NCERT Solution (Part - 1) - Issue and Redemption of Debentures | Accountancy Class 12 - Commerce PDF Download

Page No 142

Question 1: What is meant by a Debenture?

Answer: The word Debenture is derived from a Latin word 'debere' which means to borrow. A debenture is issued in the form of a certificate under the seal of a company and containing a contract for the repayment of the principal sum after a fixed period of time and payment of interest at regular intervals, generally half yearly. Debentures are issued by a company for acquiring long-term borrowings.

Question 2: What does a Bearer Debenture mean?

Answer: When a company does not maintain any record of the debenture holders and the debenture is transferable mere by delivery, then the type of the debenture held by the holders is termed as Bearer Debenture. Interests on such debentures are paid to the persons who produce the interest coupons that are attached with these debentures in a specified bank.

Question 3: State the meaning of ‘Debentures issued as a Collateral Security’.

Answer: The term collateral security means additional or secondary security in addition to the primary security. Sometimes, when a company takes loan from a financial institution, then besides the primary security, the company may issue debenture for additional security (as collateral security). The lender who receives debenture as collateral security is not entitled for interest on these debentures. If any default is made by the company in paying back the principal amount (i.e. the loan amount) or interest on the loan, then the lender has the full right to recover his/her dues from the sale of primary security. But, if the primary security is not sufficient to recover the amount of the debt, then the debentures issued as collateral may be used for recovery of the remaining amount.

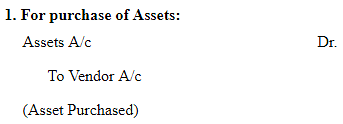

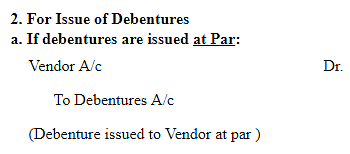

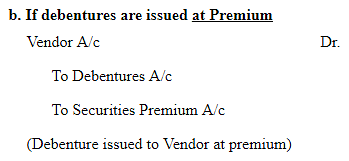

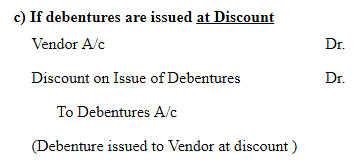

Question 4: What is meant by ‘Issue of debentures for Consideration other than Cash?

Answer: If a company purchases assets from its suppliers or vendors, then instead of paying them in cash the company issues debentures to them. This is known as issue of debenture for consideration other than cash. The issue of debenture for consideration other than cash serves the purpose of both the vendor as well as of the purchaser (company). From the purchaser’s point of view, purchasing an asset against the issue of debentures requires no additional cost for raising loans or arranging funds immediately. On the other hand, the vendor gets interest on the amount of debentures received. In this case, payment is deferred by issue of debentures and interest is paid for time lag payment. Debentures may be issued at par, premium or discount to the vendor.

Accounting treatment for Issue of Debentures for Consideration other than Cash

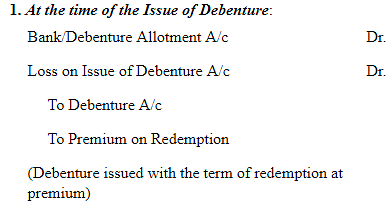

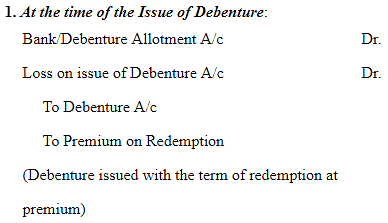

Question 5: What is meant by ‘Issue of debenture at discount and redeemable at premium?

Answer: When debentures are issued below its par value (or the face value) but are redeemed at price higher than its par value, then it is termed as issue of debenture at discount and redeemable at premium. The difference between the issue price and the redemption price is treated as loss on issue of debenture.

Example:

A 10% debenture of Rs 1,000 is issued at 5% discount and is redeemed at 10% premium.

Bank A/c | Dr. | 950 |

| |

Discount on Issue of Debenture A/c | Dr. | 50 |

| |

Loss on Issue of Debenture A/c | Dr. | 100 |

| |

| To Debenture A/c |

|

| 1,000 |

| To Debenture Redemption Premium A/c |

|

| 100 |

(Debenture issued) |

|

|

| |

Total loss = Payment made at redemption – Amount received on issue of debenture

1,100 – 950 = Rs 150

Question 6: What is ‘Capital Reserve’?

Answer: Capital Reserve is a reserve that is created out of capital profits i.e. gains or profits arising from other than the normal activities of business operations i.e. activities other than sale or purchase of goods and services. This reserve is utilised to meet future capital losses, if any, and to issue bonus shares. It cannot be distributed as dividend among the share holders. The Capital Reserve is generated out of the following activities:

i. Premium on issue of shares.

ii. Premium on issue of debentures.

iii. Profit on redemption of debentures.

iv. Profit on sale of fixed assets.

v. Profit on reissue of forfeited shares.

vi. Profit prior to incorporation, etc.

Question 7: What is meant by an ‘Irredeemable Debenture’?

Answer: Irredeemable Debentures are those debentures that are not repayable or redeemable by a company during its life time. These are repayable only at the time of winding up of the company. These are also known as Perpetual Debentures that means debentures having indefinite life. In India, now days, no company can issue irredeemable debentures.

Question 8: What is a ‘Convertible Debenture’?

Answer: Convertible Debentures are those debentures that can be converted into equity shares after a specified period of time. These are of following two types:

i. Fully Convertible Debentures: When the whole amount of a debenture is convertible into equity shares worth of equivalent amount, then these debentures are called Fully Convertible Debentures. There is no need to maintain Debenture Redemption Reserves for such debentures.

ii. Partly Convertible Debentures: When only a part of the amount of a debenture is convertible into equity share, then these debentures are called Partly Convertible Debentures. In this regards, the Debenture Redemption Reserve is maintained only for the non-convertible part of the debenture.

Question 9: What is meant by ‘Mortgaged Debentures’?

Answer: Mortgaged Debentures are those debentures that are secured against asset/s of a company. These are also known as secured debentures. If the debentures are secured against a particular asset, then it is called fixed charge whereas, if the debentures are secured against all the assets of a company, then it is called floating charge. In case the company fails to pay back the principal amount of debenture or fails to meet its interest obligations on the due date, then the debenture holders have the right to sell the mortgage asset in order to realise their amount due to the company.

Question 10: What is discount on issue of debentures?

Answer: When the debentures are issued at a price below its par value or face value, then it is said that the debentures are issued at discount. The difference between the issue price and the face value of the debenture is regarded as a capital loss.

As per the Revised Schedule VI of the Companies Act, Discount on Issue of Debentures is shown in the Notes to Accounts:

1. With the amount that is to be written off within 12 months from the date of Balance Sheet - Shown under Other Current Assets

2. With the amount that is to be written off after 12 months from the date of Balance Sheet - Shown under Other Non-Current Assets

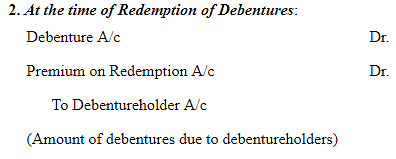

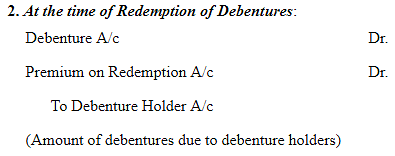

Question 11: What is meant by ‘Premium on Redemption of Debentures’?

Answer: When the debentures are redeemed at a price more than its face value or the par value, then it is said that the debentures are redeemed at premium. The difference between the redeemed price and the par value is regarded as a capital loss and this loss is written off till the redemption of the debentures. The Premium on Redemption of Debenture is shown in the Notes to Accounts under the sub-head of 'Other Long-term Liabilities'. The final balance is shown under the main head of 'Non-Current Liabilities' on the Equity and Liabilities side of the Company's Balance Sheet.

Accounting Treatment for Premium on Redemption on Debentures:

Question 12: How are debentures different from shares? Give two points.

Answer:

Basis of Comparisons | Debentures | Shares |

1. Meaning | Debentures are a part of loan, therefore, the debenture holders are the creditors of a company. | Shares form a part of capital, hence, share holders are the owner of a company. |

2. Voting Rights | These do not carry any voting rights for their holders. | These carry voting rights for their holders. |

Question 13: Name the head under which ‘discount on issue of debentures’ appears in the Balance Sheet of a company.

Answer: Discount on Issue of Debentures is regarded as a capital loss. As per the Revised Schedule VI of the Companies Act, Discount on Issue of Debentures is shown in the Notes to Accounts:

1. With the amount that is to be written off within 12 months from the date of Balance Sheet - Shown under Other Current Assets

2. With the amount that is to be written off after 12 months from the date of Balance Sheet - Shown under Other Non-Current Assets

Page No 143

Question 14: What is meant by redemption of debentures?

Answer: Redemption of debenture means repayment of debentures by the company to the debenture holders. In other words, it implies the discharge of liabilities by repaying the amount due to the debenture holders as per the terms and conditions determined at the time of issue of debentures. Debentures may be redeemable at par, premium or discount, but, nowa days, these are mostly redeemable at par or premium. The redemption can be done out of profits or from the fresh issue of debentures or shares. Redemption of debentures may be done by the following methods:

1. In lump sum at the time of maturity,

2. In instalments by draw of lots at the end of each year,

3. By purchase in open market whenever price is below its face value,

4. By converting debentures into shares or new debentures.

Question 15: Can the company purchase its own debentures?

Answer: Yes, a company can purchase its own debentures provided it is authorised by its Article of Association. As per the Company Act, if a company is authorised by its Article of Association, only then it may purchase its own debentures from the open market. The main purposes of such purchase are as follows:

1. For immediate cancellation of debenture liability, if the interest rate on its debenture is higher than the market rate of interest.

2. A company may also purchase its own debentures with the motive of investment and sell them at higher price in future and thereby earn profit.

Question 16: What is meant by redemption of debentures by conversion?

Answer: When a debenture holder can convert his/her debentures into shares or new debentures after the expiry of a specified period of time, then it is known as redemption of debentures by conversion. As the company do not need to pay any funds for the redemption, so there is no need to maintain the Debenture Redemption Reserve (DRR). The new shares or debentures may be issued at par, premium or at discount.

Question 17: How would you deal with ‘Premium on Redemption of Debentures’?

Answer: When the debentures are redeemed at a price more than its face value or the par value, then it is said that the debentures are redeemed at premium. The difference between the redeemed price and the par value is regarded as a capital loss and this loss is written off till the redemption of the debentures. The Premium on Redemption of Debenture is shown in the Notes to Accounts under the sub-head of 'Other Long-term Liabilities'. The final balance is shown under the main head of 'Non-Current Liabilities' on the Equity and Liabilities side of the Company's Balance Sheet.

Accounting Treatment for Premium on Redemption on Debentures:

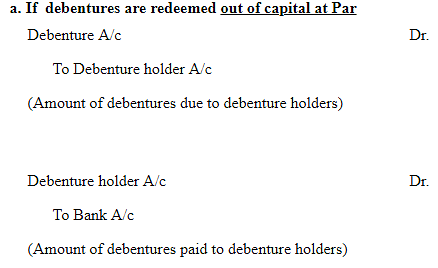

Question 18: What is meant by ‘Redemption out of Capital?

Answer: When debentures are redeemed out of capital and no profits are utilised for redemption, then such redemption is termed as redemption out of capital. In such a situation, no profits are transferred to the Debenture Redemption Reserve.

As per the guideline laid down by Securities and Exchange Board of India (SEBI) and the Section 117C of Company Act of 1956, the creation of Debenture Redemption Reserve is mandatory (DRR). Therefore, it is not possible to redeem debentures purely out of capital, as it reduces the value of assets. The following companies are exempted from the creation of DRR.

1. Infrastructure companies (i.e. those companies that are engaged in the business of developing, maintaining and operating infrastructure facilities)

2. A Company that issues debentures with a maturity up to 18 months

The following are the necessary Journal entries that need to be passed, in case the debentures are redeemed out of capital.

Question 19: What is meant by redemption of debentures by ‘Purchase in the Open Market?

Answer: According to the Company Act, if a company is authorised by its Article of Association, only then it may purchase its own debentures from the open market. The main purpose of such purchase is as follows:

1. For immediate cancellation of debenture liability, if the interest rate on its debenture is higher than the market rate of interest.

2. A company may also purchase its own debentures with the motive of investment and sell them at higher price in future and thereby earn profit.

Question 20: Under which head is the ‘Debenture Redemption Reserve’ shown in the Balance Sheet?

Answer: As per the Revised Schedule VI, Debenture Redemption Reserve (DRR) is shown in the Notes to Accounts of Reserve and Surplus. The final balance after adding DRR, is shown as the sub-head 'Reserves and Surplus' under the main head of Shareholders' Funds on the Equity and Liabilities side of the Company's Balance Sheet.

|

47 videos|180 docs|56 tests

|

FAQs on NCERT Solution (Part - 1) - Issue and Redemption of Debentures - Accountancy Class 12 - Commerce

| 1. What is the meaning of debentures? |  |

| 2. What is the difference between secured and unsecured debentures? | |

| 3. How are debentures redeemed? | |

| 4. What is the difference between redeemable and irredeemable debentures? | |

| 5. What are the methods of debenture redemption? | |

|

2.4K Views |

|

4.60/5 Rating |

|

Nov 15, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

Sample Paper

,NCERT Solution (Part - 1) - Issue and Redemption of Debentures | Accountancy Class 12 - Commerce

,Important questions

,video lectures

,NCERT Solution (Part - 1) - Issue and Redemption of Debentures | Accountancy Class 12 - Commerce

,Summary

,Previous Year Questions with Solutions

,ppt

,Free

,MCQs

,Extra Questions

,shortcuts and tricks

,Semester Notes

,study material

,mock tests for examination

,past year papers

,Viva Questions

,Exam

,practice quizzes

,Objective type Questions

,NCERT Solution (Part - 1) - Issue and Redemption of Debentures | Accountancy Class 12 - Commerce

;

NCERT Solution (Part - 1) - Issue and Redemption of Debentures Free PDF Download

Importance of NCERT Solution (Part - 1) - Issue and Redemption of Debentures

NCERT Solution (Part - 1) - Issue and Redemption of Debentures Notes

NCERT Solution (Part - 1) - Issue and Redemption of Debentures Commerce Questions

Study NCERT Solution (Part - 1) - Issue and Redemption of Debentures on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|

within 7 days!