Rectification of Mistakes, Notice for Demand - Assessment Procedure, Income Tax Laws | Income Tax Laws - B Com PDF Download

It may be possible that an Income tax authority may commit a mistake while passing the order of assessment, appeal, revision etc. With a view to rectifying any mistake, apparent from record, the income tax authority is empowered as under:-

The Income Tax Assessing Officer is empowered to rectify any order of assessment or of refund or any other order passed by him. Further, the assessing officer is also empowered to amend any intimation or deemed intimation under section 143(1).

The Commissioner is empowered to rectify any order passed by him in revision under Section 263 or 264.

The Commissioner (Appeals) may rectify any order passed by him under Section 250.

Other Income Tax Authorities mentioned under Section 116 may also amend any order passed by it.

The Income Tax Authorities may make the rectification:-

On its own motion

On application made by the assessee bringing the mistake to the notice of the authority concerned.

If the authority concerned is Commissioner (Appeals), besides the above, such mistake can be brought to his notice by the Assessing Officer also.

The Appellate Tribunal can rectify its order under Section 254(2) but not under Section 154 as it is not an income tax authority.

If any matter had been considered and decided in any proceeding by way of appeal or revision, rectification of such matter cannot be done by the Assessing Officer under Section 154. However, the matter which has not been considered and decided in the appeal/revision can be rectified under Section 154.

Relevant Points of Section 154

Opportunity of being heard is important if Rectification results in Enhancement-

If such rectification order under Section 154 has the effect of enhancing an assessment, or reducing a refund, or otherwise increasing the liability of the assessee, the authority concerned must give a notice to the assessee of its intention to do so and an opportunity of being heard must be given to the assessee.

Notice of Demand to be issued in case the Rectification results in enhancing the Assessment-

If any such assessment under Section 154 has the effect of enhancing the assessment or reducing a refund already made, the Assessing Officer shall serve on the assessee a notice of demand in the prescribed form specifying the sum payable, and such notice of demand shall be deemed to be issued under Section 156 and the provisions of the income tax act shall apply accordingly.

Time Limit for Rectification under Section 154

Rectification of an order can be made only within 4 years from the end of the financial year in which the order sought to be amended was passed. However, this time limitation shall not apply to cases where amendment is made under Section 155.

The order that is sought to be amended does not necessarily mean the original order. It could be any order including the amended or rectified order.

Time Limit for passing an Order under Section 154 if application for amendment made under Section 154-

If an application for amendment is made by the assessee, the authority shall pass an order within a period of 6 months from the end of the month in which the application is received by it:-

Making the Amendment, or

Refusing to allow the Claim

OTHER RELEVANT POINTS OF SECTION 154

The power of Rectification can be evoked with reference to the law prevailing at the time of the original order.

If the appeal has been filed but the matter has still not been considered and decided in appeal, the rectification is still possible.

If any rectification is made under this section, an order of rectification shall be passed in writing by the income tax authority concerned.

If any such amendment under Section 154 has the effect of reducing the assessment, the Assessing Officer shall make any refund which may be due to the assessee.

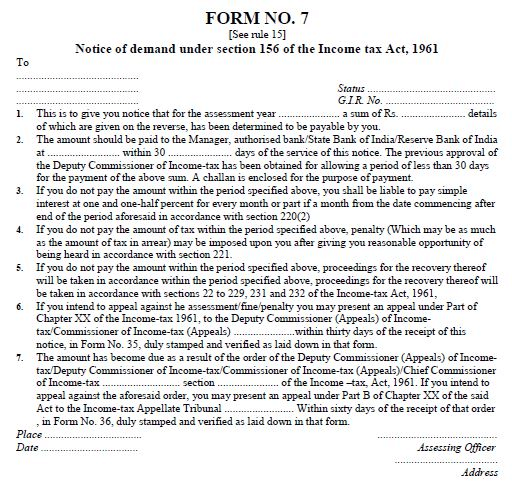

Notice u/s 156 – Notice for Demand

Section 156 tax notice is the notice of demand issued by the Income Tax Department when any tax, interest, penalty, fine or any other sum is payable in consequence of any order passed. The section 156 tax notice of demand will specify the sum which is payable.

This demand notice is generally accompanied by an intimation notice under section 143(1) or along with the assessment order that is issued on completion of the scrutiny proceedings. Notice of Demand u/s 156 is issued in respect of every assessment order for addition to income.

Time Limit

The amount which is demanded in the Section 156 demand notice has to be paid by the Assessee within a period of 30 days after the date of receipt of the notice.

Steps to be taken

If you have received a Section 156 tax notice for demand then you have to follow these steps:

1. Login to Income Tax e-filing portal with your User ID and Password.

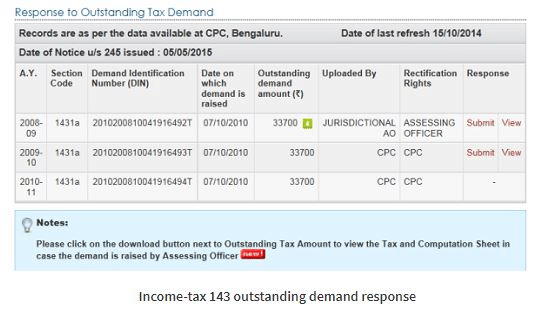

2. Click on the option of “E-file” and then select the option of “Respond to Outstanding Tax Demand“. You’ll get the following window:

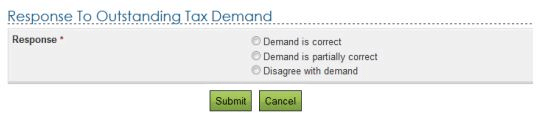

3. Click on “Submit” to submit the response and then you’ll get the following options:

4. If the demanded amount is correct, then you have to select the option of “Demand is correct“. Once the option is selected then you have to pay the tax online through the option of E-Pay Tax and if any amount of refund is due, then the amount of demand will be adjusted with it and you have to pay the balance amount.

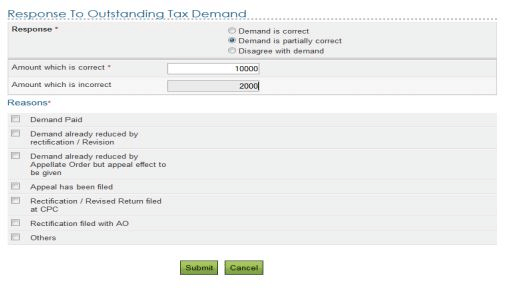

5. If the demanded amount is partially correct, then you have to select the option of “Demand is partially correct“. Then there will be two options available:

Amount which is correct

Amount which is incorrect

Enter the amount which is correct and the incorrect amount will be auto populated and you also have to give a valid reason because of which the demanded amount is incorrect. In this case, the acceptance is subject to approval by the Department.

6. If the demanded amount is incorrect, then you have to select the option of "Disagree with demand". You’ve to select the reason because of which the demanded amount is incorrect. After submitting a reason the success screen would be displayed with the transaction ID. The status of demand will be updated after the response is processed by the IT Department.

Penalty

If the person to whom the section 156 tax notice for demand has been issued fails to pay the amount demanded within the time limit provided under the section 156 tax notice, then the assessee is liable for following penalties:

Interest u/s 220- Interest at the rate of 1% per month or part thereof is payable after the expiry of the 30 days time provided under section 156 tax notice.

Penalty u/s 221- A penalty u/s 221 may be imposed by the AO on the assessee but it should not be more than the amount demanded in the Demand Notice.

|

33 videos|41 docs|11 tests

|

FAQs on Rectification of Mistakes, Notice for Demand - Assessment Procedure, Income Tax Laws - Income Tax Laws - B Com

| 1. What is the process of rectification of mistakes in income tax assessment? |  |

| 2. How can I rectify a mistake in my income tax return after it has been filed? | |

| 3. What is a notice for demand in the assessment procedure of income tax laws? | |

| 4. Can I challenge a notice for demand issued by the income tax department? | |

| 5. What are the consequences of not responding to a notice for demand in income tax assessment? | |

study material

,Income Tax Laws | Income Tax Laws - B Com

,past year papers

,Objective type Questions

,Free

,Extra Questions

,Important questions

,Income Tax Laws | Income Tax Laws - B Com

,Exam

,Income Tax Laws | Income Tax Laws - B Com

,Viva Questions

,Notice for Demand - Assessment Procedure

,video lectures

,Sample Paper

,MCQs

,shortcuts and tricks

,Rectification of Mistakes

,mock tests for examination

,Notice for Demand - Assessment Procedure

,Previous Year Questions with Solutions

,Rectification of Mistakes

,ppt

,Summary

,Semester Notes

,Notice for Demand - Assessment Procedure

,Rectification of Mistakes

,practice quizzes

;

Rectification of Mistakes, Notice for Demand - Assessment Procedure, Income Tax Laws Free PDF Download

Importance of Rectification of Mistakes, Notice for Demand - Assessment Procedure, Income Tax Laws

Rectification of Mistakes, Notice for Demand - Assessment Procedure, Income Tax Laws Notes

Rectification of Mistakes, Notice for Demand - Assessment Procedure, Income Tax Laws B Com Questions

Study Rectification of Mistakes, Notice for Demand - Assessment Procedure, Income Tax Laws on the App

|

© EduRev

|

Education Revolution

|

|