Meaning & Objectives of Accounting - Commerce PDF Download

Meaning & objectives of Accounting

Meaning of accounting:

‘Accounting is the art of recording, classifying, and summarizing in a significant manner and in terms of money, transactions and events which are, in part at least, of financial character, and interpreting the results thereof'.

Characteristics/ Features & Attributes of Accounting:

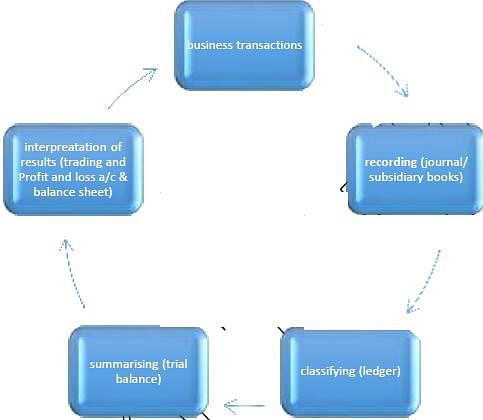

1. Accounting is an art as well as science:

- ART is the technique of attaining some predetermined objectives and Accounting is the art of recording, classifying, and summarizing the business transactions for the purpose of finding the profit & loss of the business.

- Science is a specified body of knowledge that is based on certain principles and accounting is a science as it is also based on accounting standards and principles.

2. Identifying and measuring the financial transactions only:

- Only those transaction will be recorded which re of a financial character (can be expressed in terms of money)

- There are a number of transactions in business but are recorded only when they can be expressed in terms of money

- Ex: a quarrel between production and sales manager, a strike by employees etc will not be recorded

- Value of 4 tables and 5 chairs will be recorded instead of their number 4 tables= Rs.4000 and tables=Rs.500.

3. Recording:

- Accounting is the art of recording the financial transactions in the books of original entry.

- For a small business where transactions are less journal is prepared

- When the business grows it prepares separate books for original entry which is called subsidiary books like cash book (records all cash receipts and payments), purchase book (records all credit purchases), sales book (for all credit sales), purchase return book, sales return the book, bills receivable and bills payables book also.

4. Classifying:

- Grouping similar nature of items at one place under their respective accounts is called classifying which is done in the ledger

- A separate account is prepared for every person, assets, liabilities, expenses and incomes on basis of all transactions.

- Like salary account, wages account and Ram’s account etc.

5. Summarizing:

- It is the art of presenting the classified data in a manner which is understandable to the internal and external users.

- This involves balancing the books of accounts and preparation of trial balances on the basis of it.

- Trial balance is a statement which is prepared with the debit and credit balances of the ledger to check the arithmetical accuracy of books of accounts.

6. Interpretation of results :

- On the basis of trial balance financial statements namely Trading and Profit & loss account for finding the profit and loss and balance sheet to ascertain the financial position of the business are prepared.

- The purpose is to present the results of the business in such a manner that all the interested parties should have full information about the profitability and financial position of the business.

7. Communicating:

- Finally, the results (financial statements) of the business are communicated to the users to help them in decision making.

Objectives of accounting

1. To keep a systematic record of all the business transactions:

- The main objective of the business is to record all the transactions in a chronological (day to day) manner on the principle of a double-entry system.

2. To calculate profit and loss:

- Another objective of the business is to determine the financial performance of the business(find profit and loss)

3. To know the exact reasons behind those profits and loss

4. To ascertain the progress of the business year after year.

5. To prevent error and frauds.

6. To provide information to various parties

- Another objective is to communicate the accounting information to various parties like owners, creditors, banks.

7. To ascertain the financial position of the business:

- Financial position is known from the balance sheet(shows the position of assets and liabilities)

Difference between Book keeping & Accounting | |||

S.NO | POINTS OF DIFFERENCE | BOOKKEEPING | ACCOUNTING |

1. | Scope | Book keeping involves: | Accounting involves: |

2. | Stage | Primary | Secondary |

3. | Objective | To keep is a systematic record of all transactions | To find net results(p & l) of business |

4. | Nature of job | Routine | Analytical |

5. | Who performs | Junior staff | Senior staff |

6. | Knowledge level | Limited level of knowledge | Higher level of knowledge |

Difference between accounting and accountancy | |||

S.NO | POINTS OF DIFFERENCE | ACCOUNTING | ACCOUNTANCY |

1. | Meaning | Concerned with recording, classifying and summarizing of transactions. | Concerned with the rules of recording, classifying and summarizing transactions. |

2. | Scope | Narrow | Wider |

3. | Relation | Depends on book keeping. | Depends on book keeping and accounting. |

4. | Function | To find net results (p & l) and the financial position (B/S) of the business. | Decision-making function. |

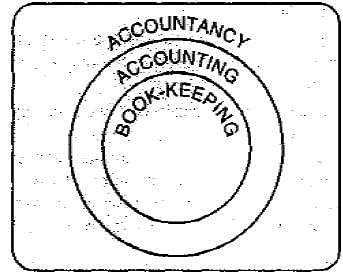

RELATIONSHIP BETWEEN ACCOUNTANCY, ACCOUNTING AND BOOK-KEEPING

Book-keeping is a part of Accounting. Accounting is a part of Accountancy. Diagrammatically, the relationship can be viewed as follows:

Types/branches of accounting:

1. Financial accounting:

- To find net results (p & l) and the financial position (B/S) of business

- To provide information to the various parties.

2. Cost accounting :

- To ascertain the total cost and per-unit cost of the product.

- To control the cost.

3. Tax accounting:

- Used for assessing the liability for tax(income tax, sales tax)

4. Management accounting:

- Present the information in such a way that is understandable to the management

- Helps in decision making.

5. Social responsibility accounting:

- Works on the reports on activities of the business towards the society(ITC)

- Techniques are used for measuring the contribution and benefits of the business towards society.

S.NO. | USERS/ INTERNAL | NEED FOR INFORMATION |

1. | Owners(present investors) | · Profitability of the business. |

2. | Management | · Decision making |

External users | ||

3. | Potential investors | How safe and rewarding will be the investment/ safety |

4. | Creditors | · Credit worthiness of the business/ financial position/ Profitability of the business |

5. | Lender/banks | Repaying capacity (Profitability of the business) |

6. | Employees | Salary and bonus (Profitability of the business) |

7. | Government | Assessment of tax liability (Profitability of the business) |

8. | Researchers | Research work/accounting theory |

9. | Public | Employment opportunities |

Advantages /Uses of accounting

1. Provide a complete and systematic record of all transactions:

- Based on a double-entry system.

* chronological order

- Helpful in management of the business: they need a lot of information about many things which the accounting provides.

- Helpful in planning

- Helpful in decision making

- Helpful in controlling

2. Information regarding profit and loss:

- Determine the financial performance of the business(find true profit and loss)

- Great use for the parties who are interested in accounting.

3. Enables a comparative study:

- Comparison between previous year and current year performance in terms of profits, sales, expenses and costs etc.

- Provide information for comparison with competitors.

4. Helpful in assessing the tax liability: income tax and sales tax

5. Evidence in legal matters: supported by source documents

6. Helpful in the detection of errors and frauds

7. Helpful in raising loans: banks demands financial statements and cash flows before granting loans.

Limitations of accounting

1. Based on concepts and conventions:

- Accounts are prepared on a number of accounting concepts and conventions.

- Ex: fixed assets are always shown at their cost and not at their market value as per the historic cost concept.

2. Incomplete information:

- It provides incomplete information about profit and loss as the actual profit and loss can be known when the business is closed down.

3. Omission of qualitative information:

- As accounting records, only those transactions which are monetary in nature t ignores the qualitative information like quality of staff, industrial relations, public relations.

4. Affected by window dressing:

- Manipulation in the books of account in financial statements to show a better position of the business.

- Ex: closing stock may be overvalued; credit purchases at the end of the year are ignored.

5. Influenced by personal judgments :

- In many situations, the accountant has to make a choice or of various alternatives.

- Ex: choice of method of depreciation- straight line, diminishing balance or for stock – LIFO or FIFO

6. Ignores the price level changes:

- As the accounts are prepared on the historical cost concept it ignores such changes.

- Money as a measurement unit changes its value, it is not stable but we still record the assets at their cost.

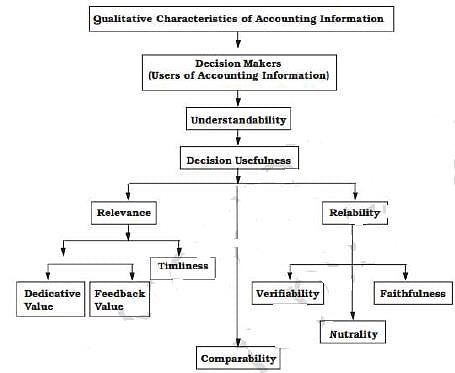

Qualitative characteristics of accounting:

1. Reliability :

- All the accounting information must be reliable it means verifiable, free from biasness and errors.

- Can be verified from the source document, which brings truth fullness to the results.

2. Relevance

- All the accounting information must be relevant for the users to help in decision making.

- Ex: rate of a dividend of the firm in the previous year will affect the shareholders decision making.

3. Understandability:

- All the accounting information must be presented in a manner in which users can also understand it.

- All the general topics can be shown in the foot notes like a method of depreciation or inventory valuation.

4. Comparability

- Comparison between previous year and current year performance in terms of profits, sales, expenses and costs etc.

- Provide information for comparison with competitors.

- Understand the topic by going through this Crash Course of Accountancy - Class 11

- Test your knowledge by attempting this test of Meaning and Scope of Accounting.

FAQs on Meaning & Objectives of Accounting - Commerce

| 1. What is the meaning of accounting in commerce? |  |

| 2. What are the objectives of accounting? | |

| 3. What are the different branches of accounting? | |

| 4. What are the benefits of studying accounting in commerce? | |

| 5. What is the role of accounting in business decision-making? | |

|

31.1K Views |

|

4.97/5 Rating |

|

Dec 25, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

Meaning & Objectives of Accounting - Commerce

,Meaning & Objectives of Accounting - Commerce

,Summary

,Viva Questions

,Extra Questions

,ppt

,mock tests for examination

,practice quizzes

,video lectures

,Previous Year Questions with Solutions

,Meaning & Objectives of Accounting - Commerce

,MCQs

,Free

,past year papers

,study material

,Exam

,shortcuts and tricks

,Objective type Questions

,Semester Notes

,Sample Paper

,Important questions

;

Meaning & Objectives of Accounting Free PDF Download

Importance of Meaning & Objectives of Accounting

Meaning & Objectives of Accounting Notes

Meaning & Objectives of Accounting Commerce Questions

Study Meaning & Objectives of Accounting on the App

|

© EduRev

|

Education Revolution

|

|