Methods of Valuation of Goodwill - Valuation of Goodwill & Shares, Advanced Corporate Accounting | Advanced Corporate Accounting - B Com PDF Download

1. Years’ Purchase of Average Profit Method:

Under this method, average profit of the last few years is multiplied by one or more number of years in order to ascertain the value of goodwill of the firm. How many years’ profit should be taken for calculating average and the said average should be multiplied by how many number of years — both depend on the opinions of the parties concerned. The average profit which is multiplied by the number of years for ascertaining the value of goodwill is known as Years Purchase. It is also called Purchase of Past Profit Method or Average Profit Basis Method.

Profit Basis Method:

Value of Goodwill = Average Profit x Years’ Purchase

Illustration 1:

Majumdar & Co. decides to purchase the business of Banerjee & Co. on 31.12.2003. Profits of Banerjee & Co. for the last 6 years were: 1998 Rs. 10,000; 1999 Rs. 8,000; 2000 Rs. 12,000; 2001 Rs. 16,000, 2002 Rs. 25,000 and 2003 Rs. 31,000.

The following additional information about Banerjee & Co. were also supplied:

(a) A casual income of Rs. 3,000 was included in the profit of 2000 which can never be expected in future.

(b) Profit of 2001 was reduced by Rs. 1,000 as a result of an extraordinary loss by fire.

(c) After acquisition of the business, Majumdar & Co. has to pay insurance premium amounting to Rs. 1,000 which was not paid by Banerjee & Co.

(d) S. Majumdar, the proprietor of Majumdar & Co., was employed in a firm at a monthly salary of Rs. 1,000 p.m. The business of Banerjee & Co. was managed by a salaried manager who was paid a monthly salary of Rs. 4,000. Now, Mr. Majumdar decides to manage the firm after replacing the manager.

Compute the value of Goodwill on the basis of 3 years’ purchase of the average profit for the last 4 years.

Solution:

2. Years’ Purchase of Weighted Average Method:

This method is the modified version of Years’ Purchase of Average Profit Method. Under this method, each and every year’s profit should be multiplied by the respective number of weights, e.g. 1, 2, 3 etc., in order to find out the value of product which is again to be divided by the total number of weights for ascertaining the weighted average profit. Therefore, the weighted average profit is multiplied by the years’ purchase in order to ascertain the value of goodwill. This method is particularly applicable where the trend of profit is rising.

Value of Goodwill = Weighted Average Profit x Years Purchase

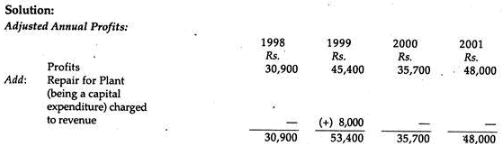

Illustration 2:

XYZ Co. Ltd. intends to purchase the business of ABC Co. Ltd. Goodwill for this purpose is agreed to be valued at 3 years’ purchase of the weighted average profits of the past four years.

The appropriate weights to be used:

1998 — 1; 1999 — 2; 2000 — 3; 2001-4.

The profits for these years were:

The following information were available:

(a) On 1.9.1999 a major repair was made in respect of a Plant at a cost of Rs. 8,000 and this was charged to revenue. The said sum is agreed to be capitalized for Goodwill calculation subject to adjustment of depreciation of 10% p.a. on Diminishing Balance Method.

(b) The Closing Stock for the year 2000 was overvalued by Rs. 3,000.

(c) To cover the Management cost an annual charge of Rs. 10,000 should be made for the purpose of Goodwill valuation.

You are asked to compute the value of Goodwill of the company.

3. Capitalisation Method:

Under this method, the value of the entire business is determined on the basis of normal profit. Goodwill is taken as the difference between the Value of the Business minus Net Tangible Assets.

Under this method, the following steps should be taken into consideration for ascertaining the amount of goodwill:

(i) Expected Average Net Profit should be ascertained;

(ii) Capitalised value of profit is to be calculated on the basis of normal rate of return;

(iii) Net Tangible Assets (i.e. Total Tangible Assets – Current Liabilities) should also be calculated;

(iv) To deduct (iii) from (ii) in order to ascertain the value of Goodwill.

Capitalised Value of Profit = Profit (Adjusted)/Normal Rate of Return x 100

Value of Goodwill = Capitalised Value of Profit – Net Tangible Assets

Illustration 3:

The following is the Balance Sheet of P. Ltd. as at 31.12.2009:

The profits of the past four years (before providing for taxation) were:

2006 — Rs. 20,000; 2007 — Rs. 30,000; 2008 — Rs. 36,000 and 2009 — Rs. 40,000.

Compute the value of Goodwill of the company assuming that the normal rate of return for this type of company is 10%. Income Tax is payable @ 50% on the above profits.

Illustration 4:

From the following Balance Sheet and other necessary information of P. Ltd. for the year ended 31.12.2001, compute the value of Goodwill by the application of Capitalisation Method:

The company commenced operation in 1997 with a paid-up capital of Rs. 2, 00,000.

Profits earned before providing for taxation have been:

1997 — Rs. 90,000; 1998 — Rs. 95,000; 1999 — Rs. 1, 05,000; 2000 — Rs. 80,000; 2001 — Rs. 1, 10,000.

Assume that Income-Tax @ 50% has been payable on these profits. Dividends have been distributed from the profits of the first three years @ 10% and for those of the next two years @ 15% on the Paid-up Capital.

4. Annuity Method:

Under this method, Super-profit (excess of actual profit over normal profit) is being considered as the value of annuity over a certain number of years and, for this purpose, compound interest is calculated at a certain respective percentage. The present value of the said annuity will be the value of goodwill.

Value of Goodwill,

V =

Where

V = Present value of Annuity

a = Annual Super Profit

n = Number of Years

I = Rate of Interest

Illustration 5:

From the following particulars, compute the value of goodwill under Annuity Method:

Super-Profit Rs. 10,000

Number of years over which Super-Profit is to be paid 5

Rate Per cent p.a. 5%

Computation of Goodwill:

5. Super-Profit Method:

Super-profit represents the difference between the average profit earned by the business and the normal profit (on the basis of normal rate of return for representative firms in the industry) i.e., the firm’s anticipated excess earnings. As such, if there is no anticipated excess earning over normal earnings, there will be no goodwill.

This method for calculating goodwill depends on:

(i) Normal rate of return of the representative firms;

(ii) Value of capital employed/Average capital employed; and

(iii) Estimated future profit, i.e. the average profit of the last few years.

Super-Profit = Average Profit (Adjusted) – Normal Profit

Value of Goodwill = Super-Profit x Years’ Purchase

The students should remember that the number of years’ purchase of goodwill differs from firm to firm and industry to industry. One or two years’ purchase should be taken into consideration if the retiring partner of a business was the main source of success. It should also be remembered that three to five years’ purchase is usually taken. Of course, a large number of years’ purchase may be considered if the super-profit itself is found to be large. If there is a declining trend in super-profit, one or two years’ purchase may be considered.

The following steps should carefully be followed for calculating the value of Goodwill under Super- Profit Method:

(a) Ascertain the amount of Capital Employed/Average Capital Employed;

(b) Ascertain the amount of Normal Profit (i.e. Percentage of Normal Rate of Return on Capital/Average Capital Employed);

(c) Ascertain the Actual Maintainable Profit;

(d) Ascertain the difference between Actual Maintainable Profit minus Normal Profit. If Actual Maintainable Profit is more than the Normal Profit, the excess is called Super-Profit and, in the opposite case, this is no Super-Profit;

(e) Value of Goodwill = Super-Profit x Year’s Purchase.

Illustration 6:

The following particulars are available in respect of the business carried on by Mr. R. N. Mitra:

Compute the value of Goodwill of the business on the basis of 3 years’ purchase of super-profit taking average of last four years.\

Illustration 7:

The following is the Balance Sheet of Mithu Ltd. as on 31.12.2009:

The Assets were revalued as:

Plant and Machinery Rs. 50,000; Land and Building Rs. 40,000; Investments Rs. 25,000; Profit includes Rs. 1,000 income from Investment. Calculate the value of Goodwill on the basis of 3 years’ purchase of Super-profit. Normal rate of return in this type of business is 12%.

Solutions:

Illustration 8:

From the following information, compute the Goodwill of the firm XYZ Co. Ltd. on the basis of four years’ purchase of the average Super-Profit on a 10% yield basis:

Solution:

As per the Articles of Association of this private company, its Directors have declared and paid dividends to its members in the month of December each year out of the profit of the related year. The cost of the Goodwill to the company was Rs. 5, 00,000. Capital employed at the beginning of the year 2006 was Rs. 19, 30,000 including the cost of Goodwill and balance in Profit and Loss Account at the same time was Rs. 60,000.

Value of Goodwill will be four years’ purchase of Average Super-Profit, i.e. Rs. 4,75,833 x 4 = Rs. 19,03,332, or, say, Rs. 19,00,000.

6. Capitalisation of Super-Profit Method:

Under the method, we are to consider super-profit in place of ordinary profit against the normal rate of return.

The same is calculated as:

Value of Goodwill = Super-Profit/Normal Rates of Returns x 100

Illustration 9:

X Ltd. Presented the following information:

Normal Rate of Return @ 10%

Capital Employed Rs. 3,00,000

Profit for last 5 years are Rs. 20,000; Rs. 25,000; Rs. 45,000; Rs. 30,000 and Rs. 50,000

Compute the value of goodwill.

7. Sliding Scale Valuation Method:

Under this method, the distribution of profit which is related to super-profit may vary from year to year. In other words, in order to find out the value of goodwill, sliding scale valuation may be considered relating to super-pr8fits of an enterprise.

Illustration 10:

Compute the value of Goodwill on the basis of Sliding Scale Method.

Amount of Super-Profit estimated at Rs. 12,000.

Sliding Scale:

First Rs, 6,000 for 3 years’ purchase

Next Rs. 4,000 for 2 years’ purchase

Balance Rs. 2,000 for 1 year’s purchase

|

89 videos|52 docs|22 tests

|

FAQs on Methods of Valuation of Goodwill - Valuation of Goodwill & Shares, Advanced Corporate Accounting - Advanced Corporate Accounting - B Com

| 1. What is the meaning of "goodwill" in the context of business valuation? |  |

| 2. What are the different methods used to value goodwill? | |

| 3. How is goodwill different from other intangible assets? | |

| 4. Why is the valuation of goodwill important? | |

| 5. What are some challenges in valuing goodwill? | |

|

7.3K Views |

|

4.84/5 Rating |

|

Nov 16, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Methods of Valuation of Goodwill - Valuation of Goodwill & Shares

,video lectures

,Extra Questions

,shortcuts and tricks

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,Important questions

,Methods of Valuation of Goodwill - Valuation of Goodwill & Shares

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,MCQs

,Methods of Valuation of Goodwill - Valuation of Goodwill & Shares

,Exam

,mock tests for examination

,practice quizzes

,Previous Year Questions with Solutions

,Free

,study material

,Sample Paper

,Semester Notes

,Summary

,Viva Questions

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,past year papers

,Objective type Questions

,ppt

;

Methods of Valuation of Goodwill - Valuation of Goodwill & Shares, Advanced Corporate Accounting Free PDF Download

Importance of Methods of Valuation of Goodwill - Valuation of Goodwill & Shares, Advanced Corporate Accounting

Methods of Valuation of Goodwill - Valuation of Goodwill & Shares, Advanced Corporate Accounting Notes

Methods of Valuation of Goodwill - Valuation of Goodwill & Shares, Advanced Corporate Accounting B Com Questions

Study Methods of Valuation of Goodwill - Valuation of Goodwill & Shares, Advanced Corporate Accounting on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|