Introduction to Cash Flow Statement - Cash flow statements, Cost Accounting | Cost Accounting - B Com PDF Download

Cash Flow Statement

When it is desired to explain to management the sources of cash and its uses during a particular period of time, a statement known as cash flow statement is prepared. A statement of cash flows reports the inflows (receipts) and outflows (payments) of cash and its equivalents of an organisation during a particular period. It provides important information that compliments Statement of Profit & Loss and balance sheet. A statement of cash flow reports cash receipts and payments classified according to the entities’ major activities - operating, investing and financing during the period. This statement reports a net cash inflow or net cash outflow for each activity and for the overall business. It also reports from where cash has come and how it has been spent. It explains the causes for the changes in the cash balance. In substance, the cash flow statement summarises a myriad of specific cash transactions into a few categories for a business entity. The statement of cash flows reports the cash receipts, cash payments, and net changes in cash resulting from operating, investing and financing activities of an enterprise during a period in a format that reconciles the beginning and ending cash balances.

In view of the significant contribution of the statement of cash flows, the Institute of Chartered Accountants of India has issued in March, 1997 Accounting Standard-3 (Revised) (AS-3 Revised) ‘Cash Flow Statements’ in suppression of Accounting Standard-3 “Changes in Financial Position” issued in June 1981. It is in tune with the trends in other countries where cash flow statement has replaced the “Statement of Changes in Financial Position”. As such cash flow statement should be prepared in line with the stipulations given in AS-3 (Revised). According to the revised Accounting Standard-3, an organisation should prepare a cash flow statement and should present it for each period.

Meaning of certain terms used in this context:

Cash: Cash comprises cash in hand and demand deposits with banks. Demand deposits mean those deposits which are repayable by bank on demand by the depositor.

Cash equivalents: Cash equivalents are short term, highly liquid investments that are readily convertible into known amounts of cash and which are subject to an insignificant risk of changes in value. Cash equivalents are held for the purpose of meeting short term cash commitments rather than for investments or other purposes. Examples of cash equivalents are treasury bills, commercial paper etc. Investments in shares are excluded from cash equivalents unless they are in substance cash equivalents, for example preference shares of a company acquired shortly before their specified redemption date (provided there is only an insignificant risk of failure of the company to repay the amount at maturity).

Cash flows: Cash flows are inflows and outflows of cash and cash equivalents. It means the movement of cash into the organisation and movement of cash out of the organisation. The difference between the cash inflows and outflows is known as net cash flow which can be either net cash inflow or net cash outflow. Cash flows exclude movements between items that constitute cash or cash equivalents because these components are part of the cash management of an enterprise rather than part of its operating, investing and financing activities. Cash management includes the investment of excess cash in cash equivalents.

Problems on Cash Flow Statements (With Solution)

Problem 1:

The bank balance of a business firm has increased during the last financial year by Rs.1,50,000. During the same period it issued shares of Rs.2,00,000 and redeemed debentures of Rs.1,50,000. It purchased fixed assets for Rs.40,000 and charged depreciation of Rs.20,000. The working capital of the firm, other than bank balance, increased by Rs.1,15,000 during the period. Calculate the profit of the firm for the year.

Solution:

1,50,000 = Profit + 2,00,000 – 1,50,000 – 40,000 + 20,000 – 1,15,000

∴ Profit = Rs.2,35,000

Problem 2:

A chemical company has net sales of Rs.50 lakhs, cash expenses (including taxes) of Rs.35 lakhs and depreciation expenses of Rs.5 lakhs. If debtors decrease over the period by Rs.6 lakhs, what is its cash from operations?

Solution:

Cash from operations = Rs.50 lakhs – Rs.35 lakhs + Rs.6 lakhs = Rs.21 lakhs

There are two methods of converting net profit into net cash flows from operating activities:

(a) Direct method, and

(b) Indirect method.

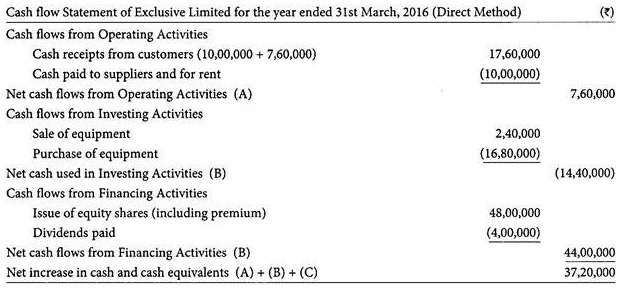

Problem 3:

The following information is available from the books of Exclusive Ltd. for the year ended 31st March, 2016:

(a) Cash sales for the year were Rs.10,00,000 and sales on account Rs.12,00,000.

(b) Payments on accounts payable for inventory totalled Rs.7,80,000.

(c) Collection against accounts receivable were Rs.7,60,000.

(d) Rent paid in cash Rs.2,20,000, outstanding rent being Rs.20,000.

(e) 4,00,000 Equity shares of Rs.10 par value were issued for Rs.48,00,000.

(f) Equipment was purchased for cash Rs.16,80,000.

(g) Dividend amounting to Rs.10,00,000 was declared, but yet to be paid.

(h) Rs.4,00,000 of dividends declared in the previous year were paid.

(i) An equipment having a book value of Rs.1,60,000 was sold for Rs.2,40,000.

(j) The cash account was increased by Rs.37,20,000.

Prepare a cash flow statement using direct method.

Solution:

Problem 4:

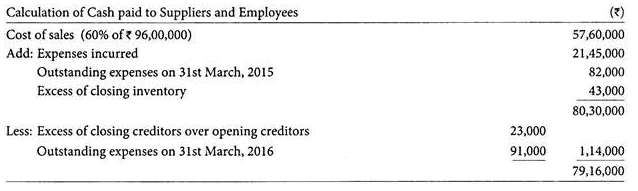

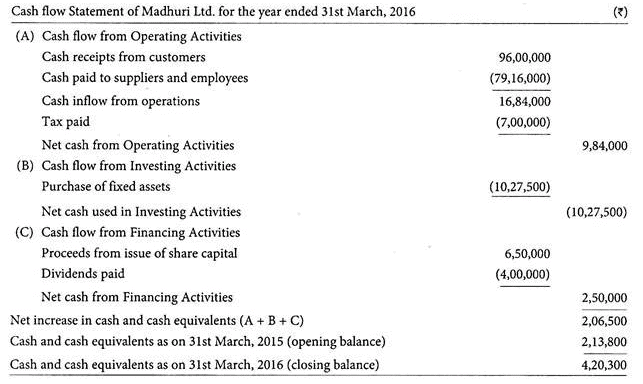

Madhuri Ltd. gives you the following information for the year ended 31st March, 2016:

(a) Sales for the year totalled Rs.96,00,000. The company sells goods for cash only.

(b) Cost of goods sold was 60% of sales.

(c) Closing inventory was higher than opening inventory by Rs.43,000.

(d) Trade creditors on 31st March, 2016 exceeded those on 31st March, 2015 by Rs.23,000

(e) Tax paid amounted to Rs.7,00,000.

(f) Depreciation on fixed assets for the year was Rs.3,15,000 whereas other expenses totalled Rs.21,45,000. Outstanding expenses on 31st March, 2015 and 31st March, 2016 totalled Rs.82,000 and Rs.91,000 respectively.

(g) New machinery and furniture costing Rs.10,27,500 in all were purchased.

(h) A rights issue was made of 50,000 equity shares of Rs.10 each at a premium of Rs.3 per share. The entire money was received with applications.

(i) Dividends totalling Rs. 4,00,000 were distributed among shareholders.

(j) Cash in hand and at bank as at 31st March, 2015 totalled Rs.2,13,800.

You are required to prepare a cash flow statement using direct method.

Solution:

Proceeds from issue of share capital:

Issue price of one share =Rs. 10 + Rs.3 = Rs.13

Proceeds from issue of 50,000 shares = Rs. 13 x 50,000 = Rs. 6,50,000

Problem 5:

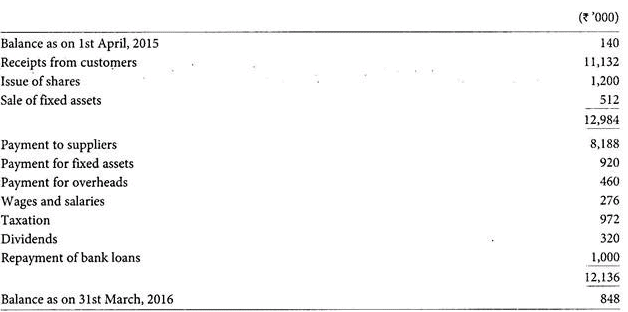

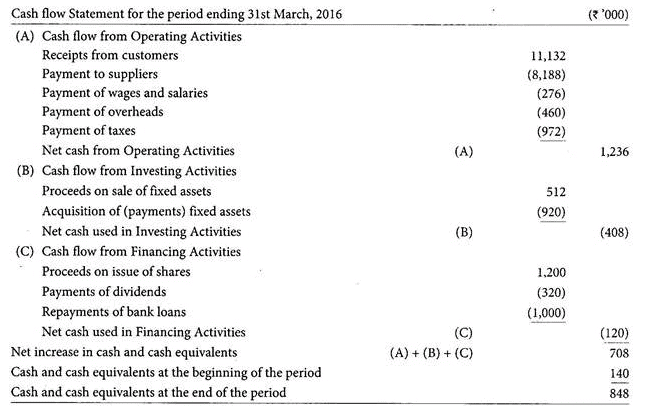

The summary of cash transactions extracted from the books of Happy Ltd. are:

You are required to prepare a cash flow statement of the company for the period ended 31st March, 2016 in accordance with the Indian Accounting Standard-3(Revised).

Solution:

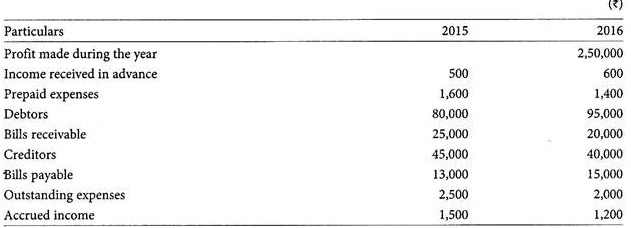

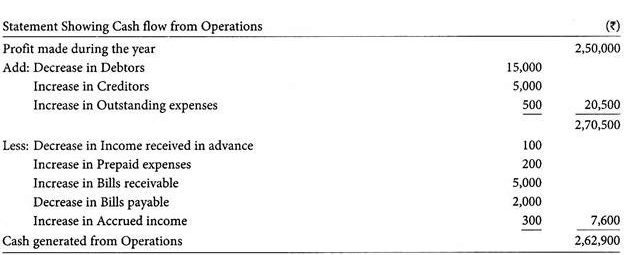

Problem 6:

Following information is available from the books of Standard Company Ltd.:

Calculate cash flow from operations.

Solution:

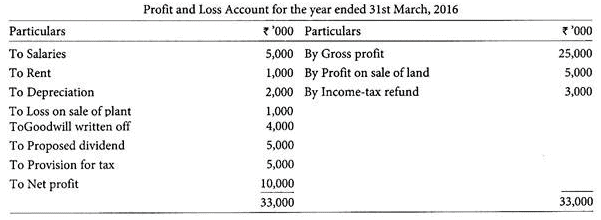

Problem 7:

From the following calculate cash from operations:

Solution:

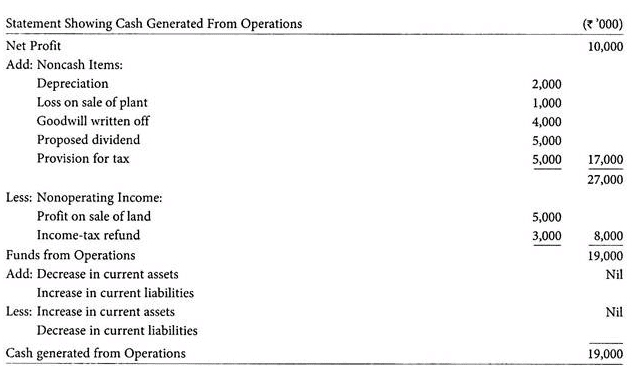

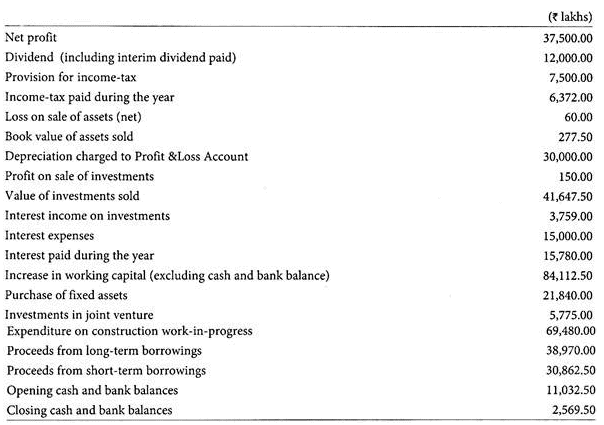

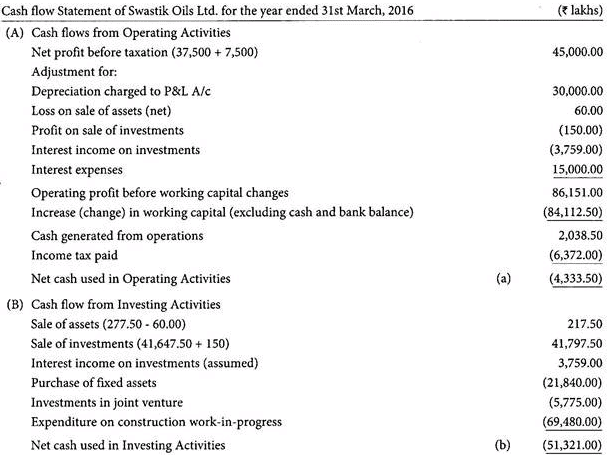

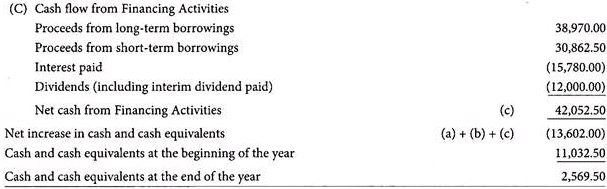

Problem 8:

Swastik Oils Ltd. has furnished the following information for the year ended 31 st March, 2016:

You are required to prepare the cash flow statement in accordance with IAS-3 for the year ended 31st March, 2016.(Make assumption wherever necessary).

Solution:

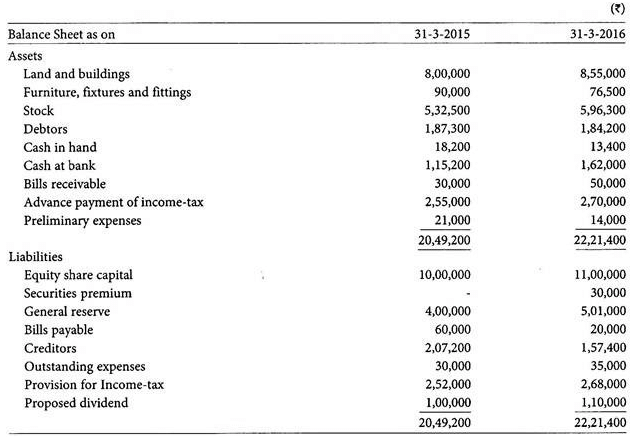

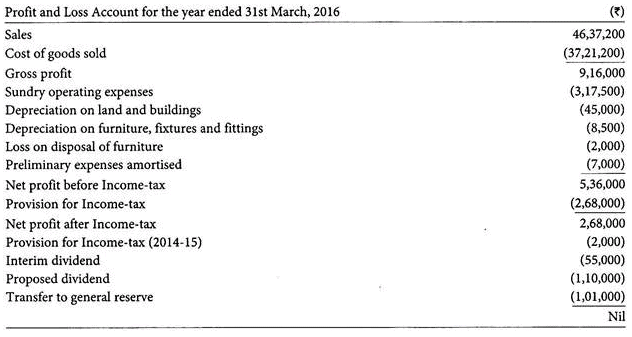

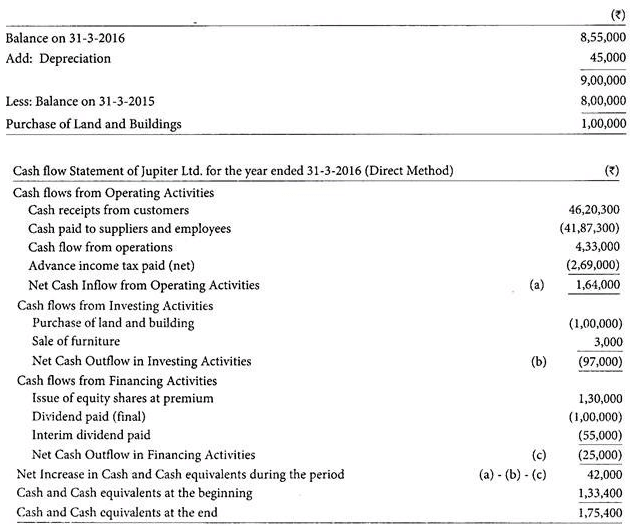

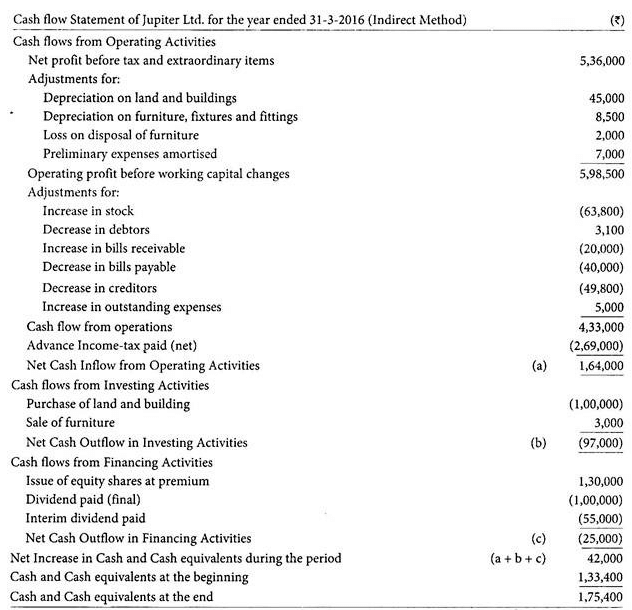

Problem 9:

The following data is available from the books of Jupiter Ltd.:

Additional Information:

(i) Liability for income-tax for the accounting year 2014-15 was fixed at Rs.2,54,000 and hence, a refund of Rs.1,000 was received out of the advance tax paid for that year.

(ii) Book value of furniture sold during the year was Rs.5,000.

You are required to prepare a Cash flow statement for the year ended 31st March, 2016.

Solution:

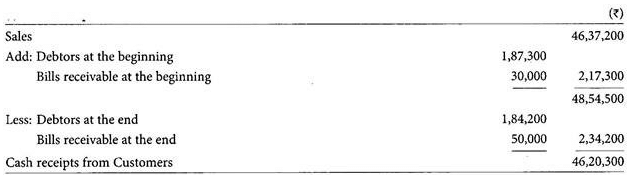

(i) Cash Receipts from Customers:

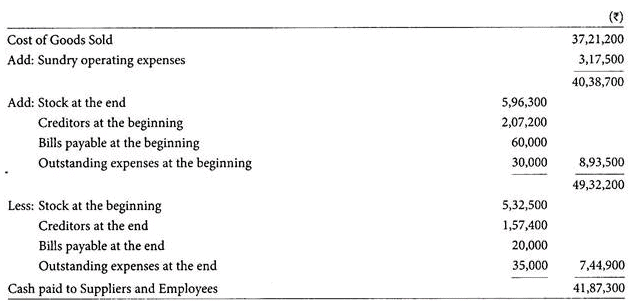

(ii) Cash Paid to Suppliers and Employees:

(iii) Tax Paid:

(iv) Purchase of Land and Building:

|

106 videos|173 docs|18 tests

|

FAQs on Introduction to Cash Flow Statement - Cash flow statements, Cost Accounting - Cost Accounting - B Com

| 1. What is a cash flow statement? |  |

| 2. Why is a cash flow statement important in cost accounting? | |

| 3. How is a cash flow statement prepared in cost accounting? | |

| 4. What is the difference between cash flow statement and income statement? | |

| 5. How can a cash flow statement help in financial decision making? | |

|

3.7K Views |

|

4.64/5 Rating |

|

Nov 15, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Objective type Questions

,Extra Questions

,Introduction to Cash Flow Statement - Cash flow statements

,MCQs

,Sample Paper

,Cost Accounting | Cost Accounting - B Com

,ppt

,Semester Notes

,mock tests for examination

,Cost Accounting | Cost Accounting - B Com

,Cost Accounting | Cost Accounting - B Com

,shortcuts and tricks

,Viva Questions

,practice quizzes

,Previous Year Questions with Solutions

,study material

,past year papers

,video lectures

,Introduction to Cash Flow Statement - Cash flow statements

,Introduction to Cash Flow Statement - Cash flow statements

,Important questions

,Summary

,Exam

,Free

;

Introduction to Cash Flow Statement - Cash flow statements, Cost Accounting Free PDF Download

Importance of Introduction to Cash Flow Statement - Cash flow statements, Cost Accounting

Introduction to Cash Flow Statement - Cash flow statements, Cost Accounting Notes

Introduction to Cash Flow Statement - Cash flow statements, Cost Accounting B Com Questions

Study Introduction to Cash Flow Statement - Cash flow statements, Cost Accounting on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|