History of Income Tax in India, Income Tax Laws | Income Tax Laws - B Com PDF Download

TAX AND ITS ORIGIN

Tax is a mandatory liability for every citizen of the country. There are two types of tax in India:

- Direct

- Indirect

Taxation in India is rooted from the period of Manu Smriti and Arthashastra. Present Indian tax system is based on this ancient tax system which was based on the theory of maximum social welfare. It was only for the good of his subjects that he collected taxes from them, just as the Sun draws moisture from the Earth to give it back a thousand fold-By Kalidas in Raghuvansh eulogizing KING DALIP.

- The origin of the word "Tax" is from "Taxation" which means an estimate.

- In India, the system of direct taxation as it is known today has been in force in one form or another even from ancient times. Variety of tax measures are referred in both Manu Smriti and Arthashastra. The wise sage advised that taxes should be related to the income and expenditure of the subject. He, however, cautioned the king against excessive taxation; a king should neither impose high rate of tax nor exempt all from tax.

- According to Manu Smriti, the king should arrange the collection of taxes in such a manner that the tax payer did not feel the pinch of paying taxes. He laid down that traders and artisans should pay 1/5th of their profits in silver and gold, while the agriculturists were to pay 1/6th, 1/8th and 1/10th of their produce depending upon their circumstances.

- Kautilya has also described in great detail the system of tax administration in the Mauryan Empire. It is remarkable that the present day tax system is in many ways similar to the system of taxation in vogue about 2300 years ago.

- Arthashastra mentioned that each tax was specific and there was no scope for arbitrariness. Tax collectors determined the schedule of each payment, and its time, manner and quantity being all pre-determined. The land revenue was fixed at 1/6 share of the produce and import and export duties were determined on ad-valorem basis. The import duties on foreign goods were roughly 20% of their value. Similarly, tolls, road cess, ferry charges and other levies were all fixed.

- Kautilya also laid down that during war or emergencies like famine or floods, etc. the taxation system should be made more stringent and the king could also raise war loans. The land revenue could be raised from 1/6th to 1/4th during the emergencies. The people engaged in commerce were to pay big donations to war efforts.

- Kautilya's concept of taxation emphasised equity and justice in taxation. The affluent had to pay higher taxes as compared to the poor.

BRIEF HISTORY OF INCOME TAX IN INDIA

- In India, this tax was introduced for the first time in 1860, by Sir James Wilson in order to meet the losses sustained by the Government on account of the Military Mutiny of 1857. In 1918, a new income tax was passed and again it was replaced by another new act which was passed in 1922.This Act remained in force up to the assessment year 1961-62 with numerous amendments.

- In consultation with the Ministry of Law finally the Income Tax Act, 1961 was passed. The Income Tax Act 1961 has been brought into force with 1 April 1962. It applies to the whole of India and Sikkim (including Jammu and Kashmir).

- Since 1962 several amendments of far-reaching nature have been made in the Income Tax Act by the Union Budget every year.

- Central Board of Revenue bifurcated and a separate Board for Direct Taxes known as Central Board of Direct Taxes (CBDT) constituted under the Central Board of Revenue Act, 1963.

- The major tax enactment in India is the Income Tax Act, 1961 passed by the Parliament, which imposes a tax on the income of persons.

THIS ACT IMPOSES A TAX ON INCOME UNDER THE FOLLOWING FIVE HEADS:

(i) Income from salaries

(ii) Income from business and profession

(iii) Income in the form of capital gains

(iv) Income from house property

(v) Income from other sources

IN TERMS OF THE INCOME TAX ACT, 1961, A PERSON INCLUDES:

- Individual

- Company

- Firm

- Association of Persons (AOP)

- Hindu Undivided Family (HUF)

- Body of Individuals (BOI)

- Local authority

- Artificial Judicial person not falling in any of the preceding categories

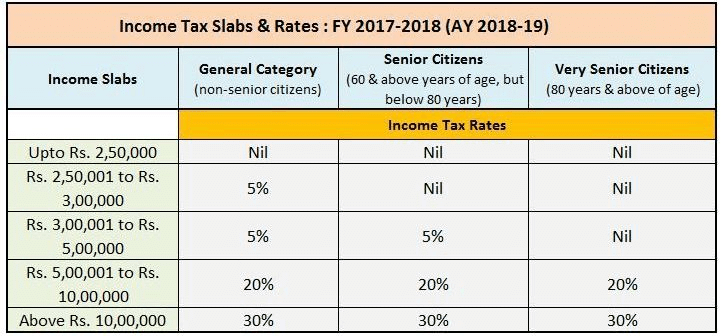

TAX SLABS IN INDIA:

(i) The Latest income tax slabs based on the Union budget presented on 29 February 2016.

(ii) The Minister of Finance Mr. Arun Jaitley presented the union budget on 29 February 2016. Following are the major highlights of the latest income tax slab.

WHY ARE TAXES IMPOSED?

- Everybody is obliged by law to pay taxes. Total Tax money goes to government exchequer. Appointed government decides that how are taxes being spent and how the budget is organized.

- Tax payment is not optional; an individual has to pay tax if his/her incoming is coming under the income tax slab. It is a duty of every citizen to pay taxes. More collection of tax allows the government to launch more and more welfare schemes.

LET'S LOOK AT THE REASONS WHY DO WE PAY TAXES?

1. To Provide Basic Facilities for Every Citizen of the Country: Whatever money is received by the government in terms of direct tax and indirect tax is spent by it for the welfare of the citizens of the country. Some of the services provided by the government are: health care, electricity, roads, education system, free houses for poor, water supply, police, firefighters, judiciary system, disaster relief, taking care of bridges and other things of public welfare.

2. To Finance Multiple Governments: All the local government of the state like village panchayats, block panchayats and municipal corporations receive fund from the state finance commission.

3. Protection of the Life: Tax payers receive the protection of life and wealth from the government in case of external aggression, internal armed rebellion or any other situation in exchange of tax paid by them.

DISSATISFACTION WITH TAXES

We often hear that there are so many scams in the country which confiscates the precious public money. There are so many other reasons given below, which lead to dissatisfaction with taxes.

a. Rate of tax is too high.

b. Unfair collection of tax from the people. Some rich people pay less tax while poor people pay high and vice versa.

c. Government is wasting tax money (inefficiency).

d. Government is spending money on wrong or unnecessary things.

|

27 videos|25 docs|12 tests

|

FAQs on History of Income Tax in India, Income Tax Laws - Income Tax Laws - B Com

| 1. What is the history of Income Tax in India? |  |

| 2. What are the Income Tax Laws in India? | |

| 3. What is the significance of income tax in India? | |

| 4. What are the penalties for not filing income tax returns in India? | |

| 5. How can one reduce their tax liability in India? | |

|

14.8K Views |

|

4.98/5 Rating |

|

Dec 23, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

practice quizzes

,Income Tax Laws | Income Tax Laws - B Com

,video lectures

,Objective type Questions

,History of Income Tax in India

,mock tests for examination

,Important questions

,Summary

,past year papers

,History of Income Tax in India

,study material

,shortcuts and tricks

,Free

,Exam

,Previous Year Questions with Solutions

,Income Tax Laws | Income Tax Laws - B Com

,History of Income Tax in India

,Semester Notes

,Viva Questions

,MCQs

,Extra Questions

,ppt

,Income Tax Laws | Income Tax Laws - B Com

,Sample Paper

;

History of Income Tax in India, Income Tax Laws Free PDF Download

Importance of History of Income Tax in India, Income Tax Laws

History of Income Tax in India, Income Tax Laws Notes

History of Income Tax in India, Income Tax Laws B Com Questions

Study History of Income Tax in India, Income Tax Laws on the App

|

© EduRev

|

Education Revolution

|

|