Life Cycle Costing - Contemporary Concepts, Cost Management | Cost Management - B Com PDF Download

1. Meaning of Life Cycle Costing:

Life cycle costing is a system that tracks and accumulates the actual costs and revenues attributable to cost object from its invention to its abandonment. Life cycle costing involves tracing cost and revenues on a product by product base over several calendar periods.

The Life Cycle Cost (LCC) of an asset is defined as:

“The total cost throughout its life including planning, design, acquisition and support costs and any other costs directly attributable to owning or using the asset”.

Life Cycle Cost (LCC) of an item represents the total cost of its ownership, and includes all the cots that will be incurred during the life of the item to acquire it, operate it, support it and finally dispose it. Life Cycle Costing adds all the costs over their life period and enables an evaluation on a common basis for the specified period (usually discounted costs are used).

This enables decisions on acquisition, maintenance, refurbishment or disposal to be made in the light of full cost implications. In essence, Life Cycle Costing is a means of estimating all the costs involved in procuring, operating, maintaining and ultimately disposing a product throughout its life.

Life cycle costing is different from traditional cost accounting system which reports cost object profitability on a calendar basis (i.e. monthly, quarterly and annually) whereas life cycle costing involves tracing costs and revenues of a cost object (i.e. product, project etc.) over several calendar periods (i.e. projected life of the cost object).

Thus, product life cycle costing is an approach used to provide a long-term picture of product line profitability, feedback on the effectiveness of the life cycle planning and cost data to clarify the economic impact on alternative chosen in the design, engineering phase etc.

It is also considered as a way to enhance the control of manufacturing costs. It is important to track and measure costs during each stage of a product’s life cycle.

2. Characteristics of Life Cycle Costing:

a. Product life cycle costing involves tracing of costs and revenues of a product over several calendar periods throughout its life cycle.

b. Product life cycle costing traces research and design and development costs and total magnitude of these costs for each individual product and compared with product revenue.

c. Each phase of the product life-cycle poses different threats and opportunities that may require different strategic actions.

d. Product life cycle may be extended by finding new uses or users or by increasing the consumption of the present users.

3. Stages of Product Life Cycle Costing:

Following are the main stages of Product Life Cycle:

(i) Market Research: It will establish what product the customer wants, how much he is prepared to pay for it and how much he will buy.

(ii) Specification: It will give details such as required life, maximum permissible maintenance costs, manufacturing costs, required delivery date, expected performance of the product.

(iii) Design: Proper drawings and process schedules are to be defined.

(iv) Prototype Manufacture: From the drawings a small quantity of the product will be manufactured. These prototypes will be used to develop the product.

(v) Development: Testing and changing to meet requirements after the initial run. This period of testing and changing is development. When a product is made for the first time, it rarely meets the requirements of the specification and changes have to be made until it meets the requirements.

(vi) Tooling: Tooling up for production can mean building a production line; building jigs, buying the necessary tools and equipment’s requiring a very large initial investment.

(vii) Manufacture: The manufacture of a product involves the purchase of raw materials and components, the use of labour and manufacturing expenses to make the product.

(viii) Selling

(ix) Distribution

(x) Product support

(xi) Decommissioning: When a manufacturing product comes to an end, the plant used to build the product must be sold or scrapped.

4. Benefits of Product Life Cycle Costing:

Following are the main benefits of product life cycle costing:

(i) It results in earlier action to generate revenue or lower costs than otherwise might be considered. There are a number of factors that need to be managed in order to maximise return in a product.

(ii) Better decision should follow from a more accurate and realistic assessment of revenues and costs within a particular life cycle stage.

(iii) It can promote long term rewarding in contrast to short term rewarding.

(iv) It provides an overall framework for considering total incremental costs over the entire span of a product.

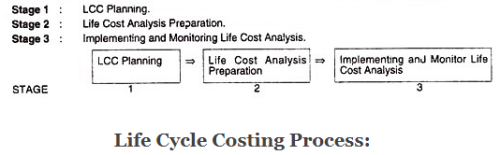

5. Life Cycle Costing Process:

Life cycle costing is a three-staged process. The first stage is life cost planning stage which includes planning LCC Analysis, Selecting and Developing LCC Model, applying LCC Model and finally recording and reviewing the LCC Results. The Second Stage is Life Cost Analysis Preparation Stage followed by third stage Implementation and Monitoring Life Cost Analysis.

The three stages are:

LCC Analysis is a multi-disciplinary activity. An analyst, involved in life cycle costing, should be fully familiar with unique cost elements involved in the life cycle of asset, sources of cost data to be collected and financial principles to be applied.

He should also have clear understanding of methods of assessing the uncertainties associated with cost estimation. Number of iteration may be required to perform to finally achieve the result. All these iterations should be documented in detail to facilitate the interpretations of final result.

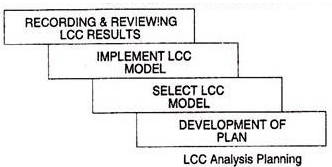

Stage 1: LCC Analysis Planning:

The Life Cycle Costing process begins with development of a plan, which addresses the purpose, and scope of the analysis.

The plan should:

i. Define the analysis objectives in terms of outputs required to assist a management decision.

Typical objectives are:

a. Determination of the LCC for an asset in order to assist planning, contracting, budgeting or similar needs.

b. Evaluation of the impact of alternative courses of action on the LCC of an asset (such as design approaches, asset acquisition, support policies or alternative technologies).

c. Identification of cost elements which act as cost drives for the LCC of an asset in order to focus design, development, acquisition or asset support efforts.

ii. Make the detailed schedule with regard to planning of time period for each phase, the operating, technical and maintenance support required for the asset.

iii. Identify any underlying conditions, assumptions, limitations and constraints (such as minimum asset performance, availability requirements or maximum capital cost limitations) that might restrict the range of acceptable options to be evaluated. Identify alternative courses of action to be evaluated.

iv. Identify alternative courses of action to be evaluated. The list of proposed alternatives may be refined as new options are identified or as existing options are found to violate the problem constraints.

v. Provide an estimate of resources required and a reporting schedule for the analysis to ensure that the LCC results will be available to support the decision-making process for which they are required.

Next step in LCC Analysis planning is the selection or development of an LCC model that will satisfy the objectives of the analysis. LCC Model is basically an accounting structure which enables the estimation of an asset components cost.

Stage 2: Life Cost Analysis Preparation:

The Life Cost Analysis is essentially a tool, which can be used to control and manage the ongoing costs of an asset or part thereof. It is based on the LCC Model developed and applied during the Life Cost Planning phase with one important difference: it uses data on real costs.

The preparation of the Life Cost Analysis involves review and development of the LCC Model as a “real-time” or actual cost control mechanism. Estimates of capital costs will be replaced by the actual prices paid. Changes may also be required to the cost breakdown structure and cost elements to reflect the asset components to be monitored and the level of detail required.

Targets are set for the operating costs and their frequency of occurrence based initially on the estimates used in the Life Cost Planning phase. However, these targets may change with time as more accurate data is obtained, from the actual asset operating costs or from the operating cost of similar other asset.

Stage 3: Implementing and Monitoring:

Implementation of the Life Cost Analysis involves the continuous monitoring of the actual performance of an asset during its operation and maintenance to identify areas in which cost savings may be made and to provide feedback for future life cost planning activities.

For example, it may be better to replace an expensive building component with a more efficient solution prior to the end of its useful life than to continue with a poor initial decision.

|

48 videos|51 docs|17 tests

|

FAQs on Life Cycle Costing - Contemporary Concepts, Cost Management - Cost Management - B Com

| 1. What is life cycle costing? |  |

| 2. How is life cycle costing different from traditional costing methods? | |

| 3. What are the benefits of using life cycle costing? | |

| 4. How is life cycle costing applied in practice? | |

| 5. What are the challenges of implementing life cycle costing? | |

|

4.75/5 Rating |

|

Dec 22, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Important questions

,Previous Year Questions with Solutions

,Life Cycle Costing - Contemporary Concepts

,practice quizzes

,Objective type Questions

,Cost Management | Cost Management - B Com

,ppt

,Semester Notes

,Sample Paper

,Summary

,Exam

,Cost Management | Cost Management - B Com

,MCQs

,mock tests for examination

,Life Cycle Costing - Contemporary Concepts

,Viva Questions

,past year papers

,Free

,study material

,Extra Questions

,Life Cycle Costing - Contemporary Concepts

,video lectures

,Cost Management | Cost Management - B Com

,shortcuts and tricks

;

Life Cycle Costing - Contemporary Concepts, Cost Management Free PDF Download

Importance of Life Cycle Costing - Contemporary Concepts, Cost Management

Life Cycle Costing - Contemporary Concepts, Cost Management Notes

Life Cycle Costing - Contemporary Concepts, Cost Management B Com Questions

Study Life Cycle Costing - Contemporary Concepts, Cost Management on the App

|

© EduRev

|

Education Revolution

|

|