Price & Output Determination under Perfect Competition - Product Pricing, Business Economics | Business Economics & Finance - B Com PDF Download

Perfect competition refers to a market situation where there are a large number of buyers and sellers dealing in homogenous products.

Moreover, under perfect competition, there are no legal, social, or technological barriers on the entry or exit of organizations.

In perfect competition, sellers and buyers are fully aware about the current market price of a product. Therefore, none of them sell or buy at a higher rate. As a result, the same price prevails in the market under perfect competition.

Under perfect competition, the buyers and sellers cannot influence the market price by increasing or decreasing their purchases or output, respectively. The market price of products in perfect competition is determined by the industry. This implies that in perfect competition, the market price of products is determined by taking into account two market forces, namely market demand and market supply.

In the words of Marshall, “Both the elements of demand and supply are required for the determination of price of a commodity in the same manner as both the blades of scissors are required to cut a cloth.” As discussed in the previous chapters, market demand is defined as a sum of the quantity demanded by each individual organizations in the industry.

On the other hand, market supply refers to the sum of the quantity supplied by individual organizations in the industry. In perfect competition, the price of a product is determined at a point at which the demand and supply curve intersect each other. This point is known as equilibrium point as well as the price is known as equilibrium price. In addition, at this point, the quantity demanded and supplied is called equilibrium quantity. Let us discuss price determination under perfect competition in the next sections.

Demand under Perfect Competition:

Demand refers to the quantity of a product that consumers are willing to purchase at a particular price, while other factors remain constant. A consumer demands more quantity at lower price and less quantity at higher price. Therefore, the demand varies at different prices.

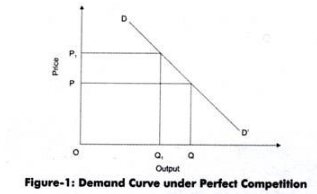

Figure-1 represents the demand curve under perfect competition:

As shown in Figure-1, when price is OP, the quantity demanded is OQ. On the other hand, when price increases to OP1, the quantity demanded reduces to OQ1. Therefore, under perfect competition, the demand curve (DD’) slopes downward.

Supply under Perfect Competition:

Supply refers to quantity of a product that producers are willing to supply at a particular price. Generally, the supply of a product increases at high price and decreases at low price.

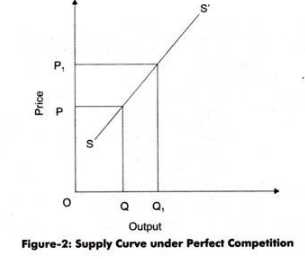

Figure-2 shows the supply curve under perfect competition:

In Figure-2, the quantity supplied is OQ at price OP. When price increases to OP1, the quantity supplied increases to OQ1. This is because the producers are able to earn large profits by supplying products at higher price. Therefore, under perfect competition, the supply curves (SS’) slopes upward.

Equilibrium under Perfect Competition:

As discussed earlier, in perfect competition, the price of a product is determined at a point at which the demand and supply curve intersect each other. This point is known as equilibrium point. At this point, the quantity demanded and supplied is called equilibrium quantity.

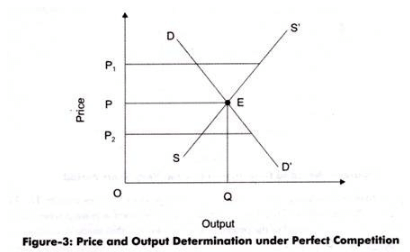

Figure-3 shows the equilibrium under perfect competition:

In Figure-3, it can be seen that at price OP1, supply is more than the demand. Therefore, prices will fall down to OP. Similarly, at price OP2, demand is more than the supply. Similarly, in such a case, the prices will rise to OP. Thus, E is the equilibrium at which equilibrium price is OP and equilibrium quantity is OQ.

|

71 videos|80 docs|23 tests

|

FAQs on Price & Output Determination under Perfect Competition - Product Pricing, Business Economics - Business Economics & Finance - B Com

| 1. What is perfect competition and how does it affect product pricing? |  |

| 2. How is output determined under perfect competition? | |

| 3. What factors influence product pricing under perfect competition? | |

| 4. How does perfect competition benefit consumers? | |

| 5. Can perfect competition exist in the real world? | |

|

4.3K Views |

|

4.92/5 Rating |

|

Dec 19, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

study material

,Important questions

,Price & Output Determination under Perfect Competition - Product Pricing

,shortcuts and tricks

,Business Economics | Business Economics & Finance - B Com

,Business Economics | Business Economics & Finance - B Com

,Previous Year Questions with Solutions

,Free

,Objective type Questions

,past year papers

,MCQs

,Summary

,video lectures

,Price & Output Determination under Perfect Competition - Product Pricing

,Semester Notes

,ppt

,mock tests for examination

,Business Economics | Business Economics & Finance - B Com

,practice quizzes

,Extra Questions

,Exam

,Sample Paper

,Viva Questions

,Price & Output Determination under Perfect Competition - Product Pricing

;

Price & Output Determination under Perfect Competition - Product Pricing, Business Economics Free PDF Download

Importance of Price & Output Determination under Perfect Competition - Product Pricing, Business Economics

Price & Output Determination under Perfect Competition - Product Pricing, Business Economics Notes

Price & Output Determination under Perfect Competition - Product Pricing, Business Economics B Com Questions

Study Price & Output Determination under Perfect Competition - Product Pricing, Business Economics on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|