Trial Balance and Errors (Part - 1) - Commerce PDF Download

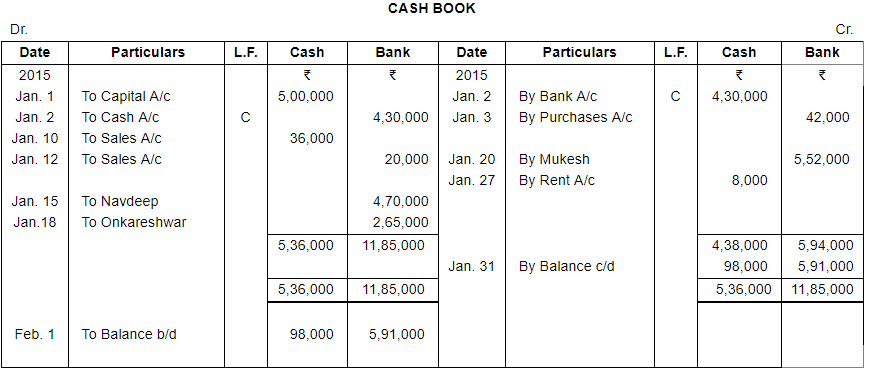

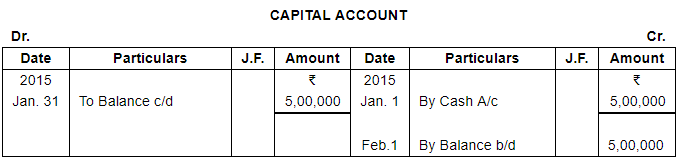

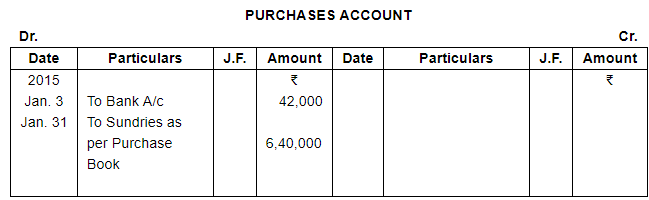

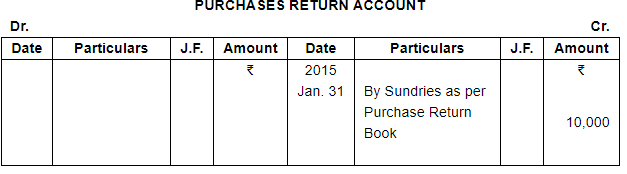

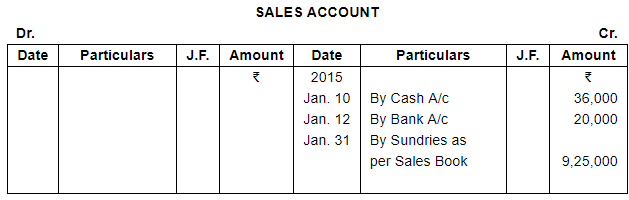

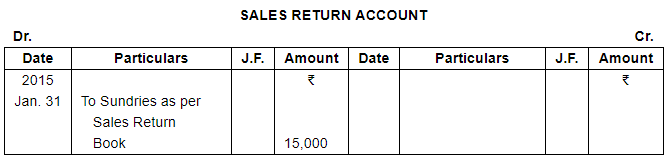

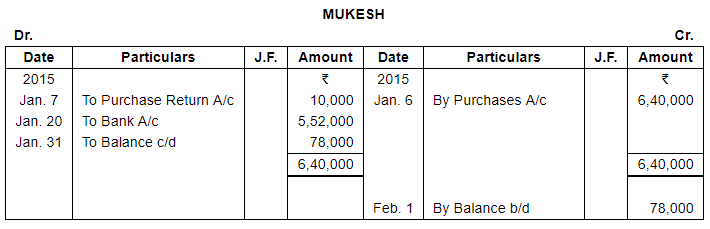

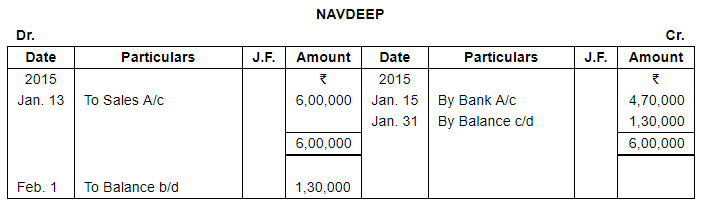

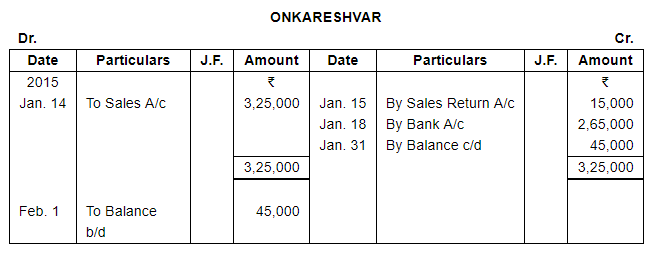

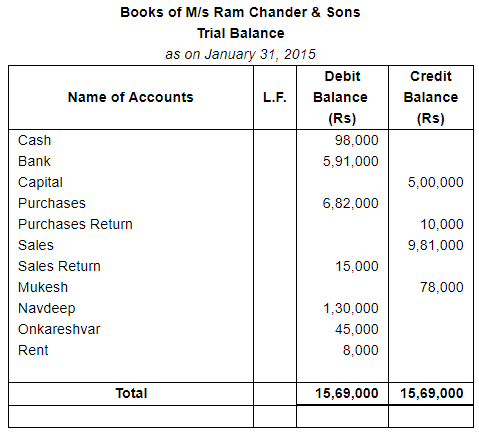

Page No 14.25:

Question 1:

Given below is a Cash Book and Ledger extracts relating to the books of M/s Ram Chander & Sons as at 31st January 2015. You are required to prepare a Trial Balance.

ANSWER:

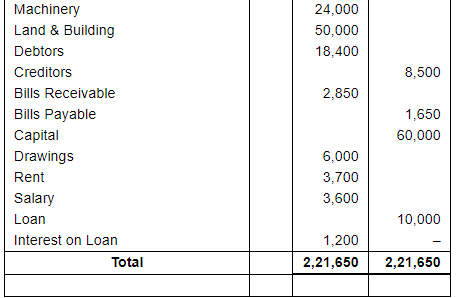

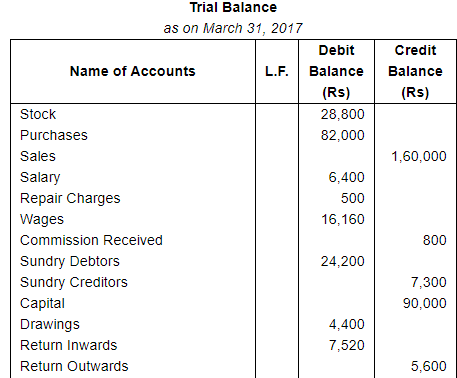

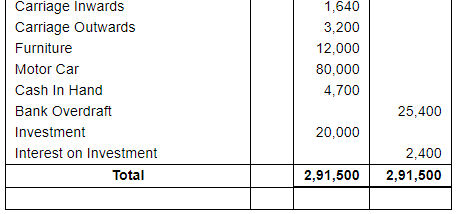

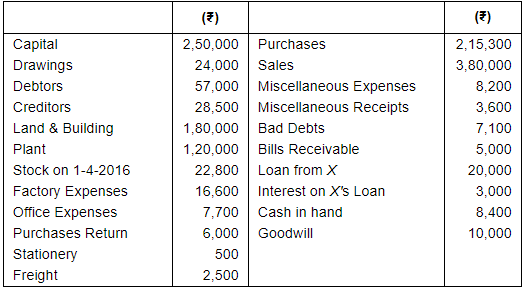

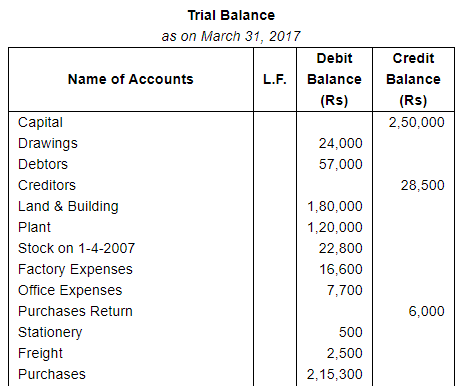

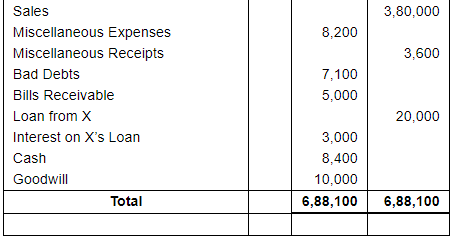

Page No 14.27:

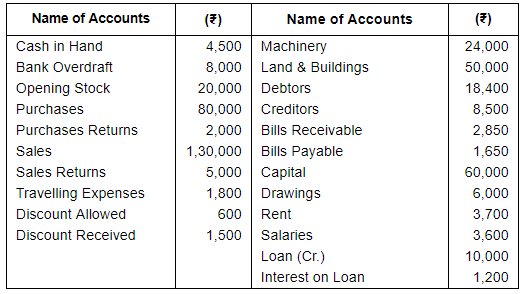

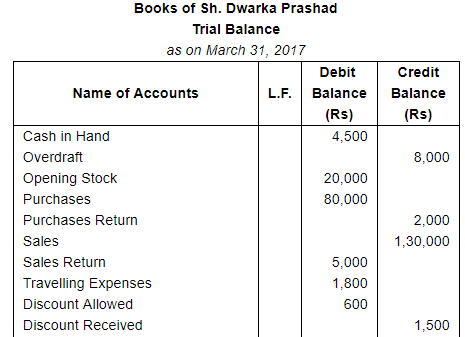

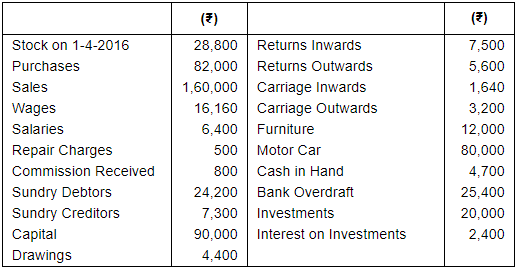

Question 2:

From the following balances, taken from the books of M/s Dwarka Parshad & Sons as at 31st March 2017, prepare a Trial Balance in proper form:−

ANSWER:

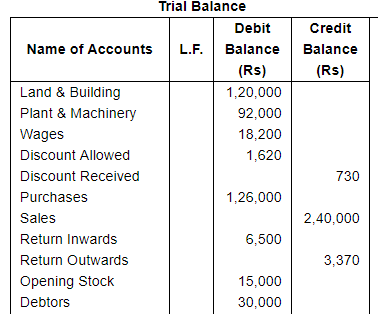

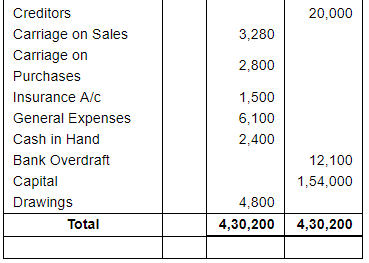

Page No 14.27:

Question 3(A):

Prepare a Trial Balance from the following balances as at 31st March 2017:−

Page No 14.28:

Question 3(B):

Prepare a Trial Balance from the following balances taken as at 31st March 2017:−

ANSWER:

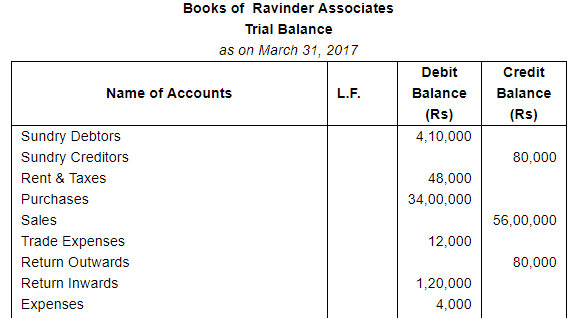

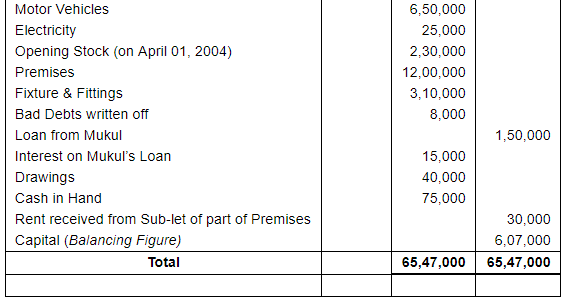

Page No 14.28:

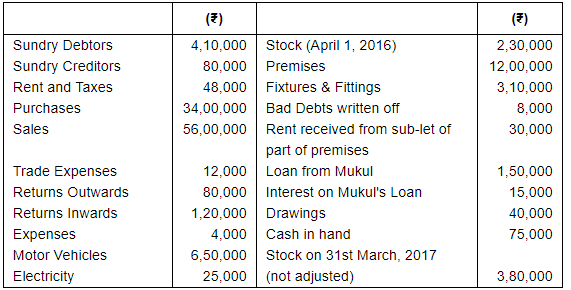

Question 4:

Following balances were extracted from the books of Ravinder Associates as at 31st March, 2017:

You are required to prepare the trial balance treating the difference as his capital.

ANSWER:

Note: Closing Stock of Rs 3,80,000 will not appear in Trial Balance, because it has not been accounted yet.

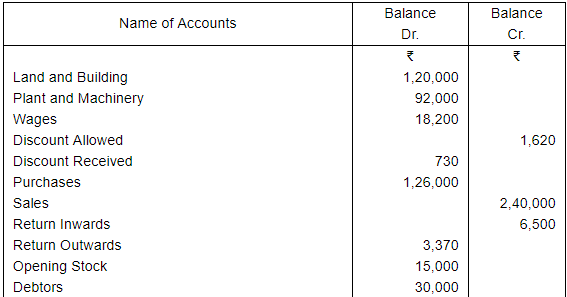

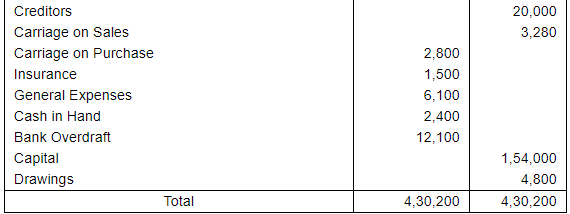

Page No 14.28:

Question 5:

The following trial balance has been prepared by an inexperienced accountant. Redraft it in a correct form:−

ANSWER:

FAQs on Trial Balance and Errors (Part - 1) - Commerce

| 1. What is a trial balance and why is it important in commerce? |  |

| 2. What are the common types of errors that can be identified through a trial balance? | |

| 3. How can errors be rectified after they are identified in a trial balance? | |

| 4. Can a trial balance guarantee that there are no errors in the accounting records? | |

| 5. How often should a trial balance be prepared in commerce? | |

|

2.9K Views |

|

4.76/5 Rating |

|

Dec 26, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

Objective type Questions

,Important questions

,video lectures

,Exam

,Trial Balance and Errors (Part - 1) - Commerce

,Trial Balance and Errors (Part - 1) - Commerce

,ppt

,Previous Year Questions with Solutions

,study material

,MCQs

,Viva Questions

,Extra Questions

,Sample Paper

,Free

,shortcuts and tricks

,mock tests for examination

,past year papers

,Semester Notes

,Trial Balance and Errors (Part - 1) - Commerce

,practice quizzes

,Summary

;

Trial Balance and Errors (Part - 1) Free PDF Download

Importance of Trial Balance and Errors (Part - 1)

Trial Balance and Errors (Part - 1) Notes

Trial Balance and Errors (Part - 1) Commerce Questions

Study Trial Balance and Errors (Part - 1) on the App

|

© EduRev

|

Education Revolution

|

|