Material Issue Procedure | Cost Accounting - B Com PDF Download

Introduction

Material issuance should only occur upon the presentation of an appropriately authorized requisition slip, typically sanctioned by the department's foreman. The practice of issuing materials should adhere to the "first in, first out" principle, ensuring that the earliest available lot is utilized first. Failing to exercise caution in this process may result in the deterioration of the quality of the initial material lot, which could be attributed to prolonged storage.

(i) Issue against Material Requisition Note: This serves as the official document authorizing the release of materials for usage within the factory or any of its departments. Upon receiving a material requisition slip, the storekeeper verifies the proper authorization and confirms that the requested quantity aligns with the specifications in the bill of materials. Once satisfied with the documentation, the storekeeper issues the materials, retains one copy of the based materials, and records the transaction in the records maintained by the stores department.

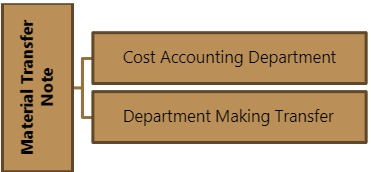

(ii) Transfer of Material: Surplus material generated from a job or other production units may sometimes be unsuitable for store transfer due to factors like bulkiness, excessive weight, brittleness, or similar reasons. In such cases, it may be viable to repurpose such materials by transferring them to another job instead of returning them to the store. It's important to emphasize that the transfer of materials from one job to another is generally irregular, if not improper, as it may hinder the accurate allocation and control of material costs for jobs or other production units. Direct transfers should only occur in the aforementioned circumstances. During material transfer, a duplicate material transfer note should be created, with the copies distributed as follows:

No additional copy is needed for the Store since no entry in the store records is necessary. The Cost Accounting Department will utilize its duplicate for the purpose of recording the essential entries in the cost ledger accounts for the impacted jobs. The format of a material requisition note may vary depending on industrial characteristics, the management information system (MIS), and the accounting system in operation.

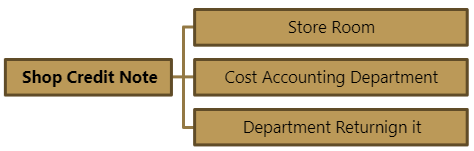

(iii) Return of Material: On occasions, it may be challenging to make precise estimates of material requirements or units of production in advance. Additionally, technical or other difficulties may sometimes hinder the exact measurement of the quantity of material needed by a department. In such cases, materials may need to be issued from stores in bulk, potentially exceeding the actual quantity required. In terms of materials control, it is crucial that any surplus material remaining upon the completion of a job is promptly handed over to the storekeeper for secure and proper custody.

Failure to do so may lead to misappropriation or misapplication of surplus material for purposes other than the originally intended one. The material cost of the job against which the excess material was initially drawn could be overstated unless the job receives credit for the surplus.

When returning surplus material to the storeroom, it should be accompanied by a document known either as a Shop Credit Note or alternatively as a Stores Debit Note. This document, prepared by the department returning the surplus material, should be in triplicate and serve the following purposes:

The structure of a shop credit note can vary depending on industrial characteristics, the management information system (MIS), and the accounting system in use.

|

106 videos|173 docs|18 tests

|

FAQs on Material Issue Procedure - Cost Accounting - B Com

| 1. What is a material issue in the context of B Com? |  |

| 2. How does a material issue affect business operations? | |

| 3. What is the procedure to address a material issue in B Com? | |

| 4. What are the common material issues faced by businesses in B Com? | |

| 5. How can businesses prevent material issues in B Com? | |

|

Dec 19, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

mock tests for examination

,Extra Questions

,MCQs

,Sample Paper

,practice quizzes

,Summary

,Previous Year Questions with Solutions

,study material

,Free

,Viva Questions

,Material Issue Procedure | Cost Accounting - B Com

,video lectures

,Material Issue Procedure | Cost Accounting - B Com

,shortcuts and tricks

,Semester Notes

,Material Issue Procedure | Cost Accounting - B Com

,Important questions

,past year papers

,Objective type Questions

,Exam

,ppt

;

Material Issue Procedure Free PDF Download

Importance of Material Issue Procedure

Material Issue Procedure Notes

Material Issue Procedure B Com Questions

Study Material Issue Procedure on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|