Scanner - Price Determination | SSC CGL Tier 2 - Study Material, Online Tests, Previous Year PDF Download

N.C.E.R.T Questions

(Q1) Explain Market equilibrium

(Q2) When do we say there is excess demand for a commodity in the market ?

(Q3) When do we say there is excess supply for a commodity in the market ?

(Q4) What will happen if the prevailing price in the market is

(i) above the equilibrium price (ii) below the equilibrium price

(Q5) How are equilibrium price and quantity affected when income of the consumer

(a) increases (b) decreases

(Q6) Using supply and demand curve, show how an increase in the price of shoes affects the price of a pair of socks and the number of socks bought and sold.

(Q7) How do the equilibrium price and quantity of a commodity changes when price of input used in its production changes ?

(Q8) How are he equilibrium price and quantity affected when

(a) Both demand and supply changes in same direction

(b) demand and supply curves shift in opposite directions

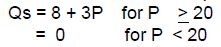

(Q9) Suppose the demand and supply curve of commodity X in a perfectly competitive market

are given by Qd = 700 - P and Qs = 500 + 3P for P  15 , for P < 15

15 , for P < 15

(a) Give reason behind the market supply of commodity X being zero at any price less

than Rs 15 ( ans. minimum average cost)

(b) Find equilibrium price and quantity ?

(Q10) Suppose the demand and supply curve of salt are given by Qd = 1000 - P and Qs = 700 + 2P

(a) Find equilibrium price and quantity

(b) Suppose due to increase in input price new supply curve is Qs = 400 + 2P ? How does the equi. Price and quantity changes ? Does the change conform to your expectation ?

(c) Suppose govt. has imposed a tax of Rs 3 per unit of sale of salt . How does it affect the equilibrium price and quantity ?

(Q11) For a non- viable industry, where does the supply curve lie relative to demand curve?

(Q12) New environmental regulations requires that the drug industry use a more environments - friendly technology whose running costs are higher but which discharges less toxic chemicals than before. How would it affect the price of drugs ?

(Q13) How the following affect the equilibrium price and quantity

(a) increase in the price of a substitute good in consumption

(b) Increase in input price

(c) Cost -saving technological progress

(d) Increases in excise tax rate

(e) Increase in the income of consumer

(f) a severe drought results in a drastic fall in the output of wheat.

(Q14) In the Budget, the excise duty on tea was reduced from Rs 2 to Rs1 per kg. All other things remaining unchanged, how will it affect the market price of tea ?

(Q15) When will an increase in demand imply an increase in price but no change in quantity supplied

(Q16) What is economic viability of an industry ?

(Q17) What will be impact on market price and quantity exchanged when

(a) There is a rightward shift in the demand curve

(b) Demand curve is perfectly elastic and supply curves shifts outward

(c) both the demand and supply curves decreases in the same proportion

(Q18) How are the decision taken by producer and consumers in the market co- ordinated?

(Q19) Mrs. Ramgopal says that economists say inconsistent things “as price falls , demand rises but as demand rises , price rises . Defend or refute

(Q20) There are 10000 identical individual buyers in the market for commodity X each with a demand function given by QD x = 12 - 2 Px and 1000 identical producers of commodity X , each with a supply function given by QSx = 20 Px

(i) Find the market demand function and the market supply function for commodity X

(ii) Obtain the equilibrium price and equilibrium quantity

(iii) Suppose the govt. decides to collect a sales tax of rs 2 per unit sold from each of the 1000 sellers of commodity X . what effect will this have on the equilibrium price and quantity of commodity X ?

Ans Px = 3 , 60000 units and Px = rs 4 , 40000 units

(Q21) The market demand curve for commodity X is Qd = 700 - P .Assume the market consists of identical firms producing commodity X. The supply curve of a

single firm is

(a) What is the significance of p = 20 ?

(b) Calculate equilibrium quantity and number of firms at the equilibrium price of Rs 20

( Ans : 680 units , 10 firms )

C.B.S.E. Questions

(Q1) How is equilibrium price and quantity affected by leftward shift of demand curve? Explain with help of diagram?

(Q2) Define equilibrium price and equilibrium quantity ?

(Q3) Define equilibrium price? Explain with the help of diagram the effect of an increase in demand on the equilibrium price and quantity.

(Q4) “ If the demand and supply of a commodity both increase, the equilibrium price may not change may increase, may decrease “ Explain with diagram

(Q5) With the help of a suitable diagram explain the process of determination of equilibrium price of commodity under perfectly competitive market.

(Q6) Explain how does rightward shift of supply curve effect equilibrium price and quantity?

(Q7) Explain the effect of a leftward shift of demand curve of a commodity on its equilibrium price are equilibrium quantity ? Explain with help of diagram ?

(Q8) How will an increase in the income of the buyers of an “ inferior good”, affect its equilibrium price and equilibrium quantity ? Explain with help of diagram.

(Q9) How is the equilibrium price and equilibrium quantity of a normal commodity affected by an increase in the income of its buyers ? Explain with the help of a diagram.

(Q10) At a given price of a commodity, there is excess supply. Is it an equilibrium price ? If not, how will the equilibrium price be reached ?

(Q11) What can be the effect of a decrease in both the market demand and market supply of a commodity it in its price ? Explain

(Q12) How is equilibrium price determined ? What happen if the market price is more than the equilibrium price?

CBSE 2008 + Sample Paper Questions

(Q1) What happens to equilibrium price of a commodity if there is decrease in its demand and increase in its supply ?(1)

(Q2) Define ‘ equilibrium Price’.

(Q3) Explain the effects of increase in supply of a good on its equilibrium and equilibrium quantity. Use diagram.(4)

(Q4) Explain the effects of increase in supply of a good on its equilibrium price and equilibrium quantity with the help of a schedule.

(Q5) There is a simultaneous decrease in demand and supply of a commodity. When will it result in :

(a) No change in equilibrium price. (b) A fall in equilibrium price. Use Diagram.(6)

(Q6) There is a simultaneous decrease in demand and supply of a commodity .Explain its effect on equilibrium price.

CBSE 2009

(Q1) With the help of a demand and supply schedule, explain the meaning of excess demand and its effect on price of a commodity. (6)

(Q2) Define equilibrium price of a commodity. How is it determined ? Explain with the help of a schedule.

CBSE 2010 + Sample Paper Questions

(Q1) How does the equilibrium price of a ‘normal’ commodity change when income of its buyers fall ? Explain the chain of effects.(4M)

(Q2) There is a simultaneous ‘decrease’ in demand and supply of a commodity. When will it result in : (a) No change in equilibrium price. (b) A fall in equilibrium price. Use diagrams.

(Q3) Give the meaning of equilibrium price.(1 M)

(Q4) Explain the changes that will take place in the market for a commodity if the prevailing market price is less than the equilibrium price.(3 M)

(Q5) What happens to equilibrium price of a commodity if there is an ‘increase’ in its demand and ‘decrease’ in its supply ?(3M)

(Q6) There is a simultaneous ‘decrease’ in demand and supply of a commodity. Explain its effect on equilibrium price.(3M)

CBSE 2011 & CBSE 2012

(Q1) Market for a good is in equilibrium. There is simultaneous “decrease” both in demand and supply but there is no change in market price. Explain with the help of a schedule how it is possible. (6 marks)

(Q2) Market for a good is in equilibrium. Explain the chain of reactions in the market if the price is (i) higher than equilibrium price and (ii) lower than equilibrium price.

(Q3) Market for a good is in equilibrium. There is ‘increase’ in supply of that good. Explain the chain of effects of this change. Use a numerical example.(6 marks)

(Q4) Market for a good is in equilibrium. There is ‘increase’ in supply of the good. Explain the chain of effects of this change. Use diagram.(6 marks)

C.B.S.E & Sample Paper 2013

(Q1) Equilibrium price of an essential medicine is too high. Explain what possible steps can be taken to bring down the equilibrium price but only through the market forces. Also explain the series of changes that will occur in the market.(4 M)

Ans: One possible step can be to reduce tax on medicine (or alternatively give subsidy).

This will bring down cost and in turn ‘increase’ supply. Demand remaining unchanged, a situation of ‘excess supply’ will emerge which will lead to competition between sellers. This will lead to fall in price of the medicine. (Any other individual response with suitable justification should also be accepted)

(Q2) State true or false “ When equilibrium price of a good is less than its market price , there will be competition among the sellers”

Ans: True, because when the prevailing market price is higher than the equilibrium price there will be excess supply, and since the sellers will not be able to sell all they want to sell, there will be competition among sellers.

(Q3) If equilibrium price of a good is greater than its market price, explain all the changes that will take place in the market. Use diagram.(6 M)

(Q4) Market for a necessary good is competitive in which the existing firms are earning supernormal profits . How can the policy of liberalisation by the government help in making the market more competitive in the interest of the consumers ? Explain

Ans: The policy of liberalization encourages new firms to enter the industry. This raises output of the industry. Total market demand remaining unchanged, price starts falling. Consumers now get the good at a cheaper price. (Any other individual response with suitable justification should also be accepted even if there is no reference to the text)

C.B.S.E Paper 2014

(Q1) Market of a commodity is in equilibrium. Demand for the commodity ‘decreases’. Explain the chain of effects of this change till the market again reaches equilibrium. Use diagram.(6M)

(Q2) Market of a commodity is in equilibrium. Demand for the commodity ‘increases’. Explain the chain of effects of this change till the market again reaches equilibrium. Use diagram.

(Q4) Consumption of liquor is responsible for many a serious diseases. How can government reduce its consumption using the market forces ? Explain chain effects of Govt. action.

Sample Paper 2015

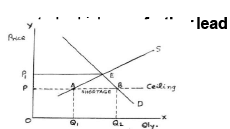

(Q1) Explain the effects of a ‘price ceiling’.(3 M)

Ans: Black marketing may be termed as a direct consequence of price-ceiling, as it implies a situation whereby the commodity under the government’s control policy is illegally sold at a higher price than the one fixed by the government , it may primarily arise due to the presence of consumers who may be willing to pay higher price for the commodity than to go without it.

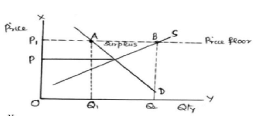

(Q2) Explain the effects of a ‘price floor’.

Ans: Buffer stock is an important tool in the hands of government to ensure price floor/minimum support price. If in case the market price is lower than what the government feels should be given to the farmers/producers it would purchase the commodity at higher price from the farmers/producers so as to maintain stock of the commodity with itself to be released in case of shortage of the commodity in future.

(Q3) Suppose the demand and supply curves of a Commodity-X is given by the following two equations simultaneously: Qd = 200 – p , Qs = 50 + 2p (i) Find the equilibrium price and equilibrium quantity. (ii) Suppose that the price of a factor of production producing the commodity has changed, resulting in the new supply curve given by the equation Qs’ = 80 +2p Analyse the new equilibrium price and new equilibrium quantity as against the original equilibrium price and equilibrium quantity. (3+3)

Ans: (a) Equilibrium Price p = 50 and Equilibrium Quantity q = 150 units (3m) (b) If the price of factor of production has changed, then under the new conditions; Qd = Qs , 200- p = 80 + 2p , (-) 3p = (-) 120Therefore, Equilibrium Price p = 40 and Equilibrium Quantity q = 200 – 40 = 160 units Thus as the equilibrium price is decreasing the equilibrium quantity is increased. (3m)

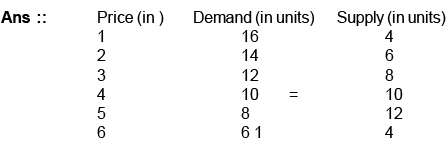

(Q4) Using appropriate schedules, briefly describe the determination of market equilibrium. (3)

Explanation – in the above schedule the market equilibrium is established at price of 4 where the quantity demanded and quantity supplied are equal, with equilibrium quantity of 10 units. (Any other valid schedule with explanation is also correct)

C.B.S.E Paper 2015

(Q1) What are the effects of ‘price-floor’ (minimum price ceiling) on the market of a good ? Use diagram.(3 M)

Ans: W hen government imposes lower limit on a price that may be charged for a particular good or service, it is called minimum price ceiling e.g. price OP1. At this price the producers are willing to supply P1B or (OQ2) While consumers demand onlyP1A (=OQ1). Unable to sell all they want to sell, the producers may try to illegally sell below the minimum price. (Answer based on minimum wages is also correct) (2M)

(Q2) Explain the effects of ‘maximum price ceiling’ on the market of a good ? Use diagram.

Ans: Maximum price ceiling refers to imposition of upper limit on the price of a good by the government. For example, in the diagram OP is price ceiling while equilibrium price is OP1. At this price the producers are willing to supply only PA (Or OQ1) while consumers demand PB (Or OQ2). The ceiling is normally imposed on goods needed by masses, like wheat, rice,sugar etc.

(Q3) Market for a good is in equilibrium. The supply of the good “increases”. Explain the chain of effects of this change.(6 M)

Ans: Given equilibrium, supply ‘increases.’

- Price remaining unchanged, excess supply emerges.

- Excess supply leads to competition among sellers causing price to fall.

- Fall in price causes rise (expansion) in demand and fall (contraction) in supply.

- These changes continue till the market is in equilibrium again at a lower price

(Q4) Market for a good is in equilibrium. Demand for the good “increases”. Explain the chain of effects of this change.(6 M)

Ans: Given equilibrium, demand increases.

- Price remaining unchanged, excess demand emerges.

- This leads to competition among buyers causing price to rise.

- Rise in price causes fall (contraction) in demand and rise (expansion) in supply.

- The price continues to rise till the market is in equilibrium again at a higher price (Diagram not required)

(Q5) Market for a good is in equilibrium. The supply of good “decreases”. Explain the chain ofeffects of this change.(6 M)

(Q6) Suppose the demand and supply curves of a Commodity-X is given by the following two equations simultaneously:

Qd = 200 – p Qs = 50 + 2p

(i) Find the equilibrium price and equilibrium quantity.

(ii) Suppose that the price of a factor of production producing the commodity has changed, resulting in the new supply curve given by the equation

Qs’ = 80 + 2p

Analyse the new equilibrium price and new equilibrium quantity as against the original equilibrium price and equilibrium quantity.[SP (3+3M)]

(Q7) The market for commodity X is in equilibrium. The price of inputs rises. Explain with the help of a diagram its chain of effects on equilibrium price, quantity demanded and quantity supplied.[Delhi (C)]

(Q8) Give the meaning of excess demand. Explain its chain of effects on equilibrium price, quantity demanded and quantity supplied.[Delhi (C)]

|

1335 videos|1432 docs|834 tests

|

FAQs on Scanner - Price Determination - SSC CGL Tier 2 - Study Material, Online Tests, Previous Year

| 1. What factors determine the price of scanners? |  |

| 2. How did the price of scanners change from 2008 to 2015? | |

| 3. Which brands of scanners are known for offering affordable prices? | |

| 4. Are there any specific features that affect the price of scanners significantly? | |

| 5. How can one find the best deals on scanners to get the lowest price? | |

practice quizzes

,Online Tests

,Previous Year

,Scanner - Price Determination | SSC CGL Tier 2 - Study Material

,Online Tests

,Sample Paper

,video lectures

,Previous Year

,Scanner - Price Determination | SSC CGL Tier 2 - Study Material

,Previous Year Questions with Solutions

,Scanner - Price Determination | SSC CGL Tier 2 - Study Material

,Summary

,Previous Year

,Viva Questions

,Objective type Questions

,Important questions

,ppt

,Free

,Exam

,Online Tests

,Semester Notes

,past year papers

,mock tests for examination

,MCQs

,shortcuts and tricks

,study material

,Extra Questions

;

Scanner - Price Determination Free PDF Download

Importance of Scanner - Price Determination

Scanner - Price Determination Notes

Scanner - Price Determination SSC CGL Questions

Study Scanner - Price Determination on the App

|

© EduRev

|

Education Revolution

|

|