Structure of Commercial Banking System - Indian Banking System, Indian Financial System | Indian Financial System - B Com PDF Download

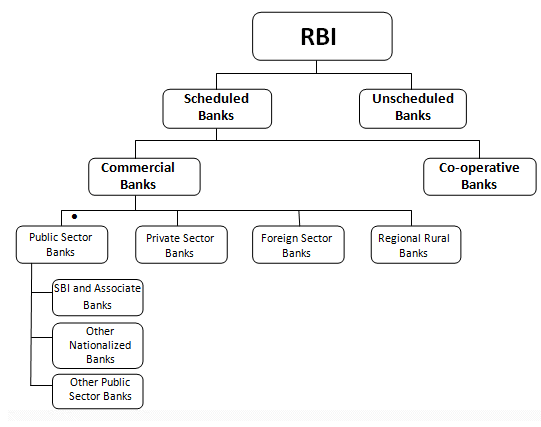

Reserve Bank of India (RBI)

The country had no central bank prior to the establishment of the RBI. The RBI is the supreme monetary and banking authority in the country and controls the banking system in India. It is called the Reserve Bank’ as it keeps the reserves of all commercial banks.

Scheduled & Non –scheduled Banks

A scheduled bank is a bank that is listed under the second schedule of the RBI Act, 1934. In order to be included under this schedule of the RBI Act, banks have to fulfill certain conditions such as having a paid up capital and reserves of at least 0.5 million and satisfying the Reserve Bank that its affairs are not being conducted in a manner prejudicial to the interests of its depositors. Scheduled banks are further classified into commercial and cooperative banks. Non- scheduled banks are those which are not included in the second schedule of the RBI Act, 1934. At present these are only three such banks in the country.

Commercial Banks

Commercial banks may be defined as, any banking organization that deals with the deposits and loans of business organizations.Commercial banks issue bank checks and drafts, as well as accept money on term deposits. Commercial banks also act as moneylenders, by way of installment loans and overdrafts.Commercial banks also allow for a variety of deposit accounts, such as checking, savings, and time deposit. These institutions are run to make a profit and owned by a group of individuals.

Scheduled Commercial Banks (SCBs):

Scheduled commercial banks (SCBs) account for a major proportion of the business of the scheduled banks. SCBs in India are categorized into the five groups based on their ownership and/or their nature of operations. State Bank of India and its six associates (excluding State Bank of Saurashtra, which has been merged with the SBI with effect from August 13, 2008) are recognised as a separate category of SCBs, because of the distinct statutes (SBI Act, 1955 and SBI Subsidiary Banks Act, 1959) that govern them. Nationalised banks and SBI and associates together form the public sector banks group IDBI ltd. has been included in the nationalised banks group since December 2004. Private sector banks include the old private sector banks and the new generation private sector banks- which were incorporated according to the revised guidelines issued by the RBI regarding the entry of private sector banks in 1993.

Foreign banks are present in the country either through complete branch/subsidiary route presence or through their representative offices.

Types of Scheduled Commercial Banks

Public Sector Banks

These are banks where majority stake is held by the Government of India.

Examples of public sector banks are: SBI, Bank of India, Canara Bank, etc.

Private Sector Banks

These are banks majority of share capital of the bank is held by private individuals. These banks are registered as companies with limited liability. Examples of private sector banks are: ICICI Bank, Axis bank, HDFC, etc.

Foreign Banks

These banks are registered and have their headquarters in a foreign country but operate their branches in our country. Examples of foreign banks in India are: HSBC, Citibank, Standard Chartered Bank, etc

Regional Rural Banks

Regional Rural Banks were established under the provisions of an Ordinance promulgated on the 26th September 1975 and the RRB Act, 1976 with an objective to ensure sufficient institutional credit for agriculture and other rural sectors. The area of operation of RRBs is limited to the area as notified by GoI covering one or more districts in the State.

RRBs are jointly owned by GoI, the concerned State Government and Sponsor Banks (27 scheduled commercial banks and one State Cooperative Bank); the issued capital of a RRB is shared by the owners in the proportion of 50%, 15% and 35% respectively.

Prathama bank is the first Regional Rural Bank in India located in the city Moradabad in Uttar Pradesh.

| Type of Commercial Banks | Major Shareholders | Major Players |

| Public Sector Banks | Government of India | SBI, PNB, Canara Bank, Bank of Baroda, Bank of India, etc |

| Private Sector Banks | Private Individuals | ICICI Bank, HDFC Bank, Axis Bank, Kotak Mahindra Bank, Yes Bank etc. |

| Foreign Banks | Foreign Entity | Standard Chartered Bank, Citi Bank, HSBC, Deutsche Bank, BNP Paribas, etc. |

| Regional Rural Banks | Central Govt, Concerned State Govt and Sponsor Bank in the ratio of 50 : 15 : 35 | Andhra Pradesh Grameena Vikas Bank, Uttranchal Gramin Bank, Prathama Bank, etc. |

Cooperative Banks

A co-operative bank is a financial entity which belongs to its members, who are at the same time the owners and the customers of their bank. Co-operative banks are often created by persons belonging to the same local or professional community or sharing a common interest. Co-operative banks generally provide their members with a wide range of banking and financial services (loans, deposits, banking accounts, etc).

They provide limited banking products and are specialists in agriculture-related products.

Cooperative banks are the primary financiers of agricultural activities, some small-scale industries and self-employed workers.

Co-operative banks function on the basis of “no-profit no-loss”.

Anyonya Co-operative Bank Limited (ACBL) is the first co-operative bank in India located in the city of Vadodara in Gujarat.

The co-operative banking structure in India is divided into following main 5 categories:

| 1. | Primary Urban Co-op Banks |

| 2. | Primary Agricultural Credit Societies |

| 3. | District Central Co-op Banks |

| 4. | State Co-operative Banks |

| 5. | Land Development Banks |

Difference between Scheduled Commercial and Schedule Co-operative Banks

The basic difference between scheduled commercial banks and scheduled cooperative banks is in their holding pattern. Scheduled cooperative banks are cooperative credit institutions that are registered under the Cooperative Societies Act. These banks work according to the cooperative principles of mutual assistance.Also,unlike commercial banks ,these banks work on the basis of “no-profit no-loss”.

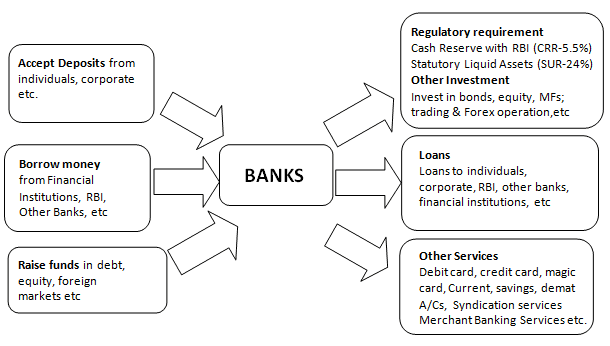

How Banks Function

Banks make money by lending your money out at interest and by charging you for services provided. Banks keep on lending money.

The other big revenue items generated by banks are the fees they charge. Bank charge for every service, whether it is for an electronic transaction, or permitting a transfer through the Internet banking system.

The banking industry in India is highly regulated. Few important regulations are mentioned below:

| Regulatory Requirements |

A bank has to set aside a certain percentage of total funds to meet regulatory requirements. The primary regulatory ratios are Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR). RBI uses both these instruments to regulate money supply in the economy. CRR is the percentage of net total of deposits a bank is required to maintain in form of cash with RBI. Currently this ratio is at 5.5%. This is used to control the liquidity in the economy. Higher the CRR, the lower is the amount that banks will be able to use for lending activities and vice versa. SLR is the minimum percentage of deposits that the bank has to maintain in form of gold, cash and/or other approved securities. Currently, the SLR is 24%. This is used to regulate the credit growth |

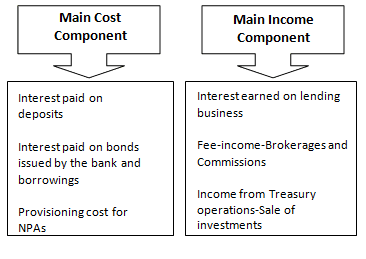

The core operating income of a bank is interest income (comprises 75-85% in the total income of almost all Indian Banks). Besides interest income, a bank also generates fee-based income in the form of commissions and exchange, income from treasury operations and other income from other banking activities. As banks were assigned a special role in the economic development of the country, RBI has stipulated that a portion of bank lending should be for the development of under-banked and under-privileged sections, which is called the priority sector. Current rules stipulate that domestic banks should lend 40% and the foreign banks should lend 32% of their net credit to the priority sector. On the cost sides, the major items for a bank are interest paid on different types of deposits, bonds issued and borrowings, and provisioning cost for Non-performing Assets (NPAs).

Types of Businesses of Banks

The banking business can be broadly categorized into Retail Banking, Wholesale or Corporate Banking, Treasury Operations and Other Banking Activities.

| Business Segmentation | |

| Retail Banking | Loans to individuals (Housing loan, Auto loan, Education loan and other personal loan) or small businesses. |

| Wholesale banking | Loans to mid and large corporate (Project Finance, Working Capital Loans, Terms Loans, Lease Finance, etc.) |

| Treasury Operations | Investment in bonds, equity, Mutual Funds, commodities, derivatives; trading and forex operations |

| Other Banking Activities | Hire purchase activities, leasing business, merchant banking, Syndication services, etc. |

Retail banking also known as Consumer Banking is the provision of services by a bank to individual consumers, rather than to companies, corporations or other banks. Services offered include savings and transactional accounts, mortgages, personal loans, debit cards, and credit cards. Retail banking segment is the highest margin business as compared to other business segments in the banking industry. Currently, ICICI Bank is the largest players in this segment in India. Other major players in this segment are SBI, PNB, HDFC Bank, etc.

Typical products offered by a retail bank include:

| 1. | Savings /Current accounts |

| 2. | Debit cards |

| 3. | ATM cards |

| 4. | Credit cards |

| 5. | Traveler’s cheques |

| 6. | Mortgages |

| 7. | Home equity loans |

| 8. | Personal loans |

| 9. | Certificates of deposit/Term deposits |

Wholesale banking is the provision of services by banks to organizations such as Mortgage Brokers, large corporate clients, mid-sized companies, real estate developers and investors, international trade finance businesses, institutional customer(such as pension funds and government entities/agencies), and services offered to other banks or other financial institutions.

Wholesale finance refers to financial services conducted between financial services companies and institutions such as banks, insurers, fund managers, and stockbrokers.

Modern wholesale banks engage in:

| 1. | Finance wholesaling |

| 2. | Underwriting |

| 3. | Market making |

| 4. | Consultancy |

| 5. | Mergers and acquisitions |

| 6. | Fund management |

Wholesale banking segment in India is largely dominated by large Indian banks – SBI, ICICI Banks, PNB, BoB, etc.

Treasury management (or treasury operations) includes management of an enterprise’s holdings, with the ultimate goal of managing the firm’s liquidity and mitigating its operational, financial and reputational risk. Treasury Management includes a firm’s collections, disbursements, concentration, investment and funding activities. In larger firms, it may also include trading in bonds, currencies, financial derivatives and the associated financial risk management. Most banks have whole departments devoted to treasury management and supporting their clients’ needs in this area

Bank Treasuries may have the following departments:

| 1. | A Fixed Income or Money Market desk that is devoted to buying and selling interest bearing securities |

| 2. | A Foreign exchange or “FX” desk that buys and sells currencies |

| 3. | A Capital Markets or Equities desk that deals in shares listed on the stock market. |

|

39 videos|39 docs|14 tests

|

FAQs on Structure of Commercial Banking System - Indian Banking System, Indian Financial System - Indian Financial System - B Com

| 1. What is the structure of the commercial banking system in India? |  |

| 2. What is the role of the Reserve Bank of India (RBI) in the Indian banking system? | |

| 3. What is the difference between public sector banks and private sector banks in India? | |

| 4. What are regional rural banks and co-operative banks in India? | |

| 5. What is the importance of the Indian banking system in the Indian financial system? | |

Exam

,Previous Year Questions with Solutions

,Important questions

,Structure of Commercial Banking System - Indian Banking System

,Structure of Commercial Banking System - Indian Banking System

,Objective type Questions

,Indian Financial System | Indian Financial System - B Com

,practice quizzes

,Sample Paper

,shortcuts and tricks

,past year papers

,ppt

,Indian Financial System | Indian Financial System - B Com

,Free

,video lectures

,Viva Questions

,Indian Financial System | Indian Financial System - B Com

,MCQs

,Extra Questions

,Semester Notes

,Structure of Commercial Banking System - Indian Banking System

,mock tests for examination

,Summary

,study material

;

Structure of Commercial Banking System - Indian Banking System, Indian Financial System Free PDF Download

Importance of Structure of Commercial Banking System - Indian Banking System, Indian Financial System

Structure of Commercial Banking System - Indian Banking System, Indian Financial System Notes

Structure of Commercial Banking System - Indian Banking System, Indian Financial System B Com Questions

Study Structure of Commercial Banking System - Indian Banking System, Indian Financial System on the App

|

© EduRev

|

Education Revolution

|

|