Short Questions & Answer - Financial Statements of a Company | Accountancy Class 12 - Commerce PDF Download

Q1 :

What is public company?

Answer :

A public company is defined as a company that offers a part of its ownership in the form of shares, debentures, bonds, securities to the general public through stock market. There must be atleast seven members to form a public company. As per the section 3 (1) (iv) of Companies Act 1956, public company means a company which:

a) is not a private company,

b) has a minimum paid up capital of Rs 5,00,000 or such higher paid up capital, as may be prescribed,

c) is a private company, being a subsidiary of a company which is not a private company.

A public company should not be mistakenly understood as a publicly-owned company, as the latter is exclusively owned and controlled by the government. A public company issues its share to general public without any restriction on maximum number of persons. A public company can be segmented into two types:

1. Listed Company- A Company whose shares are listed and traded in the stock exchange like, Tata Motors, Reliance, etc.

2. Unlisted Company- A Company whose shares are not listed in the stock exchange and thereby these shares cannot be traded in the stock exchange.

Q2 :

Explain the nature of the financial statements.

Answer :

The financial statements are the end-products of the accounting process. The financial statements not only reveal the true financial position of the company but also help various accounting users in decision making and policy designing process. The nature of the financial statements depends upon the following aspects like recorded facts, conventions, concepts, and personal judgment

1. Recorded facts- The items recorded in the financial statements reflect their original cost i.e. the cost at which they were acquired. Consequently, financial statements do not reveal the current market price of the items. Further, financial statements fail to capture the inflation effects.

2. Conventions- The preparation of financial statements is based on some accounting conventions like, Prudence Convention, Materiality Convention, Matching Concept, etc. The adherence to such accounting conventions makes financial statements easy to understand, comparable and reflects the true and fair financial position of the company.

3. Accounting Assumptions - These basic accounting assumptions like Going Concern Concept, Money Measurement Concept, Realisation Concept, etc are called as postulates. While preparing financial statements, certain postulates are adhered to. The nature of these postulates is reflected in the nature of the financial statements.

4. Personal Judgments- Personal value judgments play an important role in deciding the nature of the financial statements. Different judgments are attached to different practices of recording transactions in the financial statements. For example, recording stock either at market value or at the cost requires value judgment. Similarly, provision on various assets, method of charging depreciation, period related to writing off intangible assets depends on personal judgment. Thus, personal judgments determine the nature of the financial statements to a great extent.

Q3 :

What is private limited company?

Answer :

Private limited company is a company that is limited by shares or by guarantee by its members. A private company is defined as a company that has a minimum paid up share capital of Rs 1,00,000. As defined by the Section 3 (1) (iii) of Companies Act 1956, private limited company is defined by the following characteristics.

a) It restricts the right to transfer its shares.

b) There must be atleast two and a maximum of 50 members (excluding current and former employees) to form a private company.

c) It cannot invite application from the general public to subscribe its shares, or debentures.

d) It cannot invite or accept deposits from persons other than its members, Directors and their relatives.

Unlike public company, a private company cannot issue its shares or debentures to general public at large as shares of these companies are not traded in the stock exchange, for example, Coca-Cola India Private limited, etc.

Q4 :

Explain in detail about the significance of the financial statements.

Answer :

The importance of financial statements is mentioned below.

1. Provides Information- Financial statements provide information to various accounting users both internal as well as external users. It acts as a basic platform for different accounting users to derive information according to varying needs. For example, the financial statements on one hand help the shareholders and investors in assessing the viability and return on their investments, while on the other hand, the financial statements help the tax authorities in calculating the amount of tax liability of the company.

2. Cash Flow- Financial statements provide information about the cash flows of the company. The financial statements help the creditors and other investors in determining solvency of company.

3. Effectiveness of Management- The comparability feature of the financial statements enables management to undertake comparisons like inter-firm and intra-firm comparisons. This not only helps in assessing the viability and performance of the business but also helps in designing policies and drafting policies. The financial statements enhance the effectiveness and efficacy of the management.

4. Disclosure of Accounting Policies- Financial statements provide information about the various policies, important changes in the methods, practices and process of accounting by the company. The disclosure of the accounting policies makes financial statements simple, true and enables different accounting users to understand without any ambiguity.

5. Policy Formation by Government- It needs information to determine national income, GDP, industrial growth, etc. The accounting information assist the government in the formulation of various policy measures and to address various economic problems like employment, poverty etc.

6. Attracts Investors and Potential Investors- They invest or plan to invest in the business. Hence, in order to assess the viability and prospectus of their investment, creditors need information about profitability and solvency of the business.

Q5 :

Define Government Company?

Answer :

As per the Section 617 of Company Act of 1956, a Government Company means any company in which not less than 51% of the paid up share capital is held by the Central Government, or by any State Government or Governments, or partly by the Central Government and partly by one on more State Governments and includes a company which is a subsidiary of a Government Company as thus defined.

Q6 :

Explain the limitations of financial statements.

Answer :

The following are the limitations of financial statements.

1. Historical Data- The items recorded in the financial statements reflect their original cost i.e. the cost at which they were acquired. Consequently, financial statements do not reveal the current market price of the items. Further, financial statements fail to capture the inflation effects.

2. Ignorance of Qualitative Aspect- Financial statements does not reveal the qualitative aspects of a transaction. The qualitative aspects like colour, size and brand position in the market, employee's qualities and capabilities are not disclosed by the financial statements.

3. Biased- Financial statements are based on the personal judgments regarding the use of methods of recording. For example, the choice of practice in the valuation of inventory, method of depreciation, amount of provisions, etc. are based on the personal value judgments and may differ from person to person. Thus, the financial statements reflect the personal value judgments of the concerned accountants and clerks.

4. Inter- firm Comparisons- Usually, it is difficult to compare the financial statements of two companies because of the difference in the methods and practices followed by their respective accountants.

5. Window dressing- The possibility of window dressing is probable. This might be because of the motive of the company to overstate or understate the assets and liabilities to attract more investors or to reduce taxable profit. For example, Satyam showed high fixed deposits in the Assets side of its Balance Sheet for better liquidity that gave false and misleading signals to the investors.

6. Difficulty in Forecasting- Since the financial statements is based on historical data, so they fail to reflect the effect of inflation. This drawback makes forecasting difficult.

Q7 :

What do you mean by a listed company?

Answer :

Those public companies whose shares are listed and can be traded in a recognised stock exchange for public trading like, Tata Motors, Reliance, etc are called Listed Company. These companies are also called Quota Companies. The listing of securities (shares) helps the investor to determine the increase/decrease in value of their investment in a concerned listed company. This provides ample indication to the potential investors about the goodwill of the company and facilitates them to take various investment decisions and also to assess the viability of their investment in a company.

Q8 :

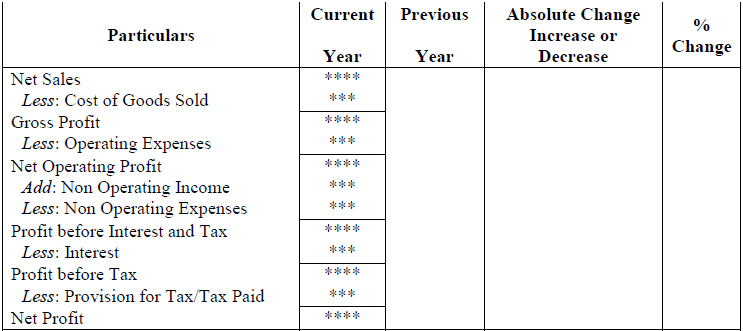

Prepare the format of income statement and explain its elements.

Answer :

Vertical Form of Income Statement

Elements of Income Statement:-

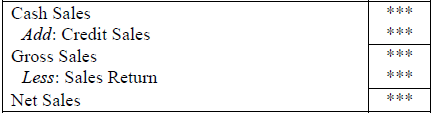

1. Net Sales- Net Sales are derived as:

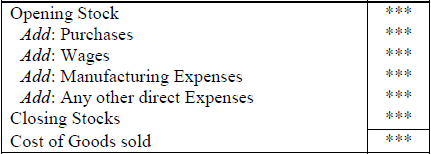

2. Cost of Goods Sold- It is derived as:

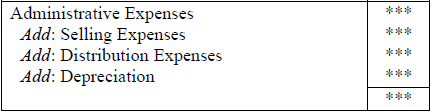

3. Operating Expenses- It is derived as:

Q9 :

What are the uses of securities premium?

Answer :

As per the Section 78 of the Companies Act of 1956, the amount of securities premium can be used by the company for the following activities.

1. For paying up un issued shares of the company to be issued to members (shareholders) of the company as fully paid bonus share,

2. For writing off the preliminary expenses of the company,

3. For writing off the expenses of, or the commission paid or discount allowed on, any issue of shares or debentures of the company,

4. For paying up the premium that is to be payable on redemption of preference shares or debentures of the company.

5. Further, as per the Section 77A, the securities premium amount can also be utilised by the company to Buy-back its own shares.

Q10 :

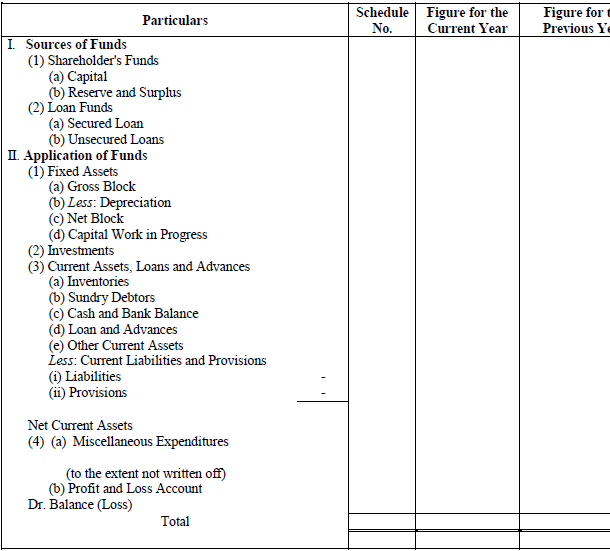

Prepare the format of balance sheet and explain the various elements of balance sheet.

Answer.

Vertical Form of Balance Sheet

Elements of Balance Sheet

1. Share Capital: It is the first item on the Liabilities side. It consists of the following items:

a) Authorised Capital

b) Issued Capital: Equity share and preference share.

c) Subscribed Capital less Call in Arrears add Forfeited Shares

2. Reserve and Surplus: As per the Schedule VI, it consists of the following items:

a) Capital Reserve

b) Capital Redemption Reserve

c) Security Premium

d) Other Reserve less Debit balance of P & L A/c

e) Surplus: Credit balance of P & L A/c

f) Proposed Additions

g) Sinking Fund

3. Secured Loans

a) Debentures

b) Loan and advances from bank etc.

4. Unsecured Loans

a) Fixed Deposits

b) Loan & Advances from subsidiaries

5. Fixed Assets: These are those assets that are used for more than one year, like:

a) Goodwill

b) Land

c) Building

d) Plant & Machinery

e) Patents, Trade Marks

f) Livestock

g) Vehicles, etc.

6. Current Assets: Assets that can be easily converted into cash or cash equivalents are termed as current assets. These are required to run day to day business activities; for example, cash, debtors, stock, etc.

7. Current Liabilities: Those liabilities that are incurred with an intention to be paid or are payable within a year; for example, bank overdraft creditors, bills payable, outstanding wages, short-term loans, etc are called current liabilities.

|

42 videos|199 docs|43 tests

|

FAQs on Short Questions & Answer - Financial Statements of a Company - Accountancy Class 12 - Commerce

| 1. What are financial statements of a company? |  |

| 2. How do financial statements help in evaluating a company's performance? | |

| 3. What is the purpose of an income statement in financial statements? | |

| 4. How does a balance sheet contribute to financial statements? | |

| 5. What is the significance of a cash flow statement in financial statements? | |

shortcuts and tricks

,Exam

,Sample Paper

,MCQs

,ppt

,Semester Notes

,study material

,Short Questions & Answer - Financial Statements of a Company | Accountancy Class 12 - Commerce

,practice quizzes

,Objective type Questions

,Free

,Summary

,Previous Year Questions with Solutions

,Viva Questions

,Important questions

,past year papers

,Short Questions & Answer - Financial Statements of a Company | Accountancy Class 12 - Commerce

,video lectures

,mock tests for examination

,Short Questions & Answer - Financial Statements of a Company | Accountancy Class 12 - Commerce

,Extra Questions

;

Short Questions & Answer - Financial Statements of a Company Free PDF Download

Importance of Short Questions & Answer - Financial Statements of a Company

Short Questions & Answer - Financial Statements of a Company Notes

Short Questions & Answer - Financial Statements of a Company Commerce

Study Short Questions & Answer - Financial Statements of a Company on the App

|

© EduRev

|

Education Revolution

|

|