Pro - rata Allotment of Shares, Advanced Corporate Accounting | Advanced Corporate Accounting - B Com PDF Download

If the promoters of a company are reputed for their successful promotional successes, the applications are received for more than shares offered under prospectus (over-subscription). They may allot full shares to some of applicants refuse allotment to others, accord partial allotment to someone. This way of allotting shares shows favour to someone and disfavour to others.

Justice in every walk of life needs that the company should also adopt it in making allotment. Instead of showing favour to certain applicants by allotting them full applied shares and disfavour to others by rejecting their applications, the company should treat all the applications of shares at par and allot them shares on pro-rata basis or proportionately. It means that all the applicants have been allotted or refused allotment on proportionate basis. For example: A company issued 60,000 shares, receives applications for 2, 40,000 shares and makes pro-rata allotment.

This will mean that applicants have been allotted 25% of the shares applied. In other words, applicants for 100 shares must have been allotted 25 shares; for 500 shares must have been allotted 125 shares and for 1,000 shares, 250 shares would have been allotted.

Accounting treatment of pro-rata allotment:

In case of pro-rata allotment excess application money received is transferred to share allotment and while receiving allotment money excess application money received is adjusted towards allotment account.

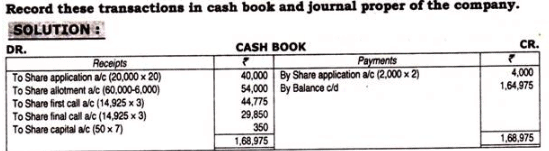

Illustration:

(Pro-rata allotment, forfeiture and reissue).

Tara Tarini Mills Ltd. invited applications for 15,000 equity shares of Rs. 10 each, payable:

On application, Rs.2 per share

On allotment on, Rs.4 per share (including premium)

On first call on, Rs. 3 per share and”

On final call on Rs. 2 per share.

Applications were received for 20,000 shares and directors decided to deal with the 7phcations as:

(a) To refuse allotment to applicants for 2,000 shares.

(b) To allot on 100% basis to applicants for 6,000 shares.

(c) To allot the remaining shares among remaining applicants on pro-rata basis

(d) To adjust the surplus applications money against the amount due on allotment. Whole of the money was received except two calls on 75 shares, which were forfeited. Out of these 50 shares were re-issued at Rs.7 per share.

|

89 videos|52 docs|22 tests

|

FAQs on Pro - rata Allotment of Shares, Advanced Corporate Accounting - Advanced Corporate Accounting - B Com

| 1. What is pro-rata allotment of shares? |  |

| 2. What is the purpose of pro-rata allotment of shares? | |

| 3. What is the difference between pro-rata allotment and rights issue? | |

| 4. How is the price of pro-rata allotment of shares determined? | |

| 5. What happens if a shareholder does not exercise their right of pro-rata allotment? | |

|

9.6K Views |

|

4.75/5 Rating |

|

Dec 23, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Pro - rata Allotment of Shares

,Summary

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,mock tests for examination

,shortcuts and tricks

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,Pro - rata Allotment of Shares

,study material

,Extra Questions

,Sample Paper

,Viva Questions

,video lectures

,Pro - rata Allotment of Shares

,Exam

,Previous Year Questions with Solutions

,Objective type Questions

,Free

,MCQs

,practice quizzes

,Semester Notes

,past year papers

,Important questions

,ppt

,Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

;

Pro - rata Allotment of Shares, Advanced Corporate Accounting Free PDF Download

Importance of Pro - rata Allotment of Shares, Advanced Corporate Accounting

Pro - rata Allotment of Shares, Advanced Corporate Accounting Notes

Pro - rata Allotment of Shares, Advanced Corporate Accounting B Com Questions

Study Pro - rata Allotment of Shares, Advanced Corporate Accounting on the App

|

© EduRev

|

Education Revolution

|

|