Principle of Maximum Social Advantage - Public Finance | Public Finance - B Com PDF Download

Principle of Maximum Social Advantage (With Diagrammatic Representation)

The fiscal or budgetary operations of the state have manifold effects on the economy. The revenue collected by the state through taxation and the dispersal of public expenditures can have significant influence on the consumption, production and distribution of the national income of the country.

The fiscal operations of the government resolve themselves into a series of transfers of purchasing power from one section of the community to another, along with the variations in the total incomes available in the community. In fact, the fiscal activities of the state affect the allocation of resources, the use of resources from one channel to another, hence, the level of income, output and employment.

Hence, it is desirable that some standard or criterion should be laid down to judge the appropriateness of a particular operation of public finance — the government’s revenue and expenditures. In a modern welfare state, such a criterion can obviously be nothing else but the economic welfare of the people.

It follows, thus, that the particular financial activity of the state which leads to an increase in economic welfare is considered as desirable. It may be considered as undesirable if such an activity does not cause an increase in the welfare or even sometimes, it may be the cause of a reduction in the general economic welfare. The guiding principle of state policy has been technically desirable as the Principle of Maximum Social Advantage by Hugh Dalton.

According to Dalton, the principle of maximum social advantage is the most fundamental principle lying at the root of public finance. Hence, the best system of public finance is that which secures the maximum social advantage from its fiscal operations. Maximum social advantage is the maxim for the states. The optimum financial activities of a state should, therefore, be determined by the principle of maximum social advantage.

It is obvious that taxation by itself is a loss of utility to the people, while public expenditure by itself is a gain of utility to the community. When the state imposes taxes, some disutility or dissatisfaction is experienced in the society. This disutility is in the form of sacrifice involved in the payment of taxes — in parting with the purchasing power.

Similarly, when the state spends money, some utility is created in the society. Some satisfaction is experienced by a group of people in the society on whom, or for whom, the public expenditure is incurred by the state. This is the social benefit of welfare of the public expenditure.

As such, the maximum social advantage is achieved when the state in its financial activities maximise the surplus of social gain or utility (resulting from public expenditure) over the social sacrifice or disutility (involved in payment of taxes.) The principle of public finance, thus, requires the state to compare the sacrifice and benefits of the society in its fiscal operations.

The principle of maximum social advantage implies that public expenditure is subject to diminishing marginal social benefits and taxes are subject to increasing marginal social costs. Thus, an equilibrium is reached when social advantage is maximised, i.e., when the size of the budget is such that marginal social benefits of public expenditures are equal to the marginal social sacrifice of taxation.

Dalton states, “Public expenditure in every direction should be carried just so far, that the advantages to the community of a further small increase in any direction is just counter-balanced by the disadvantage of a corresponding small increase in taxation or in receipts from any other sources of public expenditure and public income.”

Thus, a rational state seeks to maximise the net social advantage of its fiscal operations. The social net advantage is maximum when the aggregate social benefits resulting from public expenditure is maximum and the aggregate social sacrifice involved in raising the public revenue is minimum. According to the principle of maximum social advantage, thus, the public expenditure should be carried on up to the marginal social sacrifice of the last unit of rupee taxed.

Diagrammatic Representation:

In technical jargon, the maximum social net advantage is achieved when the marginal social sacrifice (disutility) of taxation and the marginal social benefit (utility) of public expenditure are equated. Thus, the point of equality between the marginal social benefit and the marginal social sacrifice is referred to as the point of aggregate maximum social advantage or least aggregate social sacrifice.

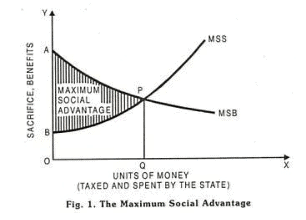

The equilibrium point of maximum social advantage may as well be illustrated by means of a diagram, as in Fig. 1.

In Fig. 1, MSS is the marginal social sacrifice curve. It is an upward sloping curve implying that the social sacrifice per unit of taxation goes on increasing with every additional unit of money raised. MSB is the marginal social benefit curve. It is a downward sloping curve implying that the social benefits per unit diminishes as the public expenditure increases.

The curves MSS and MSB intersect at point P. This equality (P) of MSS and MSB curves is regarded as the optimum limit of the state’s financial activity. It is easy to see that so long as the MSB curve lies above the MSS curve, each additional unit of revenue raised and spent by the state leads to an increase in the net social advantage.

This beneficial process would then be continued till marginal social sacrifice (MSS) becomes just equal to the marginal social benefit (MSB). Beyond this point, a further increase in the state’s financial activity means the marginal social sacrifice exceeding the marginal social benefit, hence the net social loss.

Thus, only under the condition of MSS = MSB, the maximum social advantage is achieved. Diagrammatically, the shaded area APB (the area between MSS and MSB curves, till both intersect each other) represents the quantum of maximum social advantage. OQ is the optimum amount of financial activities of the state.

Further, the ideal of maximum social advantage is attained by the state, if the following principles of financial operation are followed in the budget.

1. Taxes should be distributed in such a way that the marginal utility of money sacrificed by all the tax-payers is the same.

2. Public spending is done, such that benefits derived from the last unit of money spent on each item becomes equal.

3. Marginal benefits and sacrifices must be equated.

To sum up, all fiscal operations, both as regards revenue and expenditure, should be treated as a series of transfer of purchasing power that must ultimately increase the economic welfare of the people. In this context, Dalton enunciated the principle of maximum social advantage and asserted that financial operations of the government must be in accordance with this principle in a welfare state.

|

37 videos|35 docs|15 tests

|

FAQs on Principle of Maximum Social Advantage - Public Finance - Public Finance - B Com

| 1. What is the principle of Maximum Social Advantage in public finance? |  |

| 2. How does the principle of Maximum Social Advantage guide public finance decisions? | |

| 3. What factors are considered when applying the principle of Maximum Social Advantage? | |

| 4. How does the principle of Maximum Social Advantage relate to taxation and public expenditure? | |

| 5. What are the potential challenges in implementing the principle of Maximum Social Advantage in public finance? | |

|

1.8K Views |

|

4.72/5 Rating |

|

Nov 15, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Summary

,video lectures

,ppt

,Exam

,Viva Questions

,Principle of Maximum Social Advantage - Public Finance | Public Finance - B Com

,Sample Paper

,MCQs

,Extra Questions

,Principle of Maximum Social Advantage - Public Finance | Public Finance - B Com

,Semester Notes

,Principle of Maximum Social Advantage - Public Finance | Public Finance - B Com

,mock tests for examination

,Important questions

,past year papers

,Free

,Objective type Questions

,practice quizzes

,Previous Year Questions with Solutions

,study material

,shortcuts and tricks

;

Principle of Maximum Social Advantage - Public Finance Free PDF Download

Importance of Principle of Maximum Social Advantage - Public Finance

Principle of Maximum Social Advantage - Public Finance Notes

Principle of Maximum Social Advantage - Public Finance B Com Questions

Study Principle of Maximum Social Advantage - Public Finance on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|