Chapter Notes: Depreciation, Provisions and Reserves

Introduction

- The matching principle requires that revenues of a period be matched with the expenses incurred to earn those revenues in the same period.

- This principle ensures correct measurement of profit or loss for the accounting period.

- Costs that provide benefit over more than one accounting period must be allocated across the periods they benefit rather than charged entirely in the year of acquisition.

- Depreciation on fixed assets is a primary example of such allocation of cost.

- Where the exact amount of an expense is uncertain, the principle of conservatism (prudence) requires making suitable provisions and charging them in the current period.

- A portion of profit may be retained in the business as reserves to support future growth, contingencies or specific purposes.

Depreciation

- Depreciation denotes the decline in value of fixed assets due to usage, passage of time or obsolescence.

- Fixed assets (also called depreciable assets) are assets used in the business for more than one accounting year; their recorded value is reduced to recognise expired cost.

- Depreciation is an expense charged to the Statement of Profit and Loss because it is an expired portion of the asset's cost for the period.

- Example: A machine bought for ₹1,00,000 with an estimated useful life of 10 years will not have its full cost charged in the first year. Instead, ₹10,000 may be charged each year (assuming straight-line), representing that year's expired cost.

Meaning of Depreciation

- Depreciation is the gradual and permanent decrease in the book value of fixed assets over time.

- It is based on the cost of assets used in business, not current market value.

- According to the Institute of Cost and Management Accounting, depreciation is the reduction in intrinsic value of an asset due to use and/or passage of time.

- Accounting Standard (AS) 6 (Revised) defines depreciation as the allocation of the depreciable amount of an asset over its expected useful life. It includes amortisation of intangible assets with predetermined useful life.

- Depreciation is allocated so that a fair portion of the depreciable amount is charged to each accounting period during the asset's expected useful life.

AS-6 (Revised): Depreciation (Summary)

- Depreciation measures reduction in value of a depreciable asset caused by use, passage of time, or obsolescence due to technological or market changes.

- It is allocated to charge a fair proportion of the depreciable amount to each accounting period during the asset's expected useful life.

- The base for depreciation is depreciable assets - assets expected to be used for more than one accounting period, held for production, supply, rental or administrative use rather than for sale in the ordinary course of business.

- The amount of depreciation depends on three factors: Cost, Useful life, and Net realizable (salvage) value.

- Once a depreciation method is selected, it should be applied consistently; changes are permitted only under specified circumstances.

Depreciable assets are those that:

- are expected to be used for more than one accounting period,

- have a limited useful life, and

- are held for production, supply, rental or administrative purposes (not for sale in ordinary course).

Examples: machines, plants, furniture, buildings, computers, trucks and equipment.

- Depreciation is charged on the depreciable amount - historical cost (or substituted amount) less estimated salvage value.

- Expected useful life is the period over which an asset is expected to be used or the number of similar units expected to be produced using the asset.

Features of Depreciation

- Decline in Book Value: Depreciation reduces the carrying (book) value of fixed assets over time.

- Causes of Value Loss: Loss due to time, usage and obsolescence; for example, a machine becomes less valuable when a newer model appears.

- Continuing Process: Depreciation is an ongoing process occurring throughout an asset's useful life.

- Expired Cost: Depreciation is an expense and must be deducted before calculating taxable profits.

- Depreciation is a non-cash expense; it does not involve cash outflow but writes off past capital expenditure.

Depreciation and Similar Terms

Depletion and Amortisation

- Depletion relates to reduction in quantity of natural resources (minerals, oil) due to extraction; treated similarly to depreciation for accounting purposes.

- Amortisation is the systematic write-off of the cost of intangible assets (patents, copyrights, goodwill) over their useful life; similar in concept to depreciation.

Causes of Depreciation

- Wear and Tear due to Use: Physical deterioration resulting from usage in business operations.

- Wear and Tear due to Passage of Time: Assets may deteriorate over time even when not in use (e.g., exposure to elements).

- Expiration of Legal Rights: Patents, copyrights and leases lose value when legal protection or contractual rights expire.

- Obsolescence: Technological improvements, changes in market demand or production methods can make an asset outdated.

- Abnormal Factors: Accidents, fire, earthquake, flood can cause sudden irreversible reduction in asset usefulness; such losses are permanent but not gradual.

Need for Depreciation

- Matching of Costs and Revenue: As fixed assets generate revenue over multiple periods, depreciation allocates asset cost to those periods for correct profit measurement.

- Tax Consideration: Depreciation is an allowable deduction for tax purposes, though tax rules may differ from accounting practice.

- True and Fair Financial Position: Without depreciation assets would be overstated and balance sheet would not present a true position.

- Compliance with Law and Standards: Accounting standards and some laws require provision for depreciation.

Factors Affecting Amount of Depreciation

The amount of depreciation depends on three main parameters: cost, estimated useful life, and probable salvage value.

Cost of Asset

- The cost includes invoice price plus necessary expenditures to bring the asset to working condition - freight, transit insurance, installation, registration and commissions.

- For second-hand assets, initial repairs to make them usable are part of cost.

- AS-6 states cost includes acquisition, installation, commissioning and any improvements or additions.

- Example: Photocopy machine bought for ₹50,000 with ₹5,000 transportation and installation costs will have an original cost of ₹55,000 to be depreciated.

Estimated Net Residual (Salvage) Value

- Net residual value (scrap or salvage value) is estimated realizable value at end of useful life after disposal costs.

- Example: Machine expected sale value ₹6,000 less disposal expenses ₹1,000 gives net residual value ₹5,000.

Depreciable Cost

- Depreciable cost = Cost of asset - Net residual value.

- Example: Cost ₹50,000, net residual value ₹5,000 → depreciable cost ₹45,000.

- The total depreciation charged over the asset's life should equal the depreciable cost. Under-recovery violates matching principle.

Estimated Useful Life

- Useful life is the estimated economic or commercial lifespan, not necessarily physical life.

- An asset may remain physically usable but economically unviable; useful life depends on usage, maintenance, technology and market changes.

- AS-6: useful life is the period expected to be used by the enterprise; it may be expressed in years, units of output or working hours.

- Factors influencing useful life include legal limits, number of shifts, repair and maintenance practice, technological obsolescence, innovations, and legal or other restrictions.

Methods of Calculating Depreciation

- The depreciable amount and the method of allocation determine the annual depreciation charge.

- Two principal methods commonly used and recognised in India are:

- Straight Line Method (SLM)

- Written Down Value Method (WDV)

- Other methods include:

- Annuity Method

- Depreciation Fund Method

- Insurance Policy Method

- Sum of Years' Digits Method

- Double Declining Balance Method

- Selection of method depends on type of asset, nature of use and business circumstances.

Straight Line Method (SLM)

- Assumes equal usage of the asset across its useful life; depreciation charged is constant each year.

- Also called the fixed instalment method or fixed percentage on original cost method.

- Annual depreciation reduces the asset's cost to its scrap value by the end of useful life.

- Formula for annual depreciation (SLM): Depreciation = (Cost - Salvage value) / Useful life.

Example illustration: Asset cost ₹2,50,000; useful life 10 years; residual value ₹50,000. Annual depreciation is computed to be ₹20,000.

Advantages of SLM

- Simple and easy to understand.

- Distributes full depreciable cost over useful life to scrap value or zero.

- Provides consistent annual depreciation charges - useful for comparison of profits across years.

- Suitable where usage and benefits are uniform across years (e.g., leasehold buildings).

Limitations of SLM

- Assumes uniform utility which may be unrealistic.

- Repair and maintenance costs often increase over time while SLM charges remain constant, causing total periodic charges (depreciation + repairs) to be uneven.

Written Down Value Method (WDV)

- Depreciation is charged on the book value (written down value) of the asset at the beginning of each period.

- Also called the reducing balance method.

- A fixed percentage is applied to the diminishing book value, so depreciation expense falls each year.

- This method recognises that many assets lose value faster in early years.

Example: Original cost ₹2,00,000; depreciation @10% WDV produces a declining series of depreciation amounts each year.

- Book value = Original cost - Accumulated depreciation.

- Depreciation under WDV decreases over time because the base (book value) declines.

Rate of depreciation under WDV can be derived from formula relating cost, salvage value and useful life:

Example calculation: Truck cost ₹9,00,000; net salvage after 16 years ₹50,000; appropriate rate is computed using the formula above.

Advantages of WDV

- Reflects more realistic allocation of cost where assets yield higher benefits early in life.

- Balances depreciation and repair expense, giving a more uniform total expense over years.

- Accepted for income tax purposes in India.

- Reduces loss due to obsolescence by writing off more cost in earlier years.

- Suitable for long-lasting assets with increasing repair costs and assets subject to quick obsolescence.

Limitations of WDV

- Depreciable cost cannot be fully written off to zero because depreciation is a percentage of a diminishing base.

- Choosing the correct depreciation rate may be difficult.

SLM vs WDV - Comparative Analysis

- Basis of charging: SLM charges on original cost; WDV charges on net book value at period's start.

- Annual charge: SLM gives fixed annual charge; WDV yields higher initial charge which declines yearly.

- Total charge against profit: Under SLM, depreciation is constant and repair costs often increase later; under WDV, depreciation decreases and total (depreciation + repairs) is more even across years.

- Income tax recognition: SLM is not generally recognised by Income Tax Law; WDV is recognised.

- Suitability: SLM suits assets with low repair costs and low obsolescence (e.g., buildings), WDV suits machinery, vehicles and assets with higher early consumption or obsolescence risk.

Methods of Recording Depreciation

There are two principal ways of recording depreciation in the books:

1. Charging Depreciation to Asset Account

- Depreciation is deducted directly from the asset's book value.

- Journal entry records depreciation charge to Profit & Loss and credits the Asset account (or reduces asset directly).

- On the balance sheet, the asset appears at net book value (cost less accumulated depreciation/charge to date).

Balance sheet treatment: asset appears at its net book value (original cost less depreciation charged to date).

2. Provision for Depreciation / Accumulated Depreciation Account

- Asset account remains at original cost throughout; depreciation is accumulated in a separate Provision for Depreciation (accumulated depreciation) account.

- This provides clear disclosure of original cost and total depreciation charged to date.

- On the balance sheet the asset is shown at original cost and accumulated depreciation is shown either as a deduction from the asset or as a liability item.

- Journal entries: debit Profit & Loss A/c and credit Provision for Depreciation A/c for the depreciation amount.

Balance sheet treatment: fixed asset continues to show original cost; provision for depreciation appears either on liabilities side or shown as deduction from asset cost.

Illustrative Example - Journal Entries and Accounts

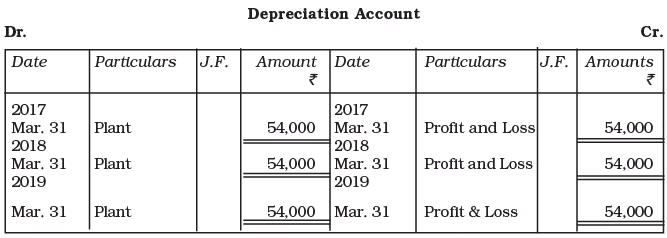

Example (M/s Singhania and Bros.) purchased a plant for ₹5,00,000 on 01.04.2017 and spent ₹50,000 on installation. Salvage value after 10 years is ₹10,000. Record journal entries for the year and show Plant Account and Depreciation Account for first three years assuming SLM and books close on 31 March and depreciation is charged to asset account.

Working Notes:

Disposal of Asset

An asset may be disposed at the end of useful life or earlier (due to obsolescence or abnormal factors). The accounting treatment differs slightly depending on the recording method used.

If an asset is sold at end of life, amount realised is credited to the asset account and the balance (if any) is transferred to Profit & Loss Account. Appropriate journal entries are passed to record sale and remove asset from books.

Where provision for depreciation account is maintained, the balance of the provision must be transferred to the asset account before recording disposal.

Illustration: R.S. Limited purchased a vehicle for ₹4,00,000. After 4 years its salvage is estimated at ₹40,000. To determine annual depreciation on straight-line basis and show vehicle account for four years if sold for ₹50,000 at the end, consider two cases: (a) depreciation charged to asset account (b) provision for depreciation account maintained

(b) When Provision for depreciation account is maintained:

Use of Asset Disposal Account

- Asset Disposal Account consolidates all transactions relating to sale/disposal of an asset.

- Key items recorded are original cost, accumulated depreciation up to date of sale, sale proceeds and value of any retained parts; resultant profit or loss is shown in the account.

- Balance of Asset Disposal Account (profit or loss) is transferred to Profit & Loss Account.

- This method is useful where part of asset is sold or where provision for depreciation is maintained and comprehensive presentation is desired.

- Journal entries for asset disposal are recorded to open and close the Asset Disposal Account.

If Asset Disposal Account shows a debit balance (loss on disposal) it is transferred to Profit & Loss A/c:

If it shows a credit balance (profit on disposal) it is closed by transferring profit to Profit & Loss A/c:

Example: Karan Enterprises balances as on 31.03.2017 - Machinery (gross) ₹6,00,000; Provision for depreciation ₹2,50,000. A machine purchased for ₹1,00,000 on 01.11.2013 with accumulated depreciation ₹60,000 was sold on 01.04.2017 for ₹35,000. Asset Disposal Account will be prepared as follows:

Working Notes:

Example: On 01.01.2015 Khosla Transport Co. purchased five trucks for ₹20,000 each. Depreciation at 10% p.a. SLM was provided and accumulated in provision for depreciation account. One truck sold on 01.01.2016 for ₹15,000. On 01.07.2017 another truck (purchased 01.01.2014 for ₹20,000) sold for ₹18,000. A new truck costing ₹30,000 purchased on 01.10.2016. Prepare Trucks Account, Provision for Depreciation Account and Truck Disposal Account for years ended Dec 2015, 2016 and 2017; firm closes accounts in December each year.

Working Notes:

Effect of Additions or Extensions to Existing Asset

- When additions or extensions are made to an existing asset to make it operational, the costs incurred are capitalised and depreciated over the relevant useful life.

- Capital additions are distinct from routine repairs and maintenance which are revenue expenses and charged to Profit & Loss.

AS-6 (Revised) Guidelines

- If an addition/extension becomes an integral part of the asset, it should be depreciated over the asset's useful life, possibly at the same rate as the existing asset.

- If an addition/extension retains a separate identity and can be used after disposal of the main asset, it should be depreciated as a separate asset over its own useful life.

Example: M/s Digital Studio bought a machine for ₹8,00,000 on 01.04.2013. Depreciation charged at 20% SLM on original cost. On 01.04.2015 a substantial modification costing ₹80,000 was made; modification is to be depreciated @20% SLM. Routine maintenance during 2013-14 was ₹2,000. Prepare Machine Account, Provision for Depreciation Account and charge to Profit & Loss for year ended 31.03.2016.

Working Notes:

- Cost of modification is capitalised; routine repairs are revenue expenditures.

- Calculation of provision for depreciation balance on 01.04.2014.

- Depreciation for 2015-16 calculated separately for original cost and capitalised modification.

- Amount charged to Profit & Loss Account presented after computing separate depreciation sums.

Provisions and Reserves

Provisions

- Provisions are amounts set aside for known liabilities or probable losses related to the current accounting period where the exact amount is uncertain.

- Examples: Provision for doubtful debts, provision for taxation, provision for repairs and renewals, provision for discount on debtors, provision for depreciation.

- Provisions are a charge against the revenue of the current period and follow the principle of prudence to ensure true profit measurement.

- Creation of a provision: debit Profit & Loss Account; credit the respective provision or liability account.

- Presentation in balance sheet: provisions are shown either as a deduction from the related asset (e.g., provision for doubtful debts deducted from debtors) or on the liabilities side (e.g., provision for taxation).

Accounting Treatment for Provisions

- Good Debts: Debtors from whom collection is certain.

- Bad Debts: Debtors from whom collection is impossible; these are written off.

- Doubtful Debts: Debtors who may or may not pay the full amount; a percentage provision is made based on experience.

- Provision for doubtful debts is generally calculated as a percentage of sundry debtors after deducting known bad debts.

- Journal entry to create provision for doubtful debts: debit Profit & Loss Account; credit Provision for Doubtful Debts Account.

Illustration with trial balance extract and additional information is provided below in image form:

Additional Information:

- Bad debts proved bad but not recorded amounted to ₹8,000.

- Provision is to be maintained at 10% of debtors.

Journal entries to create provision for doubtful debts are shown below:

Working Notes:

Reserves

- Reserves are appropriations of profit retained in the business for future needs such as expansion or to meet contingencies.

- Reserves are not a charge against profit (they are created after determining net profit) and strengthen the financial position of the business.

- Reserves appear under Reserves and Surpluses on the liabilities side of the balance sheet after capital.

- Examples: General reserve, workmen compensation fund, investment fluctuation fund, capital reserve, dividend equalisation reserve, reserve for redemption of debentures.

Difference between Reserve and Provision

- Nature: Provision is an expense deducted from profit; reserve is appropriation of profit set aside after profit calculation.

- Purpose: Provision is for known liabilities/expected losses of current period; reserve is to strengthen financial position or for specific future purposes.

- Presentation: Provisions are shown by deduction from the related asset or as liabilities; reserves are shown under liabilities after capital.

- Tax Effect: Provisions reduce taxable profit; reserves (created from profit after tax) do not reduce taxable profit.

- Compulsion: Provisions are necessary for true and fair profit determination; reserves are generally at management discretion (some reserves may be legally required).

- Use for Dividends: Provisions cannot be used for dividends; general reserves may be used for dividend distribution.

Types of Reserves

Reserves can be classified by purpose and by the nature of profit from which they are created.

- General Reserve: Created where purpose is not specified; a free reserve available for any purpose and to strengthen financial position.

- Specific Reserve: Created for a particular purpose and can only be used for that purpose (e.g., dividend equalisation reserve, workmen compensation fund, investment fluctuation fund, debenture redemption reserve).

- Reserves are also classified into:

- Revenue Reserves: Created from revenue profits (normal operating activities) and generally available for dividend distribution (e.g., general reserve).

- Capital Reserves: Created from capital profits (non-operating items) and not available for dividend distribution; used for writing off capital losses or issuing bonus shares (e.g., premium on issue of shares, profit on sale of fixed assets, profit on revaluation of assets).

Difference between Revenue Reserve and Capital Reserve

- Source of Creation:

- Revenue Reserve: Created from revenue profits arising from normal operating activities and is distributable as dividend.

- Capital Reserve: Created from capital profits not arising from regular operations and generally not distributable as dividend.

- Purpose:

- Revenue Reserve: Strengthen financial position, meet contingencies or specific revenue purposes.

- Capital Reserve: Meet legal/accounting requirements such as writing off capital losses or issuing bonus shares.

- Usage:

- Revenue Reserve: Specific revenue reserve used for its designated purpose; general reserve is freely usable including for dividends.

- Capital Reserve: Used for specific capital purposes permitted by law.

Importance of Reserves

- Reserves protect the business against unknown future expenses and losses.

- Reserves enable conservation of funds for significant future demands such as business expansion.

- Reserves strengthen the financial position and provide a source to meet contingencies, strengthen capital base or redeem long-term liabilities.

Secret Reserve

- A secret reserve is a hidden reserve not disclosed in the balance sheet.

- It reduces disclosed profits and may reduce tax liability and hide true profit position from competitors.

- Secret reserves can be created by such practices as charging higher than necessary depreciation, undervaluing inventories, charging capital expenditure to profit and loss, making excessive provisions for doubtful debts, or showing contingent liabilities as actual liabilities.

- Creation of secret reserves within reasonable limits may be justified for prudence and commercial expediency, but excessive secrecy can mislead stakeholders.

FAQs on Chapter Notes: Depreciation, Provisions and Reserves

| 1. What is depreciation and why is it important in accounting? |  |

| 2. What are the main causes of depreciation for an asset? | |

| 3. What are the different methods for calculating depreciation amounts? | |

| 4. How is depreciation recorded in financial statements? | |

| 5. What happens to the depreciation of an asset when it is disposed of? | |