Statement of Cash Flows (Cash Flow Statement) - Financial Analysis and Reporting | Financial Analysis and Reporting - B Com PDF Download

The Cash Flow statement

Overview

The Cash flow statement is a very important financial statement, as it reveals how much cash the company is actually generating. Is this information not revealed in the P&L statement you may think? Well, the answer is both a yes and a no.

Consider the following scenario.

Assume a simple coffee shop selling coffee and short eats. All the sales the shop does is mostly on cash basis, meaning if a customer wants to have a cup of coffee and a snack, he needs to have enough money to buy what he wants. Going by that on a particular day, assume the shop manages to sell Rs.2,500/- worth of coffee and Rs.3,000/- worth of snacks. It is evident that the shop’s income is Rs.5,500/- for that day. Rs.5,500/- is reported as revenues in P&L, and there is no ambiguity with this.

Now think about another business that sells laptops. For sake of simplicity, let us assume that the shop sells only 1 type of laptop at a standard fixed rate of Rs.25,000/- per laptop. Assume on a certain day, the shop manages to sells 20 such laptops. Clearly the revenue for the shop would be Rs.25,000 x 20 = Rs.500,000/-. But what if 5 of the 20 laptops were sold on credit? A credit sale is when the customer takes the product today but pays the cash at a later point in time. In this situation here is how the numbers would look:

Cash sale: 15 * 25000 = Rs.375,000/-

Credit sale: 5 * 25000 = Rs.125,000/-

Total sales: Rs.500,000/-

If this shop was to show its total revenue in its P&L statement, you would just see a revenue of Rs.500,000/- which may seem good on the face of it. However, how much of this Rs.500,000/- is actually present in the company’s bank account is not clear. What if this company had a loan of Rs.400,000/- that had to be repaid back urgently? Even though the company has a sale of Rs.500,000 it has only Rs.375,000/- in its account. This means the company has a cash crunch, as it cannot meet its debt obligations.

The cash flow statement captures this information. A statement of cash flows should be presented as an integral part of an entity’s financial statements. Hence in this context evaluation of the cash flow statement is highly critical as it reveals amongst other things, the true cash position of the company.

To sum up, every company’s financial performance is not so much dependent on the profits earned during a period, but more realistically on liquidity or cash flows.

Activities of a company

Before we go ahead to understand the cash flow statement, it is important to understand ‘the activities’ of a company. If you think about a company and the various business activities it undertakes, you will realize that the company’s activities can be classified under one of the three standard baskets. We will understand this in terms of an example.

Imagine a business, maybe a very well established fitness center (Talwalkars, Gold’s Gym etc) with a sound corporate structure. What are the typical business activities you think a fitness center would have? Let me go ahead and list a few business activities:

- Display advertisements to attract new customers

- Hire fitness instructors to help clients in their fitness workout

- Buy new fitness equipments to replace worn out equipments

- Seek short term loan from bankers

- Issue a certificate of deposit for raising funds

- Issue new shares to a few known friends to raise fresh capital for expansion (also called preferential allotment)

- Invest in a startup company working towards innovative fitness regimes

- Park excess money (if any) in fixed deposits

- Invest in a building coming up in the neighborhood, for opening a new fitness center sometime in the future

- Upgrade the sound system for a better workout experience

As you can see the above listed business activities are quite diverse however they are all related to the business. We can classify these activities as:

- Operational activities (OA): Activities that are directly related to the daily core business operations are called operational activities. Typical operating activities include sales, marketing, manufacturing, technology upgrade, resource hiring etc.

- Investing activities (IA): Activities pertaining to investments that the company makes with an intention of reaping benefits at a later stage. Examples include parking money in interest bearing instruments, investing in equity shares, investing in land, property, plant and equipment, intangibles and other non current assets etc

- Financing activities (FA): Activities pertaining to all financial transactions of the company such as distributing dividends, paying interest to service debt, raising fresh debt, issuing corporate bonds etc

All activities a legitimate company performs can be classified under one of the above three mentioned categories.

Keeping the above three activities in perspective, we will now classify each of the above mentioned activities into one of the three categories /baskets.

- Display advertisements to attract new customers – OA

- Hire fitness instructors to help customers with their fitness workout – OA

- Buy new fitness equipment to replace worn out equipments – OA

- Seek a short term loan from bankers – FA

- Issue a certificate of deposit (CD) for raising funds – FA

- Issue new shares to few known friends to raise fresh capital for expansion (also called preferential allotment) – FA

- Invest in a startup company working towards innovative fitness regimes – IA

- Park excess money (if any) in fixed deposit – IA

- Invest in a building coming up in the neighborhood for opening a new fitness center sometime in the future – IA

- Upgrade the sound system for better workout experience- OA

Now think about the cash moving in and out of the company and its impact on the cash balance. Each activity that the company undertakes has an impact on cash. For example “Upgrade the sound system for a better workout experience” means the company has to pay money towards the purchase of a new sound system, hence the cash balance decreases. Also, it is interesting to note that the new sound system itself will be treated as a company asset.

Keeping this in perspective, we will now understand for the example given above how the various activities listed would impact the cash balance and how would it impact the balance sheet.

|

Activity No |

Activity Type |

Rational |

Cash Balance |

On Balance Sheet |

|

1 |

OA |

Expenditure towards advertisement |

Decreases |

Treated as an asset as it increases the brand value |

|

2 |

OA |

Expenditure towards new recruits |

Decreases |

Treated as an asset as it increases the company’s intellectual capital |

|

3 |

OA |

Expenditure towards new equipment |

Decreases |

Treated as asset |

|

4 |

FA |

Loan means cash inflow to business |

Increases |

Loan is a liability |

|

5 |

FA |

Deposits via CD means cash inflow |

Increases |

CD is a liability |

|

6 |

FA |

Issue of fresh capital means cash inflow |

Increases |

Treated as a liability as share capital increases |

|

7 |

IA |

Investment in startup means cash outflow |

Decreases |

Investment is an asset |

|

8 |

IA |

Money parked in FD means cash going out of business |

Decreases |

Equivalent to cash, hence considered an asset |

|

9 |

IA |

Investment in building means cash going out of business |

Decreases |

Gross block considered an asset |

|

10 |

OA |

Expenditure towards the sound system |

Decreases |

Treated as an asset |

- Increase in cash is colour coded in blue

- Decrease in cash is colour coded in red

- Assets are colour coded in green and

- Liabilities are colour coded in purple.

If you look through the table and start correlating the ‘Cash Balance’ and ‘Asset/Liability’ you will observe that:

- Whenever the liabilities of the company increases the cash balance also increases

This means if the liabilities decreases, the cash balance also decreases - Whenever the asset of the company increases, the cash balance decreases

This means if the assets decreases, the cash balance increases

The above conclusion is the key concept while constructing a cash flow statement. Also, extending this further you will realize that each activity of the company be it operating activity, financing activity, or investing activity either produces cash (net increase in cash) or reduces (net decrease in cash)the cash for the company.

Hence the total cash flow for the company will be:-

Cash Flow of the company = Net cash flow from operating activities + Net Cash flow from investing activities + Net cash flow from financing activities

The Cash Flow Statement

Having some insight into the cash flow statement, you would now appreciate the fact that you need to look into the cash flow statement to review the company from a cash perspective.

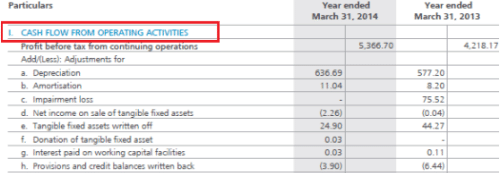

Typically when companies present their cash flow statement they split the statement into three segments to explicitly show how much cash the company has generated across the three business activities. Continuing with our example from the earlier chapters, here is the cash flow statement of Amara Raja Batteries Limited (ARBL):

I will skip going through each line item as most of them are self explanatory, however I want you to notice that ARBL has generated Rs.278.7 Crs from operating activities. Note, a company which has a positive cash flow from operating activities is always a sign of financial well being.

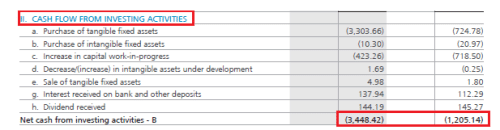

Here is the snapshot of ARBL’s cash flow from investing activities:

As you can see, ARBL has consumed Rs.344.8 Crs in its investing activities. This is quite intuitive as investing activities tend to consume cash. Also remember healthy investing activities foretells the investor that the company is serious about its business expansion. Of course how much is considered healthy and how much is not, is something we will understand as we proceed through this module.

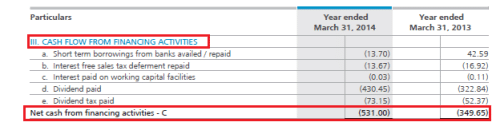

Finally, here is the snapshot of ARBL’s cash balance from financing activities:

ARBL consumed Rs.53.1Crs through its financing activities. If you notice the bulk of the money went in paying dividends. Also, if ARBL takes on new debt in future it would lead to an increase in the cash balance (remember increase in liabilities, increases cash balance). We know from the balance sheet that ARBL did not undertake any new debt.

Let us summarize the cash flow from all the activities:

| Cash Flow from | Rupees Crores (2013-14) | Rupees Crores (2012-13) |

|---|---|---|

| Operating Activities | 278.7 | 335.4 |

| Investing Activities | (344.8) | (120.05) |

| Financing Activities | (53.1) | (34.96) |

| Total | (119.19) | 179.986 |

This means the company consumed a total cash of Rs.119.19 Crs for the financial year 2013 -2014. Fair enough, but what about the cash from the previous year? As we can see, the company generated Rs.179.986 Crs through all its activities from the previous year. Here is an extract from ARBL’s cash flow statement:

Look at the section highlighted in green (for the year 2013-14). It says the opening balance for the year is Rs.409.46Crs. How did they get this? Well, this happens to be the closing balance for the previous year (refer to the arrow marks). Add to this the current year’s cash equivalents which is (Rs.119.19) Crs along with a minor forex exchange difference of Rs.2.58 Crs we get the total cash position of the company which is Rs.292.86 Crs. This means, while the company guzzled cash on a yearly basis, they still have adequate cash, thanks to the carry forward from the previous year.

Note, the closing balance of 2013-14 will now be the opening balance for the FY 2014 – 15. You can watch out for this when ARBL provides its cash flow numbers for the year ended 31st March 2015.

At this point, let us run through a few interesting questions and answers:

- What does Rs.292.86 Crs actually state?

This literally shows how much cash ARBL has in its various bank accounts - What is cash?

Cash comprises cash on hand and demand deposits. Obviously, this is a liquid asset of the company - What are liquid assets?

Liquid assets are assets that can be easily converted to cash or cash equivalents - Are liquid assets similar to ‘current items’ that we looked at in the Balance sheet?

Yes, you can think of it that way - If cash is current and cash is an asset, shouldn’t it reflect under the current asset on the Balance sheet?

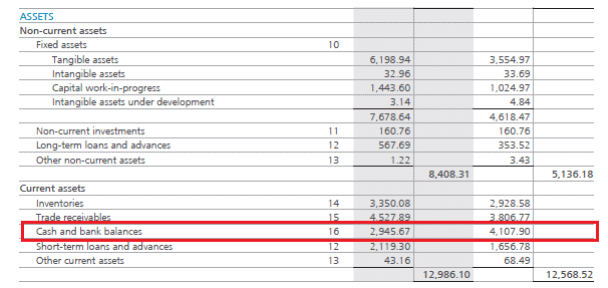

Exactly and here it is. Look at the balance sheet extract below.

Clearly, we can now infer that the cash flow statement and the balance sheet interact with each other. This is in line with what we had discussed earlier i.e all the three financial statements are interconnected with each other.

|

2 videos|51 docs|19 tests

|

FAQs on Statement of Cash Flows (Cash Flow Statement) - Financial Analysis and Reporting - Financial Analysis and Reporting - B Com

| 1. What is a Statement of Cash Flows (Cash Flow Statement)? |  |

| 2. What is the purpose of preparing a Statement of Cash Flows? | |

| 3. How is the Statement of Cash Flows different from other financial statements? | |

| 4. What are the three main sections of the Statement of Cash Flows? | |

| 5. What is the significance of the Statement of Cash Flows for investors and creditors? | |

|

4.69/5 Rating |

|

Dec 27, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

shortcuts and tricks

,Extra Questions

,practice quizzes

,Previous Year Questions with Solutions

,Sample Paper

,Objective type Questions

,video lectures

,Statement of Cash Flows (Cash Flow Statement) - Financial Analysis and Reporting | Financial Analysis and Reporting - B Com

,ppt

,mock tests for examination

,Statement of Cash Flows (Cash Flow Statement) - Financial Analysis and Reporting | Financial Analysis and Reporting - B Com

,past year papers

,Summary

,Free

,Important questions

,Semester Notes

,Exam

,study material

,Statement of Cash Flows (Cash Flow Statement) - Financial Analysis and Reporting | Financial Analysis and Reporting - B Com

,MCQs

,Viva Questions

;

Statement of Cash Flows (Cash Flow Statement) - Financial Analysis and Reporting Free PDF Download

Importance of Statement of Cash Flows (Cash Flow Statement) - Financial Analysis and Reporting

Statement of Cash Flows (Cash Flow Statement) - Financial Analysis and Reporting Notes

Statement of Cash Flows (Cash Flow Statement) - Financial Analysis and Reporting B Com Questions

Study Statement of Cash Flows (Cash Flow Statement) - Financial Analysis and Reporting on the App

|

© EduRev

|

Education Revolution

|

|