Short Answer Questions - Accounting for partnership firms: Fundamentals | Accountancy Class 12 - Commerce PDF Download

Q1 Define partnership.

Ans. When two or more persons enter into an agreement to carry on business and share its

profit and losses, it is a case of partnership. The Indian partnership Act, 1932, defines

Partnership as follows:

"Partnership is the relation between persons and who have agreed to share the profits of

a business carried on by all or any of them acting for all.

Q.2 What do you understand by 'partners', 'firm' and 'firms' name?

Ans. The persons who have entered in to a Partnership with one another are individually

called 'Partners' and collectively 'a firm' and the name under which the business is

carried is called 'the firm's name'.

Q.3 Write any four main features of partnership.

Ans. Essential elements or main features of Partnership :

i) Two or more persons: Partnership is an association of two or more persons.

ii) Agreement: The Partnership is established by an agreement either oral or in

writing.

iii) Lawful Business: A Partnership formed for the purpose of carrying a business, it

must be a legal business.

iv) Profit sharing: Profit of the firm is share by the partners in an agreed ration, if the

ratio is not agreed then equally. Profit also includes loss.

Q.4 What is the minimum and maximum number of partners in all partnership?

Ans. There should be at least two persons to form a Partnership. The maximum number of

Partners in a firm carrying an banking business should not exceed ten and in any other

business should not exceed ten and in any other business it should not exceed twenty.

Q.5 What is the status of partnership from an accounting viewpoint?

Ans. From an accounting viewpoint, partnership is a separate business entity. From legal

viewpoints, however, a Partnership, like a sole proprietorship, is not separate from the

owners.

Q.6 What is meant by partnership deed?

Ans. Partnership deed is a written agreement containing the terms and conditions agreed by

the Partners.

Q.7 State any four contents of a partnership deed.

Ans. i) The date of formation and the duration of the Partnership

ii) Name and address of the Partners

iii) Name of the firm.

iv) Interest on Partners capital and drawings

v) Ratio in which profit or losses shall be shared

Q.8 In the absence of a partnership deed, how are mutual relations of partners governed?

Ans. In the absence of Partnership deed, mutual relations are governed by the Partnership

Act, 1932.

Q.9 Give any two reason in favour of having a partnership deed.

Ans. i) In case of any dispute or doubt, Partnership deed is the guiding document.

ii) It can specify the duties and powers of each Partner.

Q.10 State the provision of 'Indian partnership Act 1932‘ relating to sharing of profits in

absence of any provision in the partnership deed.

Ans. In the absence of any provision in the Partnership deed, profit or losses are share by the

Partners equally.

Q.11 Why is it important to have a partnership deed in writing?

Ans. Partnership deed is important since it is a document defining relationship of among

Partners thus is assistance in settlement of disputes, if any and also avoids possible

disputes: it is good evidence in the court.

Q.12 What do you understand by fixed capital of partners?

Ans. Partners' capital is said to be fixed when the capital of Partners remain unaltered except

in the case where further capital is introduced or capital is withdrawn permanently.

Q.13 What do you understand by fluctuating capital of partners?

Ans. Partner‘s capital is said to be fluctuating when capital alters with every transaction in

the capital account. For example, drawing, credit of interest, etc

Q.14 Give two circumstances in which the fixed capital of partners may change.

Ans. Two circumstances in which the fixed capital of Partners may change are :

i) When additional capital is introduced by the Partners.

ii) When a part of the capital is permanently withdrawn by the Partners.

Q.15 List the items that may appear on the debit side and credit side of a partner's fluctuating

capital account.

Ans. On debit side: Drawing, interest on drawing, share of loss, closing credit balance of the

capital.

On credit side : Opening credit balance of capital, additional capital introduced, share

of profit, interest on capital, salary to a Partner, commission to a Partner.

Q.16 How will you show the following in case the capitals are?

i) Fixed and ii) Fluctuating

a) Additional capital introduced

b) Drawings

c) Withdrawal of capital

d) Interest on capital and

e) Interest on loan by partners?

Ans.i) In case, capitals are fixed:

a) On credit side of capital

(b) on debit side of current A/c

(c) on debit side of capital A/c

(d) on credit side of current A/c

(e) on credit side of loan from

partner's A/c

Q.17 If the partners capital accounts are fixed, where will you record the following items :

i) Salary to partners

ii) Drawing by a partners

iii) Interest on capital and

iv) Share of profit earned by a partner?

Ans. i) Credit side of Partner's current A/c

ii) Debit side of Partner's current A/c

iii) Credit side of Partners current A/c

iv) Credit side of Partners current A/c

Q.18 How would you calculate interest on drawings of equal amounts drawn on the Last day

of every month?

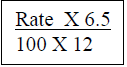

Ans. When a partners draws a fixed amount at the beginning of each month, interest on total

drawing would be on the amount withdraw for 6.5 months at the agreed rate of interest

per annum. Apply the following formula.

Interest on drawing = total drawing x

Q.19 How would you calculate interest on drawing of equal amounts drawn on the last day

of every month?

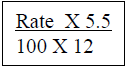

Ans. When drawing of fixed amounts are made at regular monthly intervals on the day of

every month, Interest would be charged on the amount withdrawn at the agreed rate of

interest for 5.5 months. Apply the following formula. :

Interest on drawing = Total drawing x

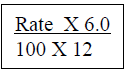

Q.20 How would you calculate interest on drawing of equal amount drawn in the middle of

every month?

Ans. Interest on drawing = Total drawing

Q.21 Ramesh, a partner in the firm has advanced a loan of a Rs. 1,00,000 to the firm and has

demanded on interest @ 9% per annum. The partnership deed is silent on the matter.

How will you deal with it?

Ans. Since the Partnership deed is silent on payment of interest, the provisions of the

Partnership Act, 1932 will apply. Accordingly, Ramesh is entitled to interest @ 6% p.a.

Q.22 The partnership deed provides that Anjali, the partner will get Rs. 10,000 per month as

salary. But, the remaining partners object to it. How will this matter be resolved?

Ans. No, he is not entitled to the salary because it is not so, Provided in the Partnership deed

and according to the Partnership act, 1932 if the Partnership deed does not provided for

payment of salary to Partners, he will not be entitled to it.

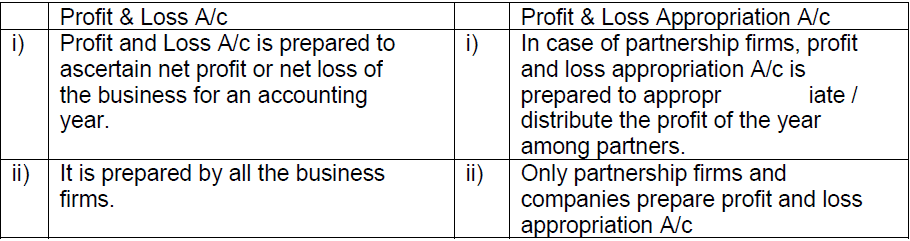

Q.23 Distinction between Profit and loss and profit and loss appropriation account:

Ans.

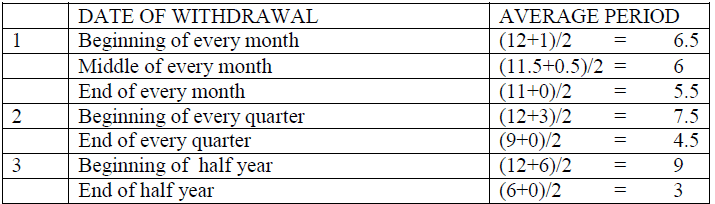

Q.24. State the Average period to be taken for calculating interest on drawing in different cases if

amount is withdrawn on regular interval.

Ans. TABLE SHOWING THE AVERAGE PERIOD WHEN WITHDRAWALS ARE

MADE REGULARLY

|

42 videos|168 docs|43 tests

|

FAQs on Short Answer Questions - Accounting for partnership firms: Fundamentals - Accountancy Class 12 - Commerce

| 1. What is accounting for partnership firms? |  |

| 2. What are the advantages of partnership firms? | |

| 3. What are the different types of partnership firms? | |

| 4. What are the legal requirements for partnership firms? | |

| 5. How are profits and losses shared in a partnership firm? | |

|

14.5K Views |

|

4.90/5 Rating |

|

Dec 26, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

Short Answer Questions - Accounting for partnership firms: Fundamentals | Accountancy Class 12 - Commerce

,ppt

,Semester Notes

,practice quizzes

,Exam

,Short Answer Questions - Accounting for partnership firms: Fundamentals | Accountancy Class 12 - Commerce

,MCQs

,Previous Year Questions with Solutions

,study material

,mock tests for examination

,Free

,Short Answer Questions - Accounting for partnership firms: Fundamentals | Accountancy Class 12 - Commerce

,Objective type Questions

,past year papers

,shortcuts and tricks

,Sample Paper

,Summary

,video lectures

,Important questions

,Extra Questions

,Viva Questions

;

Short Answer Questions - Accounting for partnership firms: Fundamentals Free PDF Download

Importance of Short Answer Questions - Accounting for partnership firms: Fundamentals

Short Answer Questions - Accounting for partnership firms: Fundamentals Notes

Short Answer Questions - Accounting for partnership firms: Fundamentals Commerce

Study Short Answer Questions - Accounting for partnership firms: Fundamentals on the App

|

© EduRev

|

Education Revolution

|

|