Methods of Capital Budgeting (Part -2), Accountancy and Financial Management | Accountancy and Financial Management - B Com PDF Download

Internal Rate of Return

Internal rate of return is time adjusted technique and covers the disadvantages of the traditional techniques. In other words it is a rate at which discount cash flows to zero. It is expected by the following ratio:

Cash inflow/Investment initial

Steps to be followed:

Step1. find out factor

Factor is calculated as follows:

F= Cash outlay (or) initial investment/Cash inflow

Step 2. Find out positive net present value

Step 3. Find out negative net present value

Step 4. Find out formula net present value

Formula

Basefactor= Positivediscount rate

DP=Difference in percentage

Merits

- It consider the time value of money.

- It takes into account the total cash inflow and outflow.

- It does not use the concept of the required rate of return.

- It gives the approximate/nearest rate of return.

Demerits

- It involves complicated computational method.

- It produces multiple rates which may be confusing for taking decisions.

- It is assume that all intermediate cash flows are reinvested at the internal rate of return.

Accept/ Reject criteria

If the present value of the sum total of the compounded reinvested cash flows is greater than the present value of the outflows, the proposed project is accepted. If not it would be rejected.

Exercise 9

A company has to select one of the following two projects:

| Project A | Project B |

Cost | Rs.22,000 | 20,000 |

Cash inflows: Year 1 | 12,000 | 2,000 |

Year 2 | 4,000 | 2,000 |

Year 3 | 2,000 | 4,000 |

Year 4 | 10,000 | 20,000 |

Using the Internal Rate of Return method suggest which is Preferable.

Solution

F = Cash outlay/Cash inflow

Project A

Cash Inflow = Total cash inflow/No. of years

= 28000/4 = 7000

= 22000/7000 = 3.14

The factor thus calculated will be located in table II below. This would give the estimated rate of return to be applied discounting the cash for the internal rate of returns. In this of project A the rate comes to 10% while in case of project B it comes to15%.

Project A

Year | Cash Inflows Rs. | Discounting Factor at 10% | Present Value Rs. |

1 | 12000 | 0.909 | 10908 |

2 | 4000 | 0.826 | 3304 |

3 | 2000 | 0.751 | 1502 |

4 | 10000 | 0.683 | 6830 |

Less: | Initial Investment. |

| 22544 |

Net Present Value |

| 22544 - 22000 = 544 | |

The present value at 10% comes to Rs. 22,544. The initial investment is Rs. 22,000. Interest rate of return may be taken approximately at 10%.

In the case more exactness is required another trial which is slightly higher than 10%(since at this rate the present value is more than initial investment) may be taken. Taking a rate of 12% the following results would emerge.

Year | Cash Inflows Rs. | Discounting Factor at 12.6% | Present Value Rs. |

1 | 12,000 | 0.893 | 10,716 |

2 | 4,000 | 0.794 | 3,188 |

3 | 2,000 | 0.712 | 1,424 |

4 | 10,000 | 0.636 | 6,380 |

Less: | Initial Investment Value |

| 21,688 |

| Net Present Value |

| 21,688 - 22,000 = (-)312 |

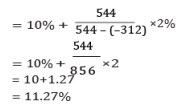

Base factor= 10%

DP =2%

Project B

Year | Cash Inflows Rs. | Discount Factor at 15% | Present value Rs. |

1 | 2,000 | 0.909# | 1,818 |

2 | 2,000 | 0.826 | 1,652 |

3 | 4,000 | 0.751 | 3,004 |

4 | 20,000 | 0.683 | 13,660 |

|

| Total present value | 20,134 |

Less: |

| Initial investment | 20,000 |

|

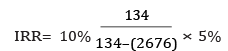

| Net present value | 134 |

= 10% + 0.24% IRR = 10.24%

Thus, internal rate of return in project ‘!’ is higher as compared to project ‘B’. Therefore project ‘!’ is preferable.

Exercise 10

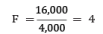

A project costs Rs. 16,000 and is expected to generate cash inflows of Rs. 4,000 each 5 years. Calculate the Interest Rate of Return.

Solution

Facts may lays between 6% to 8%

4.221 for 6%

3.993 for 8%

4000 * 4.21 = 16,840

4000 * 3.99 = 15,960

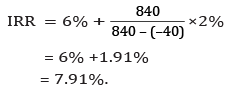

6% present value = 16,840

Less: Investment = 16,000

Net present value = 840

8% present value = 15,960

Less: Investment = 16,000

= –40

Excess Present Value Index

Excess present value is calculated on basis of net present value. It gives the results in percentage.

Exercise 11

The initial of an equipment is Rs. 10,000. Cash inflow for 5 years are estimated to be Rs. 3,500 per year. The management is desired minimum rate of excess present value index.

Solution

Present value of Rs. 1 received annually for 5 years can be had form the annuity table.

Present value of 3,500 received annually for 5 years.

Excess present value index = Total present value of cash inflows/Total present value of cash outflows

= 117,32%

Capital Rationing

In the rationing the company has only limited investment the project are selected according to the profitability. The project has selected the combination of proposal that will yield the greatest portability.

Exercise 12 Let us assume that a firm has only Rs. 20 lakhs to invest and funds cannot be provided. The various proposals along with the cost and profitability index are as follows.

Proposal | Pool of the project | Profitability Index |

1 | 6,00,000 | 1.46 |

2 | 2,00,000 | .098 |

3 | 10,00,000 | 2.31 |

4 | 4,00,000 | 1.32 |

5 | 3,00,000 | 1.25 |

Solution

In this example all proposals expect number 2 give profitability exceeding one and are profitable investments. The total outlay required to be invested in all other (profitable) project is Rs. 25,00,000(1+2+3+4+5) but total funds available with the firm are Rs. 20 lakhs and hence the firm has to do capital combination of project within a total which has the lowest profitability index along with the profitable proposals cannot be taken.

|

44 videos|75 docs|18 tests

|

|

4.81/5 Rating |

|

Dec 23, 2024 Last updated |

|

44 videos|75 docs|18 tests

|

|

Explore Courses for B Com exam

|

|

shortcuts and tricks

,study material

,Summary

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Methods of Capital Budgeting (Part -2)

,Free

,Objective type Questions

,Extra Questions

,Semester Notes

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Important questions

,MCQs

,Previous Year Questions with Solutions

,Exam

,Sample Paper

,ppt

,video lectures

,Methods of Capital Budgeting (Part -2)

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Viva Questions

,practice quizzes

,past year papers

,Methods of Capital Budgeting (Part -2)

,mock tests for examination

;

Methods of Capital Budgeting (Part -2), Accountancy and Financial Management Free PDF Download

Importance of Methods of Capital Budgeting (Part -2), Accountancy and Financial Management

Methods of Capital Budgeting (Part -2), Accountancy and Financial Management Notes

Methods of Capital Budgeting (Part -2), Accountancy and Financial Management B Com Questions

Study Methods of Capital Budgeting (Part -2), Accountancy and Financial Management on the App

|

© EduRev

|

Education Revolution

|

|