Trial Balance and Errors (Part - 1) - Commerce PDF Download

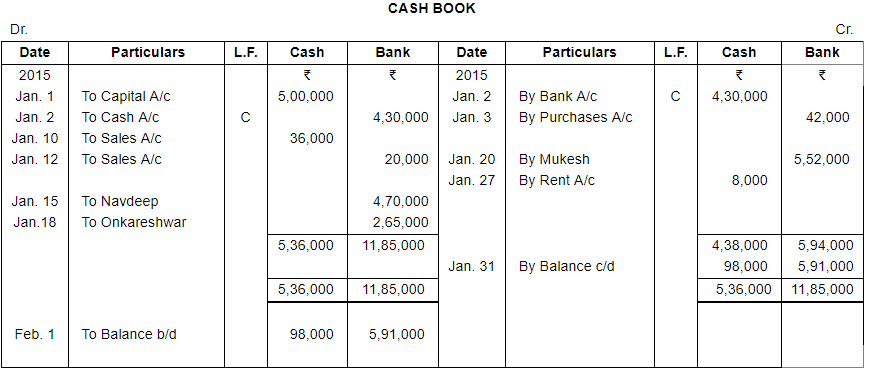

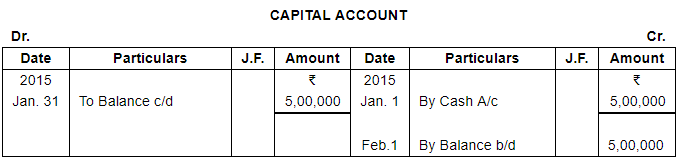

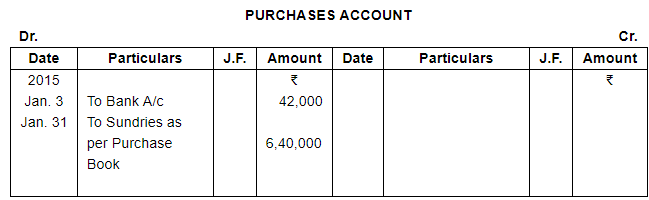

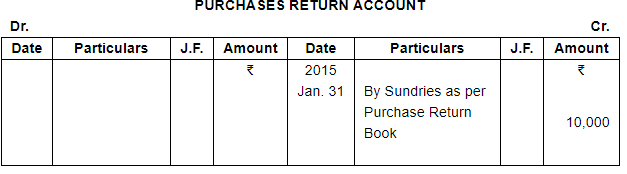

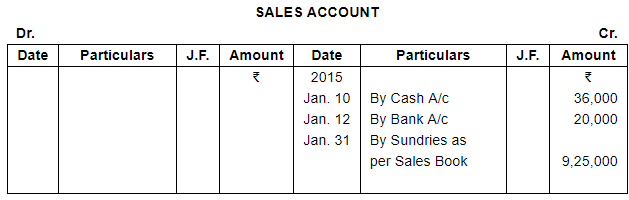

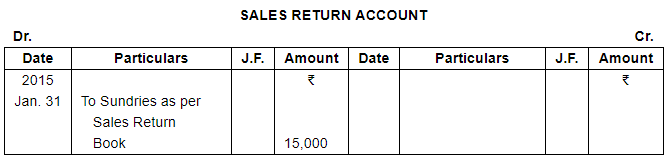

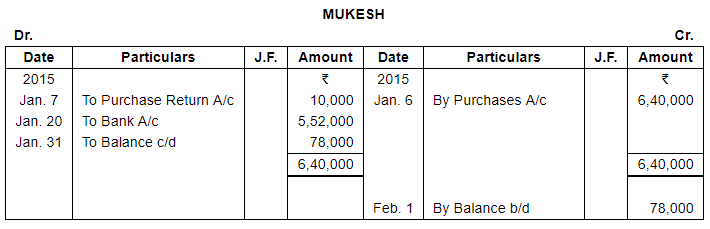

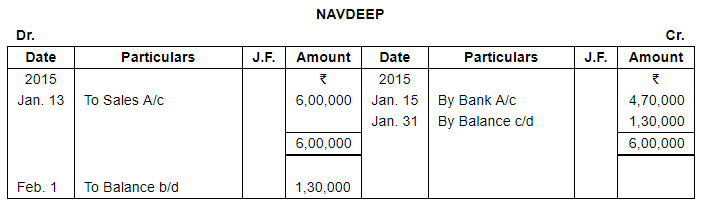

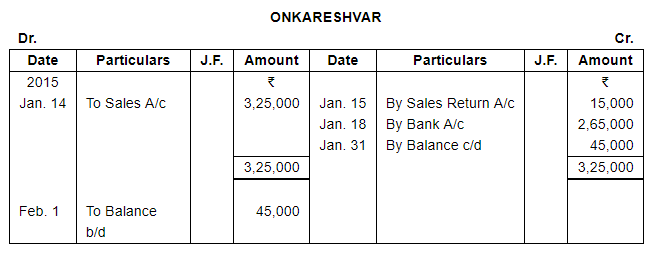

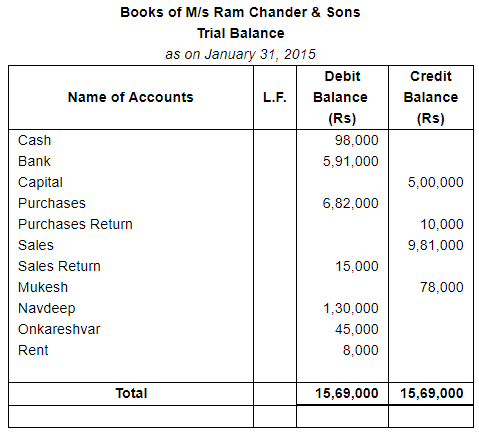

Page No 14.25:

Question 1:

Given below is a Cash Book and Ledger extracts relating to the books of M/s Ram Chander & Sons as at 31st January 2015. You are required to prepare a Trial Balance.

ANSWER:

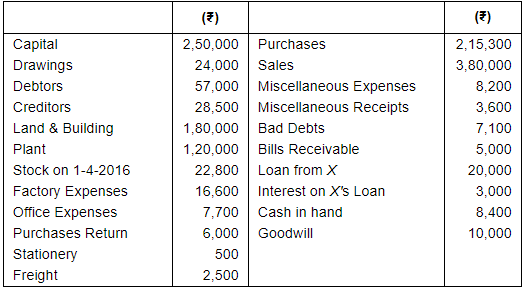

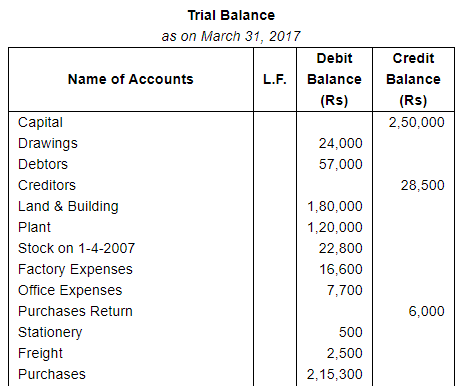

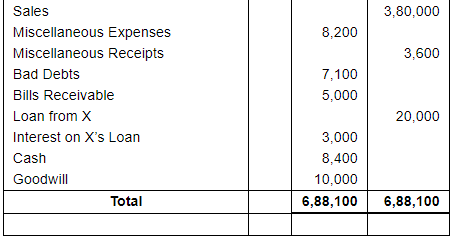

Page No 14.27:

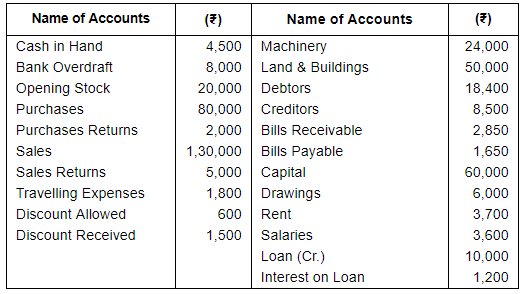

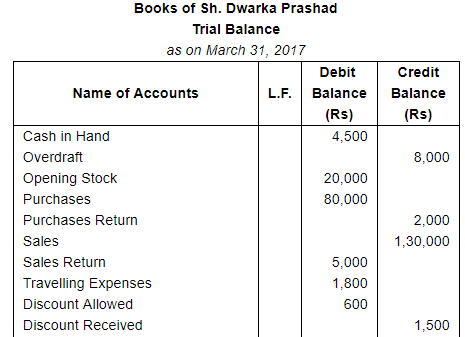

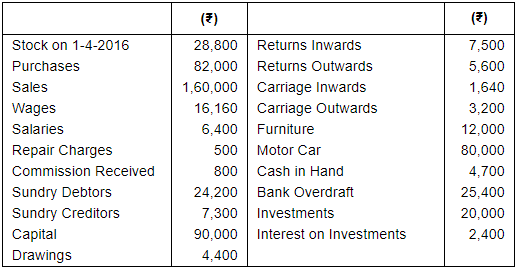

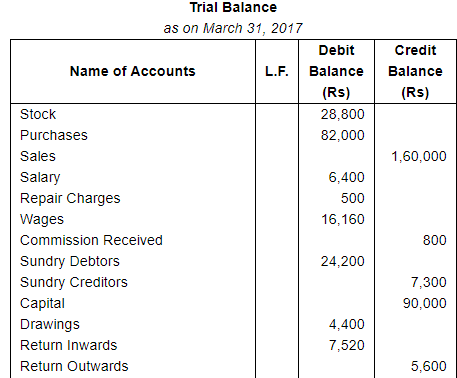

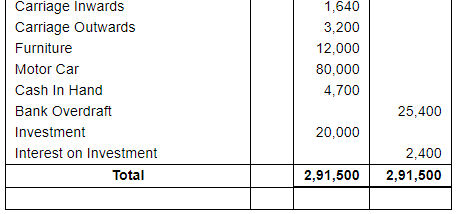

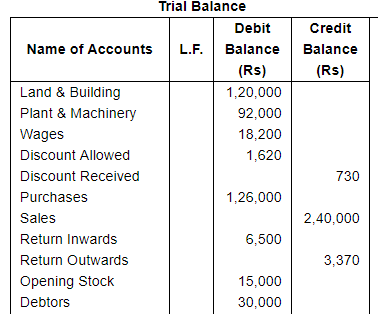

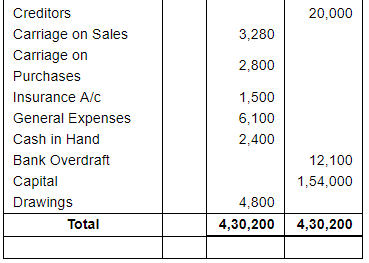

Question 2:

From the following balances, taken from the books of M/s Dwarka Parshad & Sons as at 31st March 2017, prepare a Trial Balance in proper form:−

ANSWER:

Page No 14.27:

Question 3(A):

Prepare a Trial Balance from the following balances as at 31st March 2017:−

Page No 14.28:

Question 3(B):

Prepare a Trial Balance from the following balances taken as at 31st March 2017:−

ANSWER:

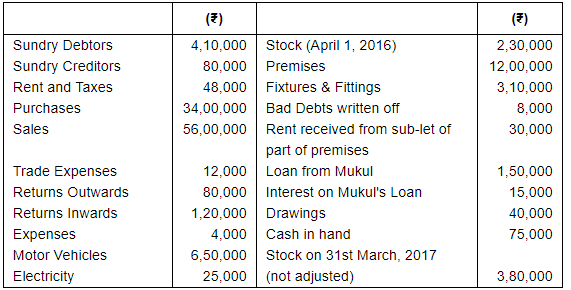

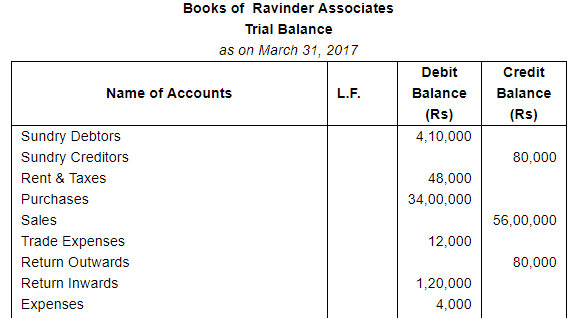

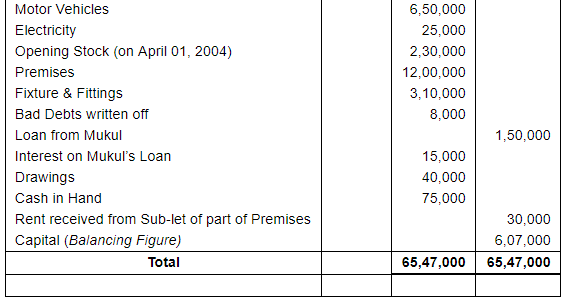

Page No 14.28:

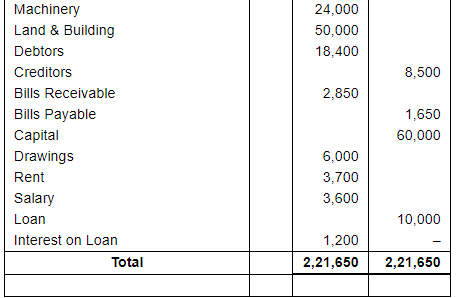

Question 4:

Following balances were extracted from the books of Ravinder Associates as at 31st March, 2017:

You are required to prepare the trial balance treating the difference as his capital.

ANSWER:

Note: Closing Stock of Rs 3,80,000 will not appear in Trial Balance, because it has not been accounted yet.

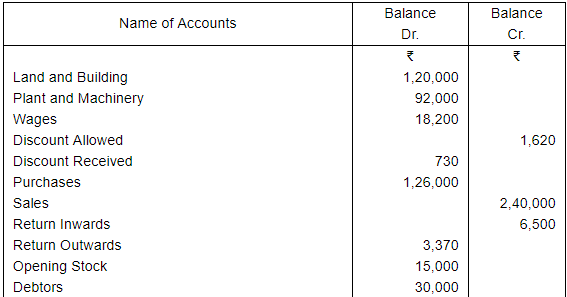

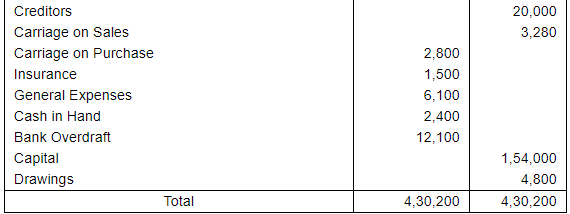

Page No 14.28:

Question 5:

The following trial balance has been prepared by an inexperienced accountant. Redraft it in a correct form:−

ANSWER:

FAQs on Trial Balance and Errors (Part - 1) - Commerce

| 1. What is a trial balance and why is it important in commerce? |  |

| 2. What are the common types of errors that can be identified through a trial balance? | |

| 3. How can errors be rectified after they are identified in a trial balance? | |

| 4. Can a trial balance guarantee that there are no errors in the accounting records? | |

| 5. How often should a trial balance be prepared in commerce? | |

|

2.9K Views |

|

4.71/5 Rating |

|

Dec 25, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

MCQs

,Objective type Questions

,ppt

,Semester Notes

,Free

,Sample Paper

,Summary

,Trial Balance and Errors (Part - 1) - Commerce

,Trial Balance and Errors (Part - 1) - Commerce

,Important questions

,study material

,Exam

,video lectures

,Viva Questions

,mock tests for examination

,Previous Year Questions with Solutions

,Extra Questions

,shortcuts and tricks

,Trial Balance and Errors (Part - 1) - Commerce

,past year papers

,practice quizzes

;

Trial Balance and Errors (Part - 1) Free PDF Download

Importance of Trial Balance and Errors (Part - 1)

Trial Balance and Errors (Part - 1) Notes

Trial Balance and Errors (Part - 1) Commerce Questions

Study Trial Balance and Errors (Part - 1) on the App

|

© EduRev

|

Education Revolution

|

|