Meaning of Residential Status under Income Tax - Income Tax Laws | Income Tax Laws - B Com PDF Download

Introduction

Tax is levied on total income of assessee. Under the provisions of Income-tax Act, 1961, the total income of each person is based upon his residential status.

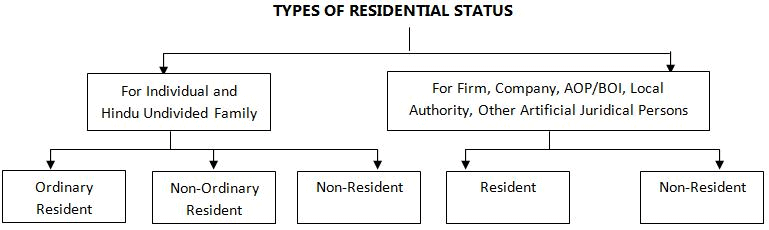

Section 6 of the Act divides the assessable persons into three categories:

- Ordinary Resident;

- Resident but Not Ordinarily Resident; and

- Non-Resident.

Residential status is a term coined under Income Tax Act and has nothing to do with nationality or domicile of a person. An Indian, who is a citizen of India can be non-resident for Income-tax purposes, whereas an American who is a citizen of America can be resident of India for Income-tax purposes. Residential status of a person depends upon the territorial connections of the person with this country, i.e., for how many days he has physically stayed in India.

The residential status of different types of persons is determined differently. Similarly, the residential status of the assessee is to be determined each year with reference to the “previous year”. The residential status of the assessee may change from year to year. What is essential is the status during the previous year and not in the assessment year.

Important Points

- Residential Status in a previous year: Residential status is to be determined for each previous year.

It implies that:- Residential status of assessment year is not important.

- A person may be resident in one previous year and a non-resident in India in another previous year, e.g., Mr. A is resident in India in the previous year 2008-09 and in the very next year, he becomes a non-resident in India.

- Duty of Assessee: It is assessee’s duty to place relevent facts, evidence and material before the Income Tax Authorities supporting the determination of Residential status.

- Dual Residential Status is possible: A person may be resident of one or more countries in a relevant previous year e.g., Mr. X may be resident of India during previous year 2Ol7-18 and he may also be resident/non-resident in England in the same previous year.

The emergence of such a situation depends upon the following:- the existence of the Residential status in countries under considerations

- the different set of rules having laid down for determination of residential status.

Determination of Residential status of different ‘Persons’

As we know that Income tax is charged on every person. The term ‘Person’ has been defined under section 2(31) includes:

- An individual

- Hindu Undivided Family

- Firm

- Company

- AOP/BOI

- Local authority

- Every other artificial juridical person not falling in preceding six sub-classes.

Therefore, it is essential to determine the residential status of above various types of persons and now, we shall learn the calculation of residential status of each type of person.

Resident (Ordinary Resident) [Section 6(1)]

Section 6 of Income Tax Act, 1961 contains provision relating to Residence in India. The taxability of an assessee is dependent on the Residential status during any Previous Year.

Individual

Income tax Act classifies Individual into 3 categories for the purpose of taxation in any Previous Year which are as follows:

- Resident and Ordinarily Resident (“ROR”)

- Resident and Not Ordinarily Resident (“RNOR”)

- Non-Resident(“NR”)

The scope of Total Income taxable under Income Act differs in each category and hence it becomes important for an Individual to know his/her Residential Status in any particular Previous Year.

Section 6 of Income Tax Act, 1961

An Individual is said to be Resident of India in any Previous Year if, period of physical stay in India is:

- First Criteria: 182 days or more, in that Previous Year, OR,

- Second Criteria: 60 days or more in that Previous Year AND 365 days or more in Preceding 4 years.

If an assessee fails to meet both the above criteria in any Previous Year, then he is considered as Non-Resident for tax purpose in that Previous Year.

Non-Applicability of Second Criteria: (60 Days+365 Days)

The following category of Individual will be classified as Resident of India only if Physical stay in Previous Year is 182 days or more:

- Citizen of India leaving India in any previous year:

- For Employment outside India

- As a crew member of an Indian Ship

- Citizen of India or Person of Indian Origin (Staying outside India) visit India in any Previous Year AND Total Income does not exceed 15 lakhs (Other than Foreign Source)

(Author’s view: This will help above Individuals to visit or stay in India for longer duration either to meet their families or manage their assets etc. without being classified as Residents of India.)

Applicability of Second Criteria with some Modification: (60 Days+365 Days)

The second criteria applicable subject to modifications in the below case: Citizen of India or Person of Indian Origin (Staying outside India) visit India in any Previous Year AND Total Income exceeds 15 lakhs (Other than Foreign Source)

Modifications: Period of Physical stay in India in any Previous Year is 120 days or more AND 365 days or more in Preceding 4 years.

(Author’s view (Citizen of India or PIO): When “Indian source income” or “Other than foreign source” income does not exceed 15 lakhs, then only physical stay of 182 days or more in the previous year triggers residency (Second criteria not required). However, when such income exceeds 15 lakhs, then in addition to first criteria of 182 days or more, the physical stay of 120 days or more in the previous year and 365 days or more in preceding 4 years also triggers residency)

Deemed Indian Resident

An Individual will be considered as Deemed Resident in the below case:

- Individual being a Citizen of India, AND

- having Total Income in excess 15 lakhs in the Previous Year (Other than foreign Source) AND

- not liable to tax in any other country/territory, by reason of domicile, residence or any similar criteria.

(Author’s view: Now Indian citizen having Indian source income exceeding 15 lakhs, cannot escape taxation. Earlier there would have been possibilities that such Individual were able to structure their stays in different countries in such a manner so as to escape taxation)

Not Ordinarily Resident (NOR)

An Individual is said to be Not Ordinarily Resident in below 4 cases:

- Individual who has been Non-Resident in India for 9 out of 10 preceding years,

OR - Individual has been in India for 729 days or less in preceding 7 years.

(If an assessee does not fall in both the above criteria in any Previous Year, then he is considered as Ordinarily Resident for tax purpose in that Previous Year) - Citizen of India or Person of Indian Origin, having total income exceeding 15 lakhs (other than foreign source) and stays in India for 120 days or more but less than 182 days.

- Deemed Resident of India.

Explanation

“Income from foreign sources” means income which accrues or arises outside India except income derived from a business controlled in or a profession set up in India and which is not deemed to accrue or arise in India

“Non-resident Indian (NRI)” means an individual, being a citizen of India or a person of Indian origin who is not a “Resident”.

“Person of Indian Origin (PIO)”: A person shall be deemed to be of Indian origin if

- he, or

- either of his parents or

- any of his grand-parents, was born in undivided India;

Hindu Undivided Family

A HUF is said to be resident in India in any previous year in Every Case Except where during that year the control and management of its affairs is situated wholly outside India.

Not Ordinarily Resident (NOR)

An HUF is said to be Not Ordinarily Resident if:

- Manager of HUF, has been Non-Resident in India for 9 out of 10 preceding years, OR

- Manager of HUF, has been in India for 729 days or less in preceding 7 years.

Company

A Company is said to be a resident in India in any previous year, if:

- it is an Indian company; OR

- its place of effective management, in that year, is in India.

Explanation: “Place of effective management” means a place where key management and commercial decisions that are necessary for the conduct of business of an entity as a whole are, in substance made.

Others

Every other person is said to be resident in India in any previous year in every case, except where during that year the control and management of his affairs is situated wholly outside India.

General

If a person is resident in India in a previous year relevant to an assessment year in respect of any source of income, he shall be deemed to be resident in India in the previous year relevant to the assessment year in respect of each of his other sources of income.

Important Points

- Meaning of Stay in India: It means stay anywhere within Indian geographical territory, i.e., anywhere in Indian villages, towns, cities, waters, or mountains.

- Stay may be continuous or intermittent: Stay in India for specified days should not necessarily be continuous. It means a person is not required to stay 182 days at a stretch as per Sec. 6(1), i.e., a person stays in India in the months of April, May, and June and then left India and stayed for 5 months in a foreign country and then came back and stayed in India upto 31st March. In such a case, the stay in India will be counted by adding a stay in India on each different occasion.

- Stay need not be at one place: A person must stay within Indian territory and where he stays is not an important consideration.

- Object of stay is not important: It is immaterial whether he stays in India for business purposes or on a personal purposes or visits India as a tourists.

- Calculation of ‘period of stay’ in India: The ‘period of stay’ in India is to be calculated on the basis of actual stay of an individual in India during the relevant previous year. Thus, if a person stays in India for a part of the day (i.e., for certain hours etc. only) then period of stay in India is to be calculated on hourly basis. Thus, a stay of 24 hours will be taken as stay of one day and total hourly stay in India will be converted into days.

However, if detail of hourly stay in India is not available then period of stay in India is to be calculated in days. It is important to note that while calculating the period of stay in India (in days), both the day of departure from India and the day of arrival in India are to be counted as stay in India.

Amendment relating to Residential Status (applicable for AY 2021-22 & onwards)

Prior to the amendment, an individual, being a person of Indian origin and who came on a visit to India during the previous year was considered as a resident in India only if his period of stay during the relevant previous year was 182 days or more (second basic condition was not required to be tested).

However, after the amendment, a dual condition has been set for determining of the residential status for such Indian citizens visiting India. Under section 6(1), an individual, being a person of Indian origin and who comes on a visit to India during the previous year will be considered as a resident in India, if:

- He stayed in India for a total period of 120 days or more during the previous year AND for 365 days or more during the 4 years immediately preceding the relevant previous year; AND

- His total income other than income from foreign sources exceeds Rs. 15,00,000. However, if the total income does not exceed Rs. 15,00,000, the said individual would be a resident in India, only if he stayed in India for a total period of 182 days or more during the previous year.

Practical example

Dhruv, a person of Indian origin and citizen of USA, got married to Deepa, an Indian citizen residing in USA, on 4th February, 2020, and came to India for the first time on 20th February, 2020. He stayed in India for 164 days during FY 2020-21.

Case 1: During FY 2020-21, Dhruv received gifts in India amounting to Rs. 2,82,000 from friends of his wife in India. Determine his residential status and compute the total income chargeable to tax along with the amount of tax payable on such income for the Assessment Year 2021-22.

Case 2: If he had received Rs. 16,00,000 instead of Rs. 2,82,000 as gifts during the previous year 2020-21 and he stayed in India for 400 days during the 4 years preceding the previous year 2020-21, what will be his residential status and tax liability?

Analysis

In the present case, since Dhruv is a person of Indian origin visiting India, the dual condition prescribed by the amendment needs to be tested.

Case 1: Dhruv stayed in India for more than 120 days in the previous year (i.e 164 days) but did not stay for 365 days or more during the 4 years immediately preceding the relevant previous year. Also, his total income did not exceed 15 lacs. It was only Rs. 282,000. Hence, he will be treated as a non-resident during FY 2020-21. His total tax payable will be Rs. 1,660. {[5% * (282,000-250,000) ] + 4% * 1600}.

Note: Rebate u/s 87A is not available to non-residents.

Case 2: Dhruv stayed in India for more than 120 days in the previous year (i.e. 164 days) and for more than 365 days during the 4 years immediately preceding the previous year (i.e 400 days). Also, his total income during FY 2020-21 exceeded Rs. 15 lacs (i.e Rs. 16 lacs in the instant case). Hence, he will be treated as a resident during FY 2020-21 under Case 2.

His total tax payable under the normal provisions will be Rs. 304,200.

|

27 videos|25 docs|12 tests

|

FAQs on Meaning of Residential Status under Income Tax - Income Tax Laws - Income Tax Laws - B Com

| 1. What is the meaning of residential status under income tax? |  |

| 2. What is an Ordinary Resident? | |

| 3. What is the significance of residential status under income tax? | |

| 4. What is the difference between Resident and Non-Resident under income tax? | |

| 5. What are the tax implications for Resident but Not Ordinarily Resident under income tax? | |

|

13K Views |

|

4.90/5 Rating |

|

Dec 23, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Important questions

,shortcuts and tricks

,Sample Paper

,Meaning of Residential Status under Income Tax - Income Tax Laws | Income Tax Laws - B Com

,Extra Questions

,Free

,study material

,Semester Notes

,Viva Questions

,Meaning of Residential Status under Income Tax - Income Tax Laws | Income Tax Laws - B Com

,ppt

,video lectures

,practice quizzes

,MCQs

,past year papers

,Meaning of Residential Status under Income Tax - Income Tax Laws | Income Tax Laws - B Com

,mock tests for examination

,Exam

,Previous Year Questions with Solutions

,Objective type Questions

,Summary

;

Meaning of Residential Status under Income Tax - Income Tax Laws Free PDF Download

Importance of Meaning of Residential Status under Income Tax - Income Tax Laws

Meaning of Residential Status under Income Tax - Income Tax Laws Notes

Meaning of Residential Status under Income Tax - Income Tax Laws B Com Questions

Study Meaning of Residential Status under Income Tax - Income Tax Laws on the App

|

© EduRev

|

Education Revolution

|

|