Input Tax Credit - Value added Tax (VAT), Indirect tax laws | Indirect Tax Laws - B Com PDF Download

Concepts of Input Tax and Output Tax

Input tax is the tax paid or payable in the course of business on purchases of any goods made from a registered dealer of the State. Output tax means the tax charged or chargeable under the Act, by a registered dealer for the sale of goods in the course of business. In simple words input tax is the tax a dealer pays on his local purchases of business inputs, which include the goods that he purchases for resale, raw materials, capital goods as well as other inputs for use directly or indirectly in his business. Output tax is the tax that a dealer charges on his sales that are subject to tax.

Input Tax Credit (ITC)

The essence of VAT is in providing set-off for the tax paid earlier, and this is given effect through the concept of input tax credit/rebate. This input tax credit in relation to any period means setting off the amount of input tax by a registered dealer against the amount of his output tax. It is reiterated that tax paid on the earlier point is called input tax. This amount will be adjusted/rebated against the tax payable by the purchasing dealer on his sales. This credit availability is called input tax credit.

Scope of input tax credit : Input tax credit shall be allowed to a registered dealer on purchase of any goods made within the State from a dealer holding a valid certificate of registration under the Act. Further, the input tax credit will be given to both manufacturers and traders for purchase of inputs/supplies meant for both sale within the State as well as to other States, irrespective of when these will be utilized/sold. Even for stock transfer/consignment transfers/branch transfer of goods out of the State, input tax paid in excess of 2% (as CST rate is 2%) will be eligible for tax credit. It is also to be noted that in some States partial input tax credit is available in respect of inputs used for manufacture of exempted goods.

Input tax credit available on capital goods : Input tax credit on capital goods will be available for traders and manufacturers. Tax credit on capital goods may be adjusted over a maximum of 36 equal monthly installments. The States may at their option reduce this number of installments. The State of Maharastra has decided to give full input tax credit in the month of purchases only. However, if the capital asset is sold within the period of 36 months proportionate input credit will be withdrawn. There is a negative list for capital goods (on the basis of principles already decided by the Empowered Committee) which are not eligible for input tax credit. The concepts relating to input tax credit on capital goods have been discussed in para 8.9 of this chapter.

Eligible Purchases for Availing Input Tax Credit

For the purpose of claiming input tax credit, the taxable goods should be purchased for any one of the following purposes:

(i) for sale/resale within the State;

(ii) for sale to other parts of India in the course of inter-State trade or commerce;

(iii) to be used as-

(a) containers or packing materials;

(b) raw materials; or

(c) consumable stores,

required for the purpose of manufacture of taxable goods or in the packing of such manufactured goods intended for sale in the State or in the course of inter-State trade or commerce;

(iv) for being used in the execution of a works contract;

(v) to be used as capital goods required for the purpose of manufacture or resale of taxable goods;

(vi) to be used as

(a) raw materials;

(b) capital goods;

(c) consumable stores and

(d) packing materials/containers for manufacturing/packing goods to be sold in the course of export out of the territory of India;

(vii) for making zero-rated sales other than those referred to in clause (vi) above.

Common goods used for taxable goods and tax-free goods : Provisions have been made in most of the States to provide that the purchases should be used for manufacture etc. of taxable goods. Taxable goods means goods other than the goods which are specified in the Schedule as tax-free goods.

Where the purchased goods are used partially for the purpose specified above, input tax credit shall be allowed proportionate to the extent the purchases are used for the purposes specified above.

Purchases not Eligible for Input Tax Credit

Input tax credit may not be allowed in the following circumstances:

(i) purchases from unregistered dealers;

(ii) purchases from registered dealer who opt for composition scheme1 under the provisions of the Act;

(iii) purchase of goods as may be notified by the State Government

(iv) purchase of goods where the purchase invoice is not available with the claimant or there is evidence that the same has not been issued by the selling registered dealer from whom the goods are purported to have been purchased;

(v) purchase of goods where invoice does not show the amount of tax separately;

(vi) purchase of goods, which are being utilized in the manufacture of, exempted goods other than exports;

(vii) goods in stock, which have suffered tax under an earlier Act but under VAT Act they are covered under exempted items;

(viii) purchase of goods used for personal use/consumption or provided free of charge as gifts);

(ix) goods imported from outside the territory of India (commonly known as high seas purchases);

(x) goods imported from other States viz. inter-State purchases.

(xi) goods like motor vehicles, toilet articles, furniture etc. which are not used in relation to production of goods or held for sale/resale.

Concept of Input Tax Credit on Capital Goods A dealer has to purchase capital goods, which may include plant and machinery, furniture, fixture, electrical installations, vehicles etc. Similarly, a dealer may be creating capital assets himself by purchasing materials. Normally all the above items are taxable and the dealer has to pay sales-tax on purchase of the above goods. Each State-VAT legislations may define ‘capital goods’ differently. Normally, under VAT system the dealer should get full credit for tax paid on such purchases, more particularly when the basic principle is to avoid the cascading effect. These assets are used for the business and while fixing sale price of the products, the dealer has to include some portion towards the cost of the acquisition of these assets as part of the sale price. If the input credit is not allowed in full then certainly, to the extent of disallowance, the principle of VAT gets defeated. For example, a dealer has purchased furniture for his business, costing ` 1,00,000/-. Assuming that the vendor has charged tax @ 12.5%, Now, if the credit for VAT paid is allowed, the dealer can consider the cost of acquisition at ` 1,00,000/-. If the credit of tax paid is not allowed then he has to consider the cost of purchase at ` 1,12,500/-. While marking up his price on account of establishment cost he has to consider this cost of furniture as one of the components. If cost remains higher, obviously to that extent the mark up will go up. If the cost is lower i.e. after considering input credit of ` 12,500/-, the cost will be lower and to that extent the mark up will also be lower, resulting in an overall lower sale price. When tax paid on purchases is included in cost, the said tax indirectly gets reflected in the sale price and hence there is also an element of tax upon tax. This cascading effect can very well be imagined from the above example. Depending upon the volume of capital goods and the tax component on the same, the magnitude of the cascading effect can be imagined.

3.9.1 Policy in the white paper : The policy lays down that in relation to capital goods, set off will be available to traders and manufacturers. The most important factor is that the White Paper recognizes the fact that set off is to be given to both traders and manufacturers. It is well known that under traditional sales-tax system, in some States, partial credit was allowed on capital goods to the manufacturers but no credit was allowed to traders. The White Paper, taking into account the very basis of VAT system, laid down a policy statement that set off will be allowed to both manufacturers and traders.

However as per the White Paper, the State Governments can provide to give set off on a staggering basis, at the most in 36 instalments. This is subject to the policy of individual States.

3.9.2 Restrictions on credit relating to capital goods : It should be noted that credit on capital goods is not being allowed across the floor. As per the White Paper, there will be a negative list for capital goods which will be based on certain pre-agreed principles by the Empowered Committee. The capital goods mentioned in the negative list would not be eligible for input tax credit. However, it appears that the States have taken their own decisions to provide negative lists or reduction in set off in respect of capital goods.

3.9.3 Procedural requirements for claim of set off Barring the items covered by the negative list and subject to retention rules, the dealers are entitled to set off on capital goods like any other purchases. Thus, the dealer will have to bifurcate their purchase into capital goods eligible for set off and capital goods not so eligible.

In respect of eligible capital goods, the dealer will be required to follow the procedural requirements for claiming set off successfully. For example, dealers will be required to support purchase of capital goods with tax invoice. In the absence of such tax invoice set off will be disallowed.

Once a dealer is entitled to set off, he has to further comply with the relevant provisions in respect of allowability. If it is subject to certain installments, the dealer will be required to claim set off accordingly in his returns. If the set off is subject to prior permission, the same should be duly obtained.

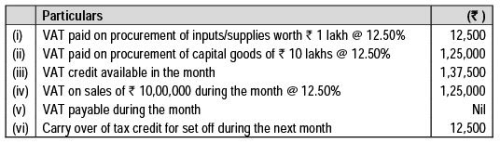

The allowable set off on capital goods will be, of course, part of normal set off. The dealer will be able to adjust this set off against his other VAT liability. For example, dealer can adjust his set off as per the following illustration:

It may be mentioned here that the set off under VAT Acts are subject to one very important condition. It is generally provided in VAT Acts that the set off on any goods should not exceed the tax received on the same goods in Government Treasury. Therefore, the purchasing dealer, desirous of claiming set off, should also look into the credentials of the vendor so as to be sure that he will get the set off of tax paid to him.

|

50 videos|54 docs

|

FAQs on Input Tax Credit - Value added Tax (VAT), Indirect tax laws - Indirect Tax Laws - B Com

| 1. What is Input Tax Credit? |  |

| 2. How does Input Tax Credit work? | |

| 3. Can all businesses claim Input Tax Credit? | |

| 4. Are there any restrictions on claiming Input Tax Credit? | |

| 5. What are the benefits of claiming Input Tax Credit? | |

|

4.65/5 Rating |

|

Dec 23, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Summary

,video lectures

,past year papers

,ppt

,shortcuts and tricks

,Sample Paper

,Extra Questions

,Viva Questions

,Input Tax Credit - Value added Tax (VAT)

,Indirect tax laws | Indirect Tax Laws - B Com

,Semester Notes

,Indirect tax laws | Indirect Tax Laws - B Com

,Previous Year Questions with Solutions

,study material

,Indirect tax laws | Indirect Tax Laws - B Com

,Input Tax Credit - Value added Tax (VAT)

,practice quizzes

,Important questions

,Objective type Questions

,Exam

,Free

,MCQs

,mock tests for examination

,Input Tax Credit - Value added Tax (VAT)

;

Input Tax Credit - Value added Tax (VAT), Indirect tax laws Free PDF Download

Importance of Input Tax Credit - Value added Tax (VAT), Indirect tax laws

Input Tax Credit - Value added Tax (VAT), Indirect tax laws Notes

Input Tax Credit - Value added Tax (VAT), Indirect tax laws B Com Questions

Study Input Tax Credit - Value added Tax (VAT), Indirect tax laws on the App

|

© EduRev

|

Education Revolution

|

|