Computation of Service Tax - Indirect Tax Laws | Indirect Tax Laws - B Com PDF Download

Service tax calculation is easy and simple to understand. Service tax is levied at a fixed rate. This rate is applied on the gross value of taxable services and the result is called output service tax. The output service tax is then adjusted with the input service tax credit and if there is any positive balance then same is paid to the government otherwise negative balance carried forward to next period.

Let us understand the service tax calculation in detail.

Determine the output service tax payable

As mentioned earlier service tax rate is levied on the taxable value of services. For example, a doctor provides services of Rs. 50,000, then he will have to collect service tax @ 14.5% on Rs. 50,000/- i.e Rs. 7250/-.

He will raise the bill as given below:

| Particulars | Amount in Rs. |

| Doctor’s Fee | 50,000 |

| Service tax @14.5% | 7,250 |

| Total | 57,250 |

In the above case the Doctor knew in advance that how much he needed to charge as service tax and accordingly he added in the bill and collected from the client.

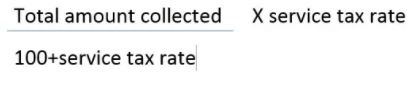

But there may be a case when the Doctor recovered only the Fees from the customer and forget to charge service tax. In this case it will be assumed that the total amount collected includes service tax portion also.

The formula to exclude the service tax portion is given below:

Hence the service tax portion will be calculated as given below:

50,000/114.5 X 14.5 = Rs. 6,332/-

So, Rs. 6,332 will be service tax amount and Balance Rs. 43,668 will be doctor’s fee.

If you will calculate the 14.5% of 43,668 you will get Rs. 6,332/-

Read:

New Current Service tax rates

Determine the input service tax payable

It is quite easy to calculate. You need to sum up all input service tax paid by you on input services used for providing taxable services.

Remember that no input credit is available for Swatch Bharat Cess. So the output Swatch Bharat Cess @0.5% need to paid in full.

Balance Tax payable or credit carried forward

The balance amount will be calculated as given below:

| Output service tax payable | XXXX |

| Less: Input service tax available | XXXX |

| Balance Service tax payable, if positive otherwise carried forward to adjust with next month balance. | XXXX |

You can also claim service tax exemption of Rs. 10 Lac.

Read:

Small service provider exemptions

Please comment for any query on service tax calculations.

|

60 videos|60 docs

|

FAQs on Computation of Service Tax - Indirect Tax Laws - Indirect Tax Laws - B Com

| 1. What is service tax and how is it computed? |  |

| 2. What are the different methods of computing service tax? | |

| 3. Are there any exemptions or abatements available for service tax computation? | |

| 4. How is service tax computed for composite services? | |

| 5. What are the penalties for non-compliance in service tax computation? | |

MCQs

,Summary

,Computation of Service Tax - Indirect Tax Laws | Indirect Tax Laws - B Com

,Sample Paper

,Computation of Service Tax - Indirect Tax Laws | Indirect Tax Laws - B Com

,Objective type Questions

,Extra Questions

,Important questions

,Previous Year Questions with Solutions

,Semester Notes

,Computation of Service Tax - Indirect Tax Laws | Indirect Tax Laws - B Com

,study material

,Viva Questions

,Exam

,past year papers

,video lectures

,shortcuts and tricks

,Free

,practice quizzes

,ppt

,mock tests for examination

;

Computation of Service Tax - Indirect Tax Laws Free PDF Download

Importance of Computation of Service Tax - Indirect Tax Laws

Computation of Service Tax - Indirect Tax Laws Notes

Computation of Service Tax - Indirect Tax Laws B Com Questions

Study Computation of Service Tax - Indirect Tax Laws on the App

|

© EduRev

|

Education Revolution

|

|