Issue of Bonus Shares & Shares at Discount - Share Capital, Company Law | Company Law - B Com PDF Download

Bonus Shares

A company may, if its Articles provide, capitalize its profits by issuing fully-paid bonus shares. The issue of bonus shares by a company is a common feature. When a company is prosperous and accumulates large distributable profits, it converts these accumulated profits into capital and divides the capital among the existing members in proportion to their entitlements. Members do not have to pay any amount for such shares. They are given free. The bonus shares allotted to the members do not represent taxable income in their hands. [Commissioner of Income Tax, Madras v. A.A.V. Ramchandra Chettiar (1964) 1 Mad CJ 281]. Issue of bonus shares is a bare machinery for capitalizing undistributed profits. The vesting of the rights in the bonus shares takes place when the shares are actually allotted and not from any earlier date.

Advantages of Issuing Bonus Shares

- Fund flow is not affected adversely.

- Market value of the Company’s shares comes down to their nominal value by issue of bonus shares.

- Market value of the members’ shareholdings increases with the increase in number of shares in the company.

- Bonus shares is not an income. Hence it is not a taxable income.

- Paid-up share capital increases with the issue of bonus shares.

Sources for issue of Bonus shares

According to section 63(1), a company may issue fully paid-up bonus shares to its members, in any manner whatsoever, out of—

- its free reserves;

- the securities premium account; or

- the capital redemption reserve account.

| No issue of bonus shares shall be made by capitalising reserves created by the revaluation of assets. |

Conditions for issue of Bonus Shares

In terms of section 63(2), no company shall capitalise its profits or reserves for the purpose of issuing fully paid-up bonus shares, unless—

(a) it is authorised by its articles;

(b) it has, on the recommendation of the Board, been authorised in the general meeting of the company;

(c) it has not defaulted in payment of interest or principal in respect of fixed deposits or debt securities issued by it;

(d) it has not defaulted in respect of the payment of statutory dues of the employees, such as, contribution to provident fund, gratuity and bonus;

(e) the partly paid-up shares, if any outstanding on the date of allotment, are made fully paid-up;

No Bonus shares in lieu of dividend

The bonus shares shall not be issued in lieu of dividend. [Section 63(3)],

SEBI has issued regulations for Bonus Issue which are contained in Chapter IX of the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009 with regard to bonus issues by listed companies. Students may refer to study material ‘Capital Markets and Securities Laws’ for details.

Prescriptions under Companies (Share Capital and Debentures) Rules, 2014 with regard to issue

Rule 14 states that the company which has once announced the decision of its Board recommending a bonus issue, shall not subsequently withdraw the same.

Issue of Shares at a Discount: Conditions and Accounting Treatment

When Shares are issued at a price lower than their face value, they are said to have been issued at a discount. For example, if a share of Rs 100 is issued at Rs 95, then Rs 5 (i.e. Rs 100—95) is the amount of discount. It is a loss to the company. It should be noted that the issue of share below the market price but above face value is not termed as ‘Issue of Share at Discount’ Issue of Share at Discount is always below the nominal value of shares. It is debited to separate account called ‘Discount on Issue of Share’ Account.

Disclosure in Balance Sheet:

It is deducted from securities premium reserve account from the liabilities side.

Conditions to Issue Share at Discount:

Shares can be issued at discount subject to the following conditions:

(a) The shares must belong to a class already issued.

(b) Discount rate should not be more than 10%.

(c) One year must have passed since the date at which the company was allowed to commence business.

(d) The issue of such shares must take place within two months after the date of court’s sanction or within such extended time as the court may allow.

(e) The issue must be authorised by a resolution passed by the company in general meeting and sanctioned by the Company Law Board.

Accounting Treatment:

i. Generally, the ‘Discount on Shares’ is recorded at the Time of Allotment:

Share Allotment A/c … Dr. (With the amt., due)

Discount on Issue of Shares A/c … Dr. (With discount)

To Share Capital A/c (Total amount)

(Being the allotment money due)

(ii) To Write off ‘Discount on Shares’

Profit & Loss A/c/Securities Premium Reserve A/c ……..Dr

To Discount on Issue of Shares A/c

Note. Discount on issue of shares is recorded at the time of allotment made due.

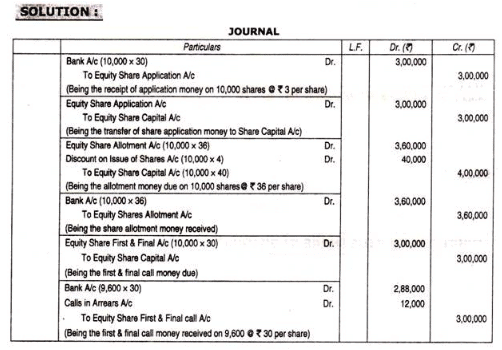

Illustration:

(Shares Issued at discount and calls in arrears. Trendy Shoe Company invited applications for 12,000 equity shares of Rs. 100 each at a discount Rs. 4 per share (allowed at the time of allotment). The amount was payable as follows: On Application Rs 30, on allotment Rs 36, on first and final call Rs. 30.

The public applied for 10,000 shares and these were allotted. All money due was with the exception the first and final call on 400 shares.

Required:

Journalise the above transactions in the books of the Company.

|

112 docs|32 tests

|

FAQs on Issue of Bonus Shares & Shares at Discount - Share Capital, Company Law - Company Law - B Com

| 1. What are bonus shares and how are they issued? |  |

| 2. Can a company issue shares at a discount? | |

| 3. What is the impact of issuing bonus shares on the share capital of a company? | |

| 4. Are bonus shares taxable for shareholders? | |

| 5. What are the advantages of issuing shares at a discount? | |

Company Law | Company Law - B Com

,practice quizzes

,Issue of Bonus Shares & Shares at Discount - Share Capital

,Issue of Bonus Shares & Shares at Discount - Share Capital

,shortcuts and tricks

,Company Law | Company Law - B Com

,Sample Paper

,Important questions

,Objective type Questions

,Free

,past year papers

,mock tests for examination

,study material

,MCQs

,Viva Questions

,Semester Notes

,Extra Questions

,video lectures

,Previous Year Questions with Solutions

,Exam

,Company Law | Company Law - B Com

,Summary

,Issue of Bonus Shares & Shares at Discount - Share Capital

,ppt

;

Issue of Bonus Shares & Shares at Discount - Share Capital, Company Law Free PDF Download

Importance of Issue of Bonus Shares & Shares at Discount - Share Capital, Company Law

Issue of Bonus Shares & Shares at Discount - Share Capital, Company Law Notes

Issue of Bonus Shares & Shares at Discount - Share Capital, Company Law B Com Questions

Study Issue of Bonus Shares & Shares at Discount - Share Capital, Company Law on the App

|

© EduRev

|

Education Revolution

|

|