Investment and Saving - Interdisciplinary Issues in Indian Commerce

What Is Investing?

Investing: The act of committing money or capital to an endeavor with the expectation of obtaining an additional income or profit.

Legendary investor Warren Buffett defines investing as “… the process of laying out money now to receive more money in the future.” The goal of investing is to put your money to work in one or more types of investment vehicles in the hopes of growing your money over time.

What is investing?

Investing is really about “working smarter and not harder.” Most of us work hard at our jobs, whether for a company or our own business. We often work long hours, which requires sacrifice and adds stress. Taking some of our hard-earned money and investing for our future needs is a way to make the most of what we earn.

Investing is also about making priorities for your money. Spending is easy and gives instant gratification—whether the splurge is on a new outfit, a vacation to some exotic spot or dinner in a fancy restaurant. All of these are wonderful and make life more enjoyable. But investing requires prioritizing our financial futures over our present desires.

Investing is a way to set aside money while you are busy with life and have that money work for you so that you can fully reap the rewards of your labour in the future. Investing is a means to a happier ending.

There are many different ways you can go about investing, including putting money into stocks, bonds, mutual funds, ETFs, real estate (and other alternative investment vehicles), or even starting your own business.

What are Savings?

Savings, according to Keynesian economics, consists of the amount left over when the cost of a person's consumer expenditure is subtracted from the amount of disposable income he earns in a given period of time. For those who are financially prudent, the amount of money left over after personal expenses have been met can be positive; for those who tend to rely on credit and loans to make ends meet, there is no money left for savings. Savings can be turned into further increased income through investing in different investment vehicles.

Breaking Down ‘Savings’:

Savings is the amount of money left over after spending. For example, Sasha’s monthly paycheck is $5,000. Her expenses include a $1,300 rent payment, $450 car payment, $500 student loan payment, $300 credit card payment, $250 for groceries, $75 for utilities, and $75 for her cell-phone and $100 for gas. Since her monthly income is $5,000 and her monthly expenses are $3,050, Sasha has $1,950 left. If Sasha saves her excess income and has an emergency, she has plenty of money to live on while resolving the issue. If Sasha does not save her extra money and her expenses exceed her income, she is living pay-check to pay-check. If she has an emergency, she does not have money to live on and must secure payments for her bills.

Examples of Bank Savings:

A current account offers unrestricted access to money with low or no monthly fees. Money is transacted through online transfers, automated teller machines (ATMs), debit card purchases or writing personal checks. A current account pays lower interest rates than other bank accounts.

A savings account pays interest on cash not needed for daily expenses but available for an emergency. Deposits and withdrawals are made by phone or mail or at a bank branch or ATM. Interest rates are higher than on current accounts.

A money market account has a higher minimum balance, pays more interest than other bank accounts and allows few monthly withdrawals through check writing privileges or debit card use.

A certificate of deposit (CD) limits access to cash in exchange for a higher interest rate. Deposit terms range from three months to five years; the longer the term, the higher the interest rate. CDs have early-withdrawal penalties that can erase interest earned; it is best to keep the money in the CD for the entire term.

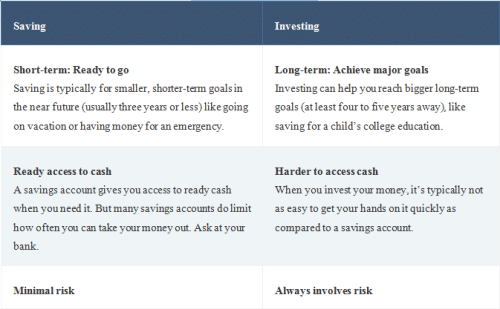

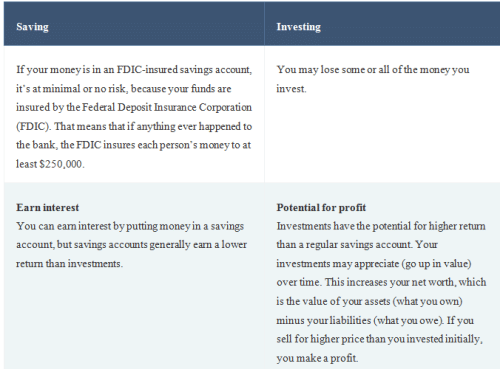

Savings Vs Investment:

Savings vs. investing

FAQs on Investment and Saving - Interdisciplinary Issues in Indian Commerce

| 1. What is the importance of investment and saving in Indian commerce? |  |

| 2. How do investments contribute to the growth of the Indian economy? | |

| 3. What are the different types of investments available in Indian commerce? | |

| 4. How can individuals effectively save money in Indian commerce? | |

| 5. What are the risks associated with investments in Indian commerce? | |