accounts depend on the double entry system? | |