Non Life Insurance - Insurance Terminology And Insurance Customers, Principles of Insurance, B com | Principles of Insurance PDF Download

An Introduction - Indian General [Non-Life] Insurance Companies

In today’s age of consumerism, insurance requirements have expanded to keep pace with the increasing risks. Gone are the days when life insurances ruled the roost; today we have a wide assortment of risk coverage commencing from health insurance to travel insurance to theft insurance to even a wedding insurance. With affluence and spending capacity on the surge there is a growing trend to fulfill needs, deal with responsibilities and secure one’s possessions, be it good health or wordly wealth.

General insurance companies have willingly catered to these increasing demands and have offered a plethora of insurance covers that almost cover anything under the sun.

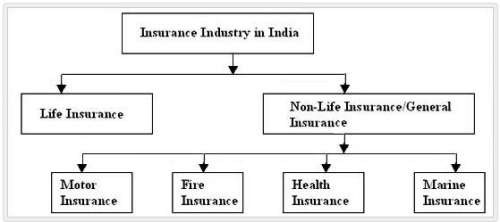

Any insurance other than ‘Life Insurance’ falls under the classification of General Insurance. It comprises of:

- Insurance of property against fire, theft, burglary, terrorism, natural disasters etc

- Personal insurance such as Accident Policy, Health Insurance and liability insurance which covers legal liabilities.

- Errors and Omissions Insurance for professionals, credit insurance etc.

- Policy covers such as coverage of machinery against breakdown or loss or damage during the transit.

- Policies that provide marine insurance covering goods in transit by sea, air, railways, waterways and road and cover the hull of ships.

- Insurance of motor vehicles against damages or accidents and theft

All these above mentioned form a major chunk of non-life insurance business.

General insurance products and services are being offered as package policies offering a combination of the covers mentioned above in various permutations and combinations. There are package policies specially designed for householders, shopkeepers, industrialists, agriculturists, entrepreneurs, employees and for professionals such as doctors, engineers, chartered accountants etc. Apart from standard covers, General insurance companies also offer customized or tailor-made policies based on the personal requirements of the customer.

A suitable general insurance cover is an absolute essential for every family. This is a necessity to overcome uncertainties and risks prevalent in life. It is also necessary to protect one’s property against risks as a loss or damage to one’s property can leave one in doldrums.

Losses created by catastrophes such as the tsunami, earthquakes, cyclones, floods, volcano eruptions or landslides have left many penniless and shelter-less. Such losses have the potential to shatter lives but availing a suitable insurance cover could help mitigate the unforeseen risks.

Similarly, an individual can be provided with a suitable insurance cover against Personal Accidents. A Health Insurance policy can provide financial relief and lowering of mental agony to an individual undergoing medical treatment on account of a disease or an injury.

It is important for prospective customers to read and understand the terms and conditions of a policy before they enter into an insurance contract. The proposal form needs to be filled in correctly and completely with all factual and relevant data by the customer. He must also ensure that the insurance cover is adequate and an appropriate one, as desired.

Classification of Indian Insurance Industry

General Insurance is also known as Non-Life Insurance in India. There are totally 16 General Insurance (Non-Life) Companies in India. These 16 General Insurance companies have been classified into two broad categories namely:

a) PSUs (Public Sector Undertakings)

b) Private Insurance Companies

a) PSUs (Public Sector Undertakings)-

These insurance companies are wholly owned by the Government of India. There are totally 4 PSUs in India namely:

- National Insurance Company Ltd

- Oriental Insurance Company Ltd

- The New India Assurance Pvt Ltd

- United India Insurance Company Ltd

b) Private Insurance Companies:

There are totally 12 private General Insurance companies in India namely:

- Apollo DKV Health Insurance Ltd

- Bajaj Allianz General Insurance Co. Ltd

- Cholamandalam MS General Insurance Co. Ltd

- Future Generali Insurance Company Ltd

- HDFC Ergo General Insurance Co Ltd

- ICICI Lombard General Insurance Ltd

- Iffco Tokio General Insurance Pvt Ltd

- Reliance General Insurance Ltd

- Royal Sundaram General Insurance Co Ltd

- Star Health and Allied Insurance

- Tata AIG General Insurance Co Ltd

- Universal Sompo General Insurance Pvt Ltd

There are basically two types of Policy Health Covers namely:

a) Individual Policy

b) Family Floater Policy

a) Individual Policy

Individual policy provides health cover for a single individual only. It is an agreement between an individual (policyholder/customer) and the insurer (insurance company). It is a legal document that is valid for a year. Such an individual policy needs to be renewed before the expiry of the contract in order to enjoy continued benefits provided by the insurance company. An individual policy can be renewed by paying the premium as stated by insurance company based on various factors and parameters. Such an individual policy is not transferable. In case, if the policyholder wants to change his policy cover from one insurance company to any other insurance company, then such a customer (insured) has to forego the benefits such as cumulative bonus or benefits during diseases or ailments being covered under the policy.

b) Family Floater Policy

A Family Floater Health Insurance Policy is a health cover wherein the entire family will be covered under a single Sum Insured. Such a policy covers reimbursement of hospitalization expenses for illness/diseases contracted or injury sustained by the Insured person, but should not exceed Sum Insured (all claims in aggregate) for that family as stated in the Schedule in any one period of insurance. Just like individual policy, this floater policy needs to be renewed before the expiry of the contract for enjoying continued benefits.General Insurance is also known as Non-Life Insurance in India. There are totally 16 General Insurance (Non-Life) Companies in India. These 16 General Insurance companies have been classified into two broad categories namely:

a) PSUs (Public Sector Undertakings)

b) Private Insurance Companies

a) PSUs (Public Sector Undertakings)-

These insurance companies are wholly owned by the Government of India. There are totally 4 PSUs in India namely:

- National Insurance Company Ltd

- Oriental Insurance Company Ltd

- The New India Assurance Pvt Ltd

- United India Insurance Company Ltd

b) Private Insurance Companies:

There are totally 12 private General Insurance companies in India namely:

- Apollo DKV Health Insurance Ltd

- Bajaj Allianz General Insurance Co. Ltd

- Cholamandalam MS General Insurance Co. Ltd

- Future Generali Insurance Company Ltd

- HDFC Ergo General Insurance Co Ltd

- ICICI Lombard General Insurance Ltd

- Iffco Tokio General Insurance Pvt Ltd

- Reliance General Insurance Ltd

- Royal Sundaram General Insurance Co Ltd

- Star Health and Allied Insurance

- Tata AIG General Insurance Co Ltd

- Universal Sompo General Insurance Pvt Ltd

There are basically two types of Policy Health Covers namely:

a) Individual Policy

b) Family Floater Policy

a) Individual Policy

Individual policy provides health cover for a single individual only. It is an agreement between an individual (policyholder/customer) and the insurer (insurance company). It is a legal document that is valid for a year. Such an individual policy needs to be renewed before the expiry of the contract in order to enjoy continued benefits provided by the insurance company. An individual policy can be renewed by paying the premium as stated by insurance company based on various factors and parameters. Such an individual policy is not transferable. In case, if the policyholder wants to change his policy cover from one insurance company to any other insurance company, then such a customer (insured) has to forego the benefits such as cumulative bonus or benefits during diseases or ailments being covered under the policy.

b) Family Floater Policy

A Family Floater Health Insurance Policy is a health cover wherein the entire family will be covered under a single Sum Insured. Such a policy covers reimbursement of hospitalization expenses for illness/diseases contracted or injury sustained by the Insured person, but should not exceed Sum Insured (all claims in aggregate) for that family as stated in the Schedule in any one period of insurance. Just like individual policy, this floater policy needs to be renewed before the expiry of the contract for enjoying continued benefits.

|

46 videos|62 docs|14 tests

|

FAQs on Non Life Insurance - Insurance Terminology And Insurance Customers, Principles of Insurance, B com - Principles of Insurance

| 1. What is non-life insurance? |  |

| 2. What are the principles of insurance? | |

| 3. Who are the customers of non-life insurance? | |

| 4. What is meant by insurance terminology? | |

| 5. What are some common frequently asked questions about non-life insurance? | |

Objective type Questions

,Important questions

,Viva Questions

,Principles of Insurance

,B com | Principles of Insurance

,mock tests for examination

,Principles of Insurance

,ppt

,Previous Year Questions with Solutions

,B com | Principles of Insurance

,shortcuts and tricks

,Summary

,Semester Notes

,B com | Principles of Insurance

,Principles of Insurance

,study material

,Exam

,Non Life Insurance - Insurance Terminology And Insurance Customers

,Sample Paper

,Non Life Insurance - Insurance Terminology And Insurance Customers

,Free

,video lectures

,past year papers

,Non Life Insurance - Insurance Terminology And Insurance Customers

,MCQs

,practice quizzes

,Extra Questions

;

Non Life Insurance - Insurance Terminology And Insurance Customers, Principles of Insurance, B com Free PDF Download

Importance of Non Life Insurance - Insurance Terminology And Insurance Customers, Principles of Insurance, B com

Non Life Insurance - Insurance Terminology And Insurance Customers, Principles of Insurance, B com Notes

Non Life Insurance - Insurance Terminology And Insurance Customers, Principles of Insurance, B com B Com Questions

Study Non Life Insurance - Insurance Terminology And Insurance Customers, Principles of Insurance, B com on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!