Trading - Principles of Accounting, Accountancy and Financial Management | Accountancy and Financial Management - B Com PDF Download

Definition and Explanation:

The account which is prepared to determine the gross profit or gross loss of a business concern is called trading account.

It should be noted that the result of the business determined through trading account is not true result. The true result is the net profit or the net loss which is determined through profit and loss account. The trading accounting has the following features:

- It is the first stage of final accounts of a trading concern.

- It is prepared on the last day of an accounting period.

- Only direct revenue and direct expenses are considered in it.

- Direct expenses are recorded on its debit side and direct revenue on its credit side.

- All items of direct expenses and direct revenue concerning current year are taken into account but no item relating to past or next year is considered in it.

- If its credit side exceeds it represents gross profit and if debit side exceeds it shows gross loss.

Purpose of Preparing Trading Account:

The profit or loss determined by a trading account is the gross result of the business but not the net result. If so, then a question arises - what is the use of preparing a trading account? This account is necessary because of the following advantages.

Gross profit of a business is very important data, since all business expenses are met out of it. So the amount of gross profit should be adequate to meet the indirect expenses of a business concern.

The amount of net sales can be determined through this account. Gross sales can be ascertained from sales account in the ledger, but net sales cannot be so obtained. The true sales of a business is net sales - not gross sales. Net sales are determined by deducting sales returns from gross sales in trading account.

The success or failure of a business can be ascertained by comparing net sales of the current year with that of the last year. It should be noted that an increase in the amount of net sales of the current year over the last year may not be regarded as a sign of success, since sales may increase because of rise in price level.

Percentage of gross profit on net sales (gross profit ratio) can be easily determined from trading account. This percentage is very important yardstick for measuring the success or failure of a business. Compared to last year, if the rate increases, it indicates success; on the other hand if the rate decreases, it is an indication of failure.

Percentage of different items of buying expenses (direct expenses) on gross profit can be easily determined and by comparing the percentage of the current year with that of the previous year the variations can be ascertained. An analysis of variances will disclose their cause which will help in controlling the amount of expenses.

Inventory or stock turnover ratio can be determined from trading account. The success or failure of a business can be measured by this rate. Higher rate indicates a favorable sign i.e. goods are sold soon after their purchase. On the other hand, low rate signifies deterioration, i.e. goods are sold long after their purchase.

Method of Preparation of Trading Account:

Trial balance is a list of all ledger accounts balances, so all the necessary information for preparation of a trading account is available from the trial balance. As gross profit or gross loss of a particular period is determined through trading account. So it's heading will be as follows:

XYZ co.

Trading Account for the year ended 31.12.2005

(if accounting period ends on 31.12.2005)

From the trial balance, the balance of opening stock account, purchases account, returns inwards account and of all direct expenses are transferred on the debit side of the trading account, and the balance of the sales account, returns outwards account, and closing stock account are transferred on the credit side of the trading account. If the credit side of the trading account exceeds the debit side, the result is "gross profit", and if debit side exceeds the credit side, the result is "gross loss". The format of a trading account is shown below:

Name of Business

Trading Account for the year ended .....

|

| Rs. |

|

| Rs. | |

Stock (Opening) |

|

| Sales | ----- |

| |

Purchases | ----- |

| Less returns | ----- | ----- | |

Less returns | ----- | ----- |

|

|

| |

|

|

| Stock (closing) |

| ----- | |

Carriage inward |

| ----- | Gross loss (Transferred to P&l A/C) |

| ----- | |

Wages |

| ----- |

|

|

| |

Insurance in transit |

| ----- |

|

|

| |

Custom duty |

| ----- |

|

|

| |

Clearing charges |

| ----- |

|

|

| |

Freight inward |

| ----- |

|

|

| |

Transportation inward |

| ----- |

|

|

| |

Excise duty on goods |

| ----- |

|

|

| |

Royalty |

| ----- |

|

|

| |

Dock charges |

| ----- |

|

|

| |

Coal, Coke, Gas, fuel |

| ----- |

|

|

| |

Motive power |

| ----- |

|

|

| |

Oil, water |

| ----- |

|

|

| |

Gross profit (Transferred to P&l A/C) |

| ----- |

|

|

| |

If credit side exceeds the debit side = Gross profit

If debit side exceeds the credit side = Gross loss

Example:

The following are some ledger balances taken out from the trial balance of XYZ company on 31st December 2005.

$ | $ | ||

Stock on 1.12005 | 60,000 | Returns outwards | 16,000 |

Purchases | 360,000 | Returns inwards | 30,000 |

Carriage inwards | 24,000 | Sales | 500,000 |

The closing stock is valued at $10,000.

Required:

Prepare a trading account for the year ended 31st December 2005. Show the journal entries to close the above account (closing entries).

Solution:

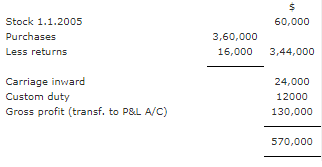

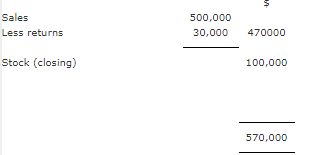

xyz co.

Trading Account for the year ended 31.12.2005

$ | $ | ||||

Stock 1.1.2005 | 60,000 | Sales | 500,000 | ||

Purchases | 3,60,000 | Less returns | 30,000 | 470000 | |

Less returns | 16,000 | 3,44,000 | |||

Stock (closing) | 100,000 | ||||

Carriage inward | 24,000 | ||||

Custom duty | 12000 | ||||

Gross profit (transf. to P&L A/C) | 130,000 | ||||

570,000 | 570,000 |

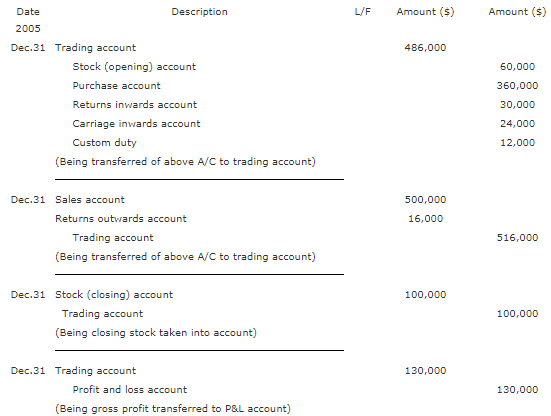

Closing Entries:

Date | Description | L/F | Amount ($) | Amount ($) |

2005 | ||||

Dec.31 | Trading account | 486,000 | ||

Stock (opening) account | 60,000 | |||

Purchase account | 360,000 | |||

Returns inwards account | 30,000 | |||

Carriage inwards account | 24,000 | |||

Custom duty | 12,000 | |||

(Being transferred of above A/C to trading account) | ||||

Dec.31 | Sales account | 500,000 | ||

Returns outwards account | 16,000 | |||

Trading account | 516,000 | |||

(Being transferred of above A/C to trading account) | ||||

Dec.31 | Stock (closing) account | 100,000 | ||

Trading account | 100,000 | |||

(Being closing stock taken into account) | ||||

Dec.31 | Trading account | 130,000 | ||

Profit and loss account | 130,000 | |||

(Being gross profit transferred to P&L account) |

Example:

The following are some ledger balances taken out from the trial balance of XYZ company on 31st December 2005.

The closing stock is valued at $10,000.

Required:

Prepare a trading account for the year ended 31st December 2005. Show the journal entries to close the above account (closing entries).

Solution:

xyz co.

Trading Account for the year ended 31.12.2005

Closing Entries:

Advantages of Preparing Trading Account Format

- It is a very important statement from the cost point of view of the goods. By preparing the Trading account entities can take the decision for continuing or discontinuing a particular product. It helps to earn the maximum profit or reduce the losses.

- With the help of a trading account, Sales tax authorities can easily see the correct purchases and correct sales as per the sales tax return submitted by a business firm.

- It also helps the Excise authorities to assess the excise duties of business firms.

- The management decides the price of the product with the help of a trading account, after keeping in mind the market competition.

Items in Trading Account Format

Trading Account contains the following details

- Opening stock details of raw material, semi-finished goods and finished goods.

- Closing stock details of raw material, semi-finished goods, and finished goods.

- Total purchases of goods fewer Purchase Returns.

- Total sales of goods fewer Sales Returns.

- All direct expenses related to purchases or sales or manufacturing of goods.

|

44 videos|75 docs|18 tests

|

FAQs on Trading - Principles of Accounting, Accountancy and Financial Management - Accountancy and Financial Management - B Com

| 1. What are the basic principles of accounting? |  |

| 2. What is the difference between accountancy and financial management? | |

| 3. What is the role of a B.Com graduate in trading? | |

| 4. How does trading impact the financial statements of a company? | |

| 5. What are the key skills required for a successful career in trading? | |

|

1.2K Views |

|

4.73/5 Rating |

|

Dec 23, 2024 Last updated |

|

44 videos|75 docs|18 tests

|

|

Explore Courses for B Com exam

|

|

mock tests for examination

,study material

,past year papers

,MCQs

,Objective type Questions

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Previous Year Questions with Solutions

,Trading - Principles of Accounting

,Sample Paper

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Trading - Principles of Accounting

,Summary

,Viva Questions

,shortcuts and tricks

,practice quizzes

,Extra Questions

,Trading - Principles of Accounting

,video lectures

,ppt

,Semester Notes

,Free

,Exam

,Important questions

;

Trading - Principles of Accounting, Accountancy and Financial Management Free PDF Download

Importance of Trading - Principles of Accounting, Accountancy and Financial Management

Trading - Principles of Accounting, Accountancy and Financial Management Notes

Trading - Principles of Accounting, Accountancy and Financial Management B Com Questions

Study Trading - Principles of Accounting, Accountancy and Financial Management on the App

|

© EduRev

|

Education Revolution

|

|