Issue of Shares at Par, Premium and Discount, Advanced Corporate Accounting | Advanced Corporate Accounting - B Com PDF Download

Procedure of Issue of Shares

Face value of a share is the par value of the share. It is also known as the Nominal value or denomination of a share. To issue shares a company follows a definite procedure which is controlled and regulated by the Companies Act and Securities Exchange Board of India (SEBI). There are different ways of issue of shares which may be:

(A) For consideration other than cash

(B) For cash

(A) Issue of shares for consideration other than cash

- Sometimes shares are issued to the promotors of the company in lieu of the services provided by them during the incorporation of the compnay. The issue price of these shares is normally debited to ‘Goodwill A/c’ and journal entry is made as follows :

In case a company does not have sufficient funds for the purchase of fixed assets or for payment to creditors it may offer and allot its shares to vendors/ creditors in lieu of cash. Any allotment of shares against which cash is not to be received is called ‘issue of shares for consideration other than cash’. For example building is purchased and payment is made by issuing shares.

In case of purchase of assets like building, machinery, stock of materials, etc. the following journal entry is made :

(B) Issue of Shares for cash

In general, shares are issued for cash. The company may call the share money either in one instalment or in two or more instalments. But company always collects this money through its bankers.

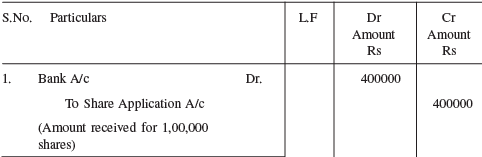

(i) Receipt of share money in one instalment

The company may receive the share money in one instalment along with application. In this case the following journal entries are made in the books of the company

(ii) Share money received in two or more instalments

Instead of receiving payment in one instalment i.e. at the time of application the company collects it in two or more instalments. The first, instalment which the appplicants have to pay along with the applications for shares is known as application money. On the allotment of shares the allottees are required to pay the second instalment which is termed as allotment money. If the company decides to call the share money in more than two instalments the other instalment is/are termed as call money (i.e. first-call, second call or final call).

In the above case the transactions are recorded in journal as given below :

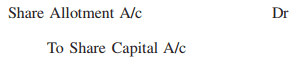

(b) On allotment of shares

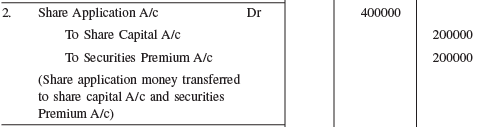

After receiving the application for shares within the prescribed time, the Board of Directors of the company proceed to allot shares. On allotment of shares the applicaion money is transferred to Share Capital A/c. For this the following journal entry is made :

(Share application for …. Shares @ Rs… per share transferred to share capital A/c)

Allotment Money becoming due and received

On the allotment of shares the amount receivable on the next instalment i.e. on allotment becomes due. The following entry is made for recording the amount due :

(i) Allotment money becoming due

(Share allotment money due on …. shares @Rs ... per share)

(ii) Receipt of allotment money

On the receipt of share allotment money the following journal entry is made:

(Receipt of the amount due on allotment of … shares)

Calls on shares

After the receipt of application and allotment money the money that remains unpaid can be called up by the company as and when required. Thus a call is a demand made by the company asking the shareholders to remit the called up amount on shares allotted to them.

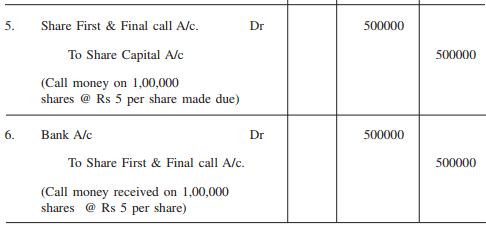

The company may demand the remaining money in more than two instalments. The amount called after the allotment is known as call money. There may be one or more calls, depending on the funds requirements of the company. When only one call is made Call Money is Due :

(Call money due on …. share @ Rs … per share)

Receipt of call money The following journal entry is made for receipt of call money:

(call money due on … shares @ Rs ... per share received)

Note : If the company makes more than one call the same accounting treatment is followed for recording the second call or third call money due and their receipt. The last call made is termed as final call.

Illustration 1

Fashion Fabrics Ltd. issued 100000 shares of Rs. 10 each on 1st April, 2006.

The amount payable on these shares was as under:

Rs 2 per share on application.

Rs 3 per share on allotment.

Rs 5 per share on call.

Make journal entries and prepare relevant accounts in the books of company.

Solutions:

Fashion Fabrics Ltd

Journal entries

Note : Although shares may be equity shares or preference shares but if the term shares is used it means equity shares)

Relevant Accounts

Bank A/c

| Dr | Cr | ||||||

Date | Particulars | JF | Amount Rs | Date | Particulars | JF | Amount Rs |

| Share Application A/c |

| 200000 |

| Balance cld |

| 1000000 |

| Share Allotment A/c |

| 300000 |

|

|

|

|

| Share First and Final call A/c |

| 500000 |

|

|

|

|

|

|

| 1000000 |

|

|

| 1000000 |

| Balance b/d |

| 1000000 |

|

|

|

|

Share Application A/c

| Dr | Cr | ||||||

Date | Particulars | JF | Amount Rs | Date | Particulars | JF | Amount Rs |

| Share Capital A/c |

| 200000 |

| Bank A/c |

| 200000 |

|

|

| 200000 |

|

|

| 200000 |

Share Capital A/c

| Dr | Cr | ||||||

Date | Particulars | JF | Amount Rs | Date | Particulars | JF | Amount Rs |

| Balance cld |

| 1000000 |

| Share Applicaiton A/c |

| 200000 |

|

|

|

|

| Share Allotment A/c |

| 300000 |

|

|

|

|

| Share First and Final call A/c |

| 500000 |

|

|

| 1000000 |

|

|

| 1000000 |

|

|

|

|

| Balance b/d |

| 1000000 |

Share Allotment A/c

| Dr | Cr | ||||||

Date | Particulars | JF | Amount Rs | Date | Particulars | JF | Amount Rs |

| Share Capital A/c |

| 300000 |

| Bank A/c |

| 300000 |

|

|

| 300000 |

|

|

| 300000 |

Share First and Final Call A/c

| Dr | Cr | ||||||

Date | Particulars | JF | Amount Rs | Date | Particulars | JF | Amount Rs |

| Share Capital A/c |

| 500000 |

| Bank A/c |

| 500000 |

|

|

| 500000 |

|

|

| 500000 |

Issue of Shares at Premium

A company can issue its shares at their face value. When company issues its shares at their face value, the shares are said to have been issued at par. Company can also issue its shares at more than or less than its face value i.e, at ‘Premium’ or at ‘Discount’ respectively. When shares are issued at premium or at discount an accounting treatment different from shares issued at par is required. Let us discuss issue of shares at premium.

Issue of Shares at Premium

If a company issues its shares at a price more than its face value, the shares are said to have been issued at Premium. The difference between the issue price and face value or nominal value is called ‘Premium’. If a share of Rs 10 is issued at Rs 12, it is said to have been issued at a premium of Rs 2 per share. The money received as premium is transferred to Securities Premium A/c. A company issues its shares at premium only when its financial position is very sound. It is a capital gain to the company. The Premium money may be demanded by the company with application, allotment or with calls.

The Companies Act has laid down certain restrictions on the utilisation of the amount of premium.

According to Section 78 of this Act, the amount of premium can be utilised for : (i) Issuing fully-paid bonus shares; |

Further, the company may demand the total amount of premium in more than one instalment. In case the company doesn’t specify the particular call with which Securities Premium is to be paid it is supposed to be called at the time of Allotment.

Accounting Treatment of premium on Issue of Shares

Following is the accounting treatment of Premium on issue of shares :

(a) Securities premium collected with share Application money :

If the Securities premium is collected on application and the company has taken decision about the allotment of shares, the following journal entry is made :

(The amount of Securities premium received on application of the alloted shares is transferred to Securities Premium A/c)

(b) Premium collected with Allotment money or Calls.

If the company decides to demand the premium with share Allotment or/and share call money, the journal entry made is:

(Adjustment of share premium due on……shares @Rs…….per share.)

Illustration :

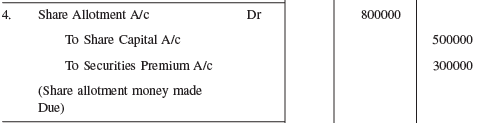

Luxuary Cars Ltd. issued 100000 shares of Rs 10 each at a premium of Rs 5 per share, payable as:

On application - Rs. 4 (including Rs 2 premium) per share

On allotment - Rs 8 (including Rs 3 premium) per share

On call - Rs. 3 per share

Applications were received for 100000 shares and allotment was made to all. Make journal entries.

Solution:

Books of Luxury Cars Ltd.

Journal entries

Issue of Shares at Discount

When the issue price of share is less than the face value, shares are said to have been issued at discount. For example if a company issues its shares of Rs 100 each at Rs. 90 each, the shares are said to be issued at discount. The amount of discount is Rs 10 per share (i.e. Rs 100 – Rs 90). Discount on shares is a loss to the company.

Section 79 of Companies Act 1956 has laid down certain conditions subject to which a company can issue its shares at a discount. These conditions are as follows :

(i) At least one year must have elapsed from the date of commencement of business; (ii) Such shares are of the same class as had already been issued; (iii) The company has sanctioned such issue by passing a resolution in its General meeting and the approval of the court is obtained. (iv) Discount should not be more than 10% of the face value of the share and if the company wants to give discount more than 10%, it will have to obtain the sanction of the Central Government. |

Accounting Treatment of Shares Issued at Discount

The amount of discount is generally adjusted towards share allotment money and the following journal entry is made:

Allotment money due on….shares @Rs ……per share after allowing discount @Rs ……….per share.

Illustraion:

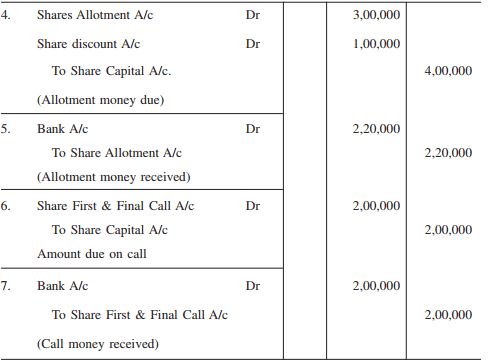

Sri Krishna Agro Chemical Ltd. was registered with a capital of Rs 5000000 divided into 50000 shares of Rs 100 each. It issued 10000 shares at discount of Rs 10 per share, payable as :

Rs 40 per share on application

Rs 30 per share on allotment

Rs 20 per share on call.

Company received applications for 15000 shares. Applicants for 12000 shares were allotted 10000 shares and applications for the remaining shares were sent letters of regret and their application money was returned. Call was made. Allotment and call money was duly received. Make journal entries in the books of the company.

Solution

Sri Krishna Agro Chemicals Ltd

Journal entries

|

89 videos|52 docs|22 tests

|

FAQs on Issue of Shares at Par, Premium and Discount, Advanced Corporate Accounting - Advanced Corporate Accounting - B Com

| 1. What is the meaning of issuing shares at par? |  |

| 2. What is the meaning of issuing shares at a premium? | |

| 3. What is the meaning of issuing shares at a discount? | |

| 4. What is the impact of issuing shares at a premium on the company's financial statements? | |

| 5. What are the legal requirements for issuing shares at a premium or discount? | |

|

15.6K Views |

|

4.62/5 Rating |

|

Dec 23, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Summary

,Sample Paper

,ppt

,Issue of Shares at Par

,Free

,Premium and Discount

,mock tests for examination

,past year papers

,Objective type Questions

,Exam

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,Semester Notes

,Extra Questions

,Issue of Shares at Par

,study material

,Premium and Discount

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,Premium and Discount

,Issue of Shares at Par

,Important questions

,video lectures

,Previous Year Questions with Solutions

,shortcuts and tricks

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,MCQs

,practice quizzes

,Viva Questions

;

Issue of Shares at Par, Premium and Discount, Advanced Corporate Accounting Free PDF Download

Importance of Issue of Shares at Par, Premium and Discount, Advanced Corporate Accounting

Issue of Shares at Par, Premium and Discount, Advanced Corporate Accounting Notes

Issue of Shares at Par, Premium and Discount, Advanced Corporate Accounting B Com Questions

Study Issue of Shares at Par, Premium and Discount, Advanced Corporate Accounting on the App

|

© EduRev

|

Education Revolution

|

|