NCERT Solution (Part - 1) - Bank Reconciliation Statement | Accountancy Class 11 - Commerce PDF Download

Short Answers

Page No. : 181

Question 1 : State the need for the preparation of bank reconciliation statement?

Answer :

The need to prepare Bank Reconciliation Statement are given below.

1. It helps in finding out the errors and omissions committed in the Cash Book and the Pass Book.

2. It shows uncleared cheques, which have already been debited in the Cash Book but have not been yet recorded in the Pass Book.

3. It helps in checking embezzlement of money from the bank account.

4. It helps in measuring the accuracy of the transactions recorded in the Cash Book.

5. It facilitates in preparing revised Cash Book that reflects true bank balance.

Question 2: What is a bank overdraft?

Answer: Bank overdraft is a liability to an account holder. When the account holder withdraws excess amount over his/her available bank balance, he/she runs a negative bank balance. The negative bank balance is an obligation to the account holder and is called bank overdraft. In other words, bank overdraft is the excess of withdrawal over deposits.

Question 3: Briefly explain the statement 'wrongly debited by the bank' with the help of an example.

Answer :Amount wrongly debited by the bank implies a situation when the bank wrongly debits a Pass Book. The following are the common mistakes that occur in the Pass Book when bank wrongly debits the Pass Book.

1. Mistake occurs when any two account holders' names are identical. For example, a cheque of Rs 2,000 issued by Mr. Prem Singh was wrongly paid through Mr. Prem Kumar's account.

2. Mistake occurs in case a person has more than one account in a bank. For example, a cheque of Rs 1,000 issued from his Current Account was wrongly paid through his Savings Account.

3. Sometimes amounts of cheques are wrongly recorded. For example, payment of Rs 2,000 through cheque was wrongly debited in the Pass Book as Rs 20,000.

Question 4 : State the causes of difference occurred due to time lag.

Answer : The causes of difference that occur due to time lag are given below.

1. When issued cheques are not presented for payment in the period for which Bank Reconciliation Statement is being prepared, i.e., date of issue and the date of presenting the cheques are not same.

Cheques are credited in the Cash Book on the date that is mentioned on it, while in the

Pass Book, cheques are debited when they are presented for the payment. Sometimes,

the holder of a cheque does not present the cheque for payment on date ehich is mentioned on Cheque. The time gap between the date of issue and the date of presenting cheque for payment in the bank may lead to difference between the Cash Book and the Pass Book balances.

2. When deposited cheques are not cleared in the period for which the Bank Reconciliation Statement is being prepared.

Usually, date of deposit of cheque and date of clearance are not same as the clearance

of cheque takes time. The difference between the Cash Book and the Pass Book balances arise when a cheque is deposited at the end of a period for which the Bank Reconciliation Statement is prepared and the cheque gets clearance in the subsequent period.

Question 5 : Briefly explain the term favourable balance as per cash book

Answer : Favourable balance (Debit Balance), as per the Cash Book, is an asset to an account holder. It is also known as debit balance as per the Cash Book. Favourable balance is the excess of total of debit side over total of credit side of a bank column of a Cash Book. In other words, favourable balance means excess of deposits over withdrawals.

Question 6 : Enumerate the steps to ascertain the correct cash book balance.

Answer : Generally, differences between the Cash Book and the Pass Book arise due to the reason that items have not been recorded in the Cash Book. In order to ascertain the correct Cash Book balance, we need to prepare Corrected (Adjusted) Cash Book. The below given steps are involved in the preparation of Corrected (Adjusted) Cash Book.

Step 1: Note down the bank balance as per the Cash Book.

Step 2: Rectify all the errors committed in the Cash Book.

Step 3: Enter those transactions in the debit of the Cash Book, which are only in the credit of the Pass Book.

Step 4: Enter those transactions in the credit of the Cash Book that are only in the debit of the Pass Book.

Step 5: The Cash Book is totalled and balancing figure is calculated. This balancing figure is use for preparing BRS.

Page No. : 181

Long answers :

Question 1 : What is a bank reconciliation statement? Why is it prepared?

Answer : Bank Reconciliation Statement is a statement prepared for determining causes of differences and reconciling bank balance (as per the Cash Book) with the balance as per the Pass Book or vice versa.

In day to day affairs, an individual or organisation makes numerous transactions through bank. Along with the copy of bank statement (i.e., the Pass Book), an individual or organisation needs to maintain a separate book (Cash Book) for recording the banking transactions. When large number of transactions is made through bank, the balance of the Cash Book may differ from the balance of the Pass Book.

There can be many reasons of differences between the Cash Book and the Pass Book, such as below given ones.

1. Deposit of cheque was recorded in the Cash Book at the time of deposit; however, was collected later or notcollected by the bank.

2. Cheque issued was recorded in the Cash Book; however, was not recorded in the Pass Book in the month of issue. It was entered in the Pass Book in the next month when it was

presented for payment in the bank.

3. Interest allowed by the bank is added in the pass book but not in the Cash Book. Bank Reconciliation Statement (BRS) is prepared when the bank balance of the Cash Book is not equal to the balance shown by the Pass Book on the same date (when BRS is being prepared). In order to match the two respective balances, errors and omissions are to be located and rectified, which is the main rationale behind preparing the Bank Reconciliation Statement.

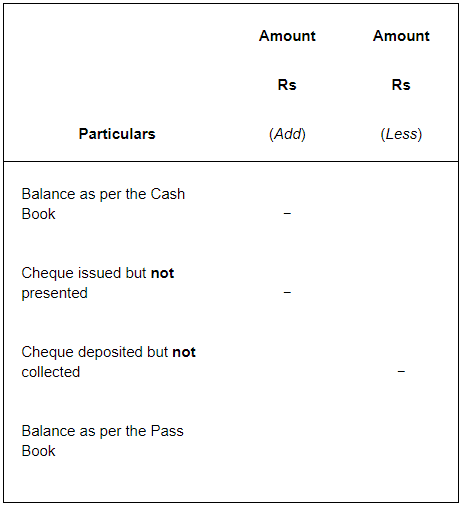

Specimen of Bank Reconciliation Statement

The need for preparation of Bank Reconciliation Statement is explained below.

1. It helps in finding out the errors and omissions committed in the Cash Book and in the Pass Book.

2. It shows uncleared cheques that have already been debited in the Cash Book but have not yet been recorded in the Pass Book.

3. It helps in checking embezzlement of money from the bank account.

4. It helps in measuring the accuracy of transactions recorded in the Cash Book.

5. It facilitates in preparing revised cash book that reflects a true bank balance.

Question 2 : Explain the reasons where the balance shown by the bank passbook does not agree with the balance as shown by the bank column of the cash book.

Answer : Below given are the reasons on account of which the balance shown by the bank Pass Book does not agree with the balance shown by the bank column of the Cash Book.

1. Differences due to time lag: In the following situations, differences may arise, if the date of recording transactions in the bank column of the Cash Book is not same to that of in the Pass Book.

2. Cheques issued by the firm but presented after the date that is mentioned on the cheque or still not presented in the bank: Usually, issue of a cheque is recorded in the bank column of the Cash Book on the date that is mentioned (mentioned date) on the cheque. Sometimes, the holder of the cheque does not present the cheque on the date which is mentioned on it. This may lead to differences in the balance between the Pass Book and the bank balance of the Cash Book.

3. Deposit of cheque recorded in the Cash Book at the time of deposit but collected later or not collected by the bank: Deposit of a cheque is recorded in the bank column of the Cash Book on the date when it is deposited in the bank for payment but bank records it in the Pass Book on the date of clearance. Usually, date of deposit and date of clearance are not the same. This difference in the two respective dates leads to a mismatch between the Pass Book and the bank balance of the Cash Book.

4. Transactions recorded only in the Pass Book: Transactions, like interest allowed by bank on the deposits, bank charges, etc., are recorded first in the Pass Book. After getting intimation from the bank, these are recorded in the bank column of the Cash Book. However, sometimes, due to delay in intimation of these transactions to the customers, the Cash Book remains notupdated, which leads to the difference between the Pass Book and the bank balance of the Cash Book.

Below given are the examples that lead to such differences.

1. The transactions that reduce balance of the Pass Book and are recorded only in the Pass Book and not in the Cash Book are given below.

- Bank charges, charged by the bank but not recorded in the Cash Book

- Dishonour of a bill discounted by the bank

- Interest charged by the bank on overdraft

- Direct payment made by the bank as per the instructions of the accountholder

2. The transactions that increase the balance of the Pass Book and are recorded only in

the Pass Book and not in the Cash Book are given below.

- When intimation regarding interests and dividend collected by the bank is not given to the account holder

- Amount deposited by any customer directly into the bank

- Interest credited (allowed) by the bank

3. Errors and omissions

Any error or omission committed in the Pass Book, such as double recording of a deposited cheque, wrong posting of amounts, current account cheque wrongly paid through saving account, etc., result in the difference of the balance between the Pass Book and the bank balance of the Cash Book.

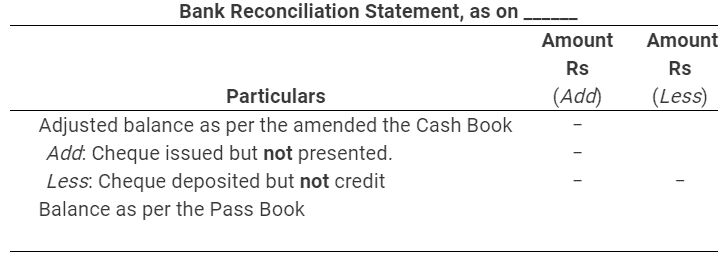

Question 3 : Explain the process of preparing bank reconciliation statement with amended cash balance.

Answer : Bank Reconciliation Statement can be prepared with the adjusted/amended bank column of the Cash Book by the below given steps.

Step 1: Note down the bank balance as per the Cash Book.

Step 2: Rectify all the errors committed in the Cash Book.

Step 3: Enter those transactions in the debit column of the Cash Book that are only in the credit column of the Pass Book.

Step 4: Enter those transactions in the credit column of the Cash Book that are only in the debit column of the Pass Book.

Step 5: After completing the above steps, the balance or the overdraft, as per amended Cash Book, arrives, with which Bank Reconciliation Statement can be prepared.The performa of Bank Reconciliation Statement through amended balance is given below.

Numerical questions :

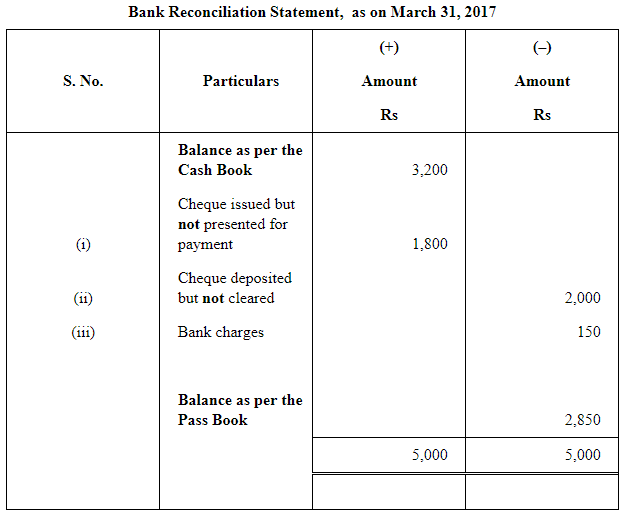

Question 1 : From the following particulars, prepare a, bank reconciliation statement as at March 31, 2017.

(i) Balance as per cash book Rs 3,200

(ii) Cheque issued but not presented for payment Rs 1,800

(iii) Cheque deposited but not collected upto March 31, 2017 Rs 2,000

(iv) Bank charges debited by bank Rs 150

Answer :

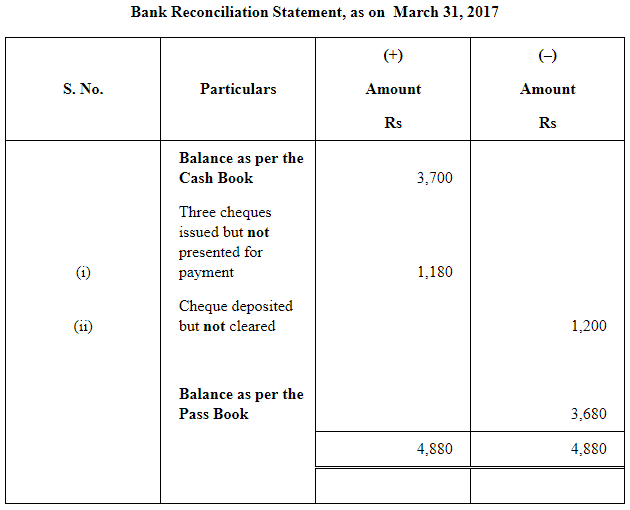

Question 2 : On March 31 2017 the cash book showed a balance of Rs 3,700 as cash at bank, but the bank passbook made up to same date showed that cheques for Rs 700, Rs 300 and Rs 180 respectively had not presented for payment, Also, cheque amounting to Rs 1,200 deposited into the account had not been credited. Prepare a bank reconciliation statement.

Answer :

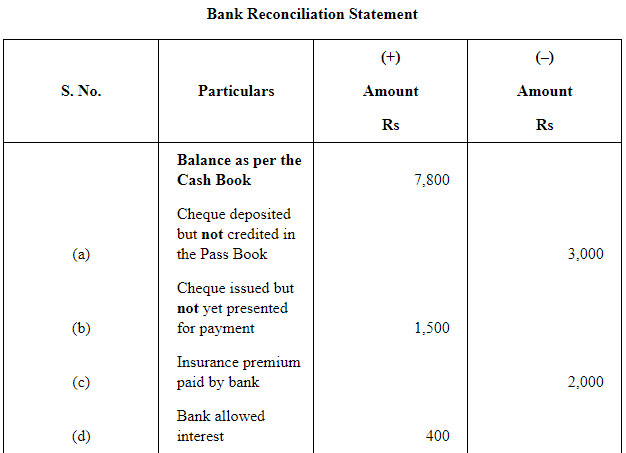

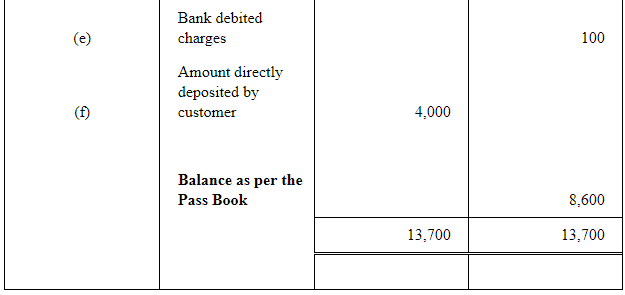

Question 3 : The cash book shows a bank balance of Rs 7,800. On comparing the cash book with passbook the following discrepancies were noted:

(a) Cheque deposited in bank but not credited Rs 3,000

(b) Cheque issued but not yet present for payment Rs 1,500

(c) Insurance premium paid by the bank Rs 2,000

(d) Bank interest credit by the bank Rs 400

(e) Bank charges Rs 100

(d) Directly deposited by a customer Rs 4,000

Answer :

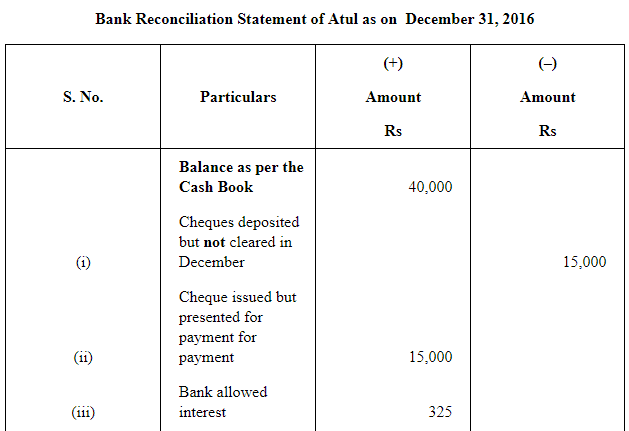

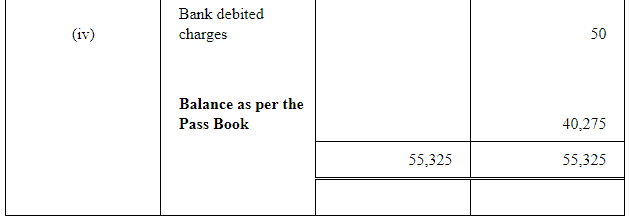

Question 4 : Bank balance of Rs 40,000 showed by the cash book of Atul on December 31, 2016. It was found that three cheques of Rs 2,000, Rs 5,000 and Rs 8,000 deposited during the month of December were not credited in the passbook till January 02, 2017. Two cheques of Rs 7,000 and Rs 8,000 issued on December 28, were not presented for payment till January 03, 2017. In addition to it bank had credited Atul for Rs 325 as interest and had debited him with Rs 50 as bank charges for which there were no corresponding entries in the cash book.

Prepare a bank reconciliation statement as on December 31, 2016.

Answer :

Page No 182:

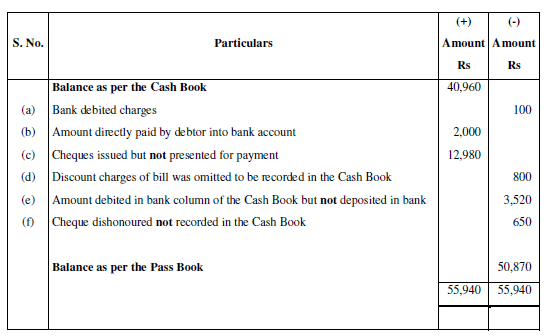

Question 5 : On comparing the cash book with passbook of Naman it is found that on March 31, 2017, bank balance of Rs 40,960 showed by the cash book differs from the bank balance with regard to the following:

(a) | Bank charges Rs 100 on March 31, 2017, are not entered in the cash book. |

(b) | On March 21, 2017, a debtor paid Rs 2,000 into the company’s bank in settlement of his account, but no entry was made in the cash book of the company in respect of this. |

(c) | Cheques totaling Rs 12,980 were issued by the company and duly recorded in the cash book before March 31, 2017, but had not been presented at the bank for payment until after that date. |

(d) | A bill for Rs 6,900 discounted with the bank is entered in the cash book with recording the discount charge of Rs 800. |

(e) | Rs 3,520 is entered in the cash book as paid into bank on March 31st, 2017, but not credited by the bank until the following day. |

(f) | No entry has been made in the cash book to record the dishonour or on March 15, 2017 of a cheque for Rs 650 received from Bhanu. |

Prepare a reconciliation statement as on March 31, 2017.

Answer :

|

64 videos|152 docs|35 tests

|

FAQs on NCERT Solution (Part - 1) - Bank Reconciliation Statement - Accountancy Class 11 - Commerce

| 1. What is a Bank Reconciliation Statement? |  |

| 2. Why is Bank Reconciliation Statement important? | |

| 3. What are the steps involved in preparing a Bank Reconciliation Statement? | |

| 4. How often should a company prepare a Bank Reconciliation Statement? | |

| 5. What are the benefits of preparing a Bank Reconciliation Statement? | |

|

17.4K Views |

|

4.97/5 Rating |

|

Dec 22, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

video lectures

,Exam

,past year papers

,Semester Notes

,Objective type Questions

,mock tests for examination

,Previous Year Questions with Solutions

,Extra Questions

,NCERT Solution (Part - 1) - Bank Reconciliation Statement | Accountancy Class 11 - Commerce

,MCQs

,NCERT Solution (Part - 1) - Bank Reconciliation Statement | Accountancy Class 11 - Commerce

,Important questions

,shortcuts and tricks

,Viva Questions

,NCERT Solution (Part - 1) - Bank Reconciliation Statement | Accountancy Class 11 - Commerce

,Summary

,practice quizzes

,study material

,Free

,ppt

,Sample Paper

;

NCERT Solution (Part - 1) - Bank Reconciliation Statement Free PDF Download

Importance of NCERT Solution (Part - 1) - Bank Reconciliation Statement

NCERT Solution (Part - 1) - Bank Reconciliation Statement Notes

NCERT Solution (Part - 1) - Bank Reconciliation Statement Commerce Questions

Study NCERT Solution (Part - 1) - Bank Reconciliation Statement on the App

|

© EduRev

|

Education Revolution

|

|