Bonus Shares: Meaning, Advantages and Disadvantages - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com PDF Download

Meaning of Bonus Shares:

Sometimes a company cannot pay dividend in cash due to shortage of liquid funds, viz., cash, in spite of earning a large amount of profit for a particular period. Under the circumstances, the company issues new shares to the existing shareholders in lieu of paying dividend in cash.

These shares are known as ‘Bonus Shares’. Such bonus shares are to be offered to the existing shareholders in proportion to the shareholdings and dividend rights. Generally, the company issues bonus shares out of profits and/ or reserve to the existing shareholders.

Since the profit/reserve is being capitalized, it is also called capitalisation of profit/reserve. As the company cannot receive cash from the shareholders for the purpose of issuing bonus shares, a sum equal to the total value of bonus issue is to be adjusted against profit/reserve and transferred to Equity Share Capital Account.

Companies Act and Bonus Issue:

According to the provisions of the Companies Act, 1956, a bonus issue can be made when the following conditions are satisfied:

i. When the Articles of Association of a company permit such issue;

ii. When the company has sufficient undistributed profits;

iii. When the proposal of the Board of Directors about such bonus issue has been approved by the shareholders in the general meeting;

iv. When the necessary consent has been obtained from the Controller of Capital Issues.

Advantages of Issuing Bonus Shares:

A. From the company’s view point:

(a) By issuing bonus shares shareholders are to be satisfied when the company cannot pay dividend in cash due to shortage of liquid funds, i.e., profit can be distributed without distributing the liquid resources, viz., cash.

(b) By issuing bonus shares shareholders are to be satisfied particularly when the company does not prefer to pay dividend in cash for the purpose of either its extension or its working capital or any other specific purposes.

(c) Sometimes a company is bound to reduce its reserve for the interest of its own. It may so happen that the amount of earning profit exceeds the amount of total paid up capital of the company which, in other words, encourages the competitors and creates unhealthy relationship between workers and the company.

B. From the shareholder’s view point:

(a) Shareholders need not pay tax on the bonus shares but they are to pay them on the dividend so received in cash.

(b) Shareholders, if they so desire, can convert the shares into cash by disposing of the same at a higher price.

(c) If partly paid shares are converted into fully paid by issuing bonus, the shareholders need not pay a further sum for the purpose. On the other hand, their shares become fully paid up.

Disadvantages of issuing Bonus Shares:

(a) If the rate of dividend fluctuates, i.e., cannot be maintained, the market value of shares may go down.

(b) If the rate of profit is not increased, the rate of dividend may be decreased.

(c) It encourages speculation which is not desirable.

Revised Directives of Central Government for the Issue of Bonus Shares:

All applications for bonus issue should be signed by a person not below the rank of director or secretary along with a certificate which will indicate that the information furnished is true and correct and necessary data required in the application form and guidelines, have been duly complied with.

An auditor’s certificate should be annexed to the application which will indicate that the guidelines for the issue of bonus shares prescribed by the government are fully met and the data that are furnished in the application is true and correct to the best of his knowledge.

The directives of the Central Government by Capital Issues Control Act, 1947 for the purpose of issuing bonus shares are:

1. There should be a provision in the Articles of Association regarding bonus issue. If not, a copy of the resolution passed at the general body meeting in order to make the proper change of the Articles of Association should be produced.

2. If the subscribed capital and paid up capital exceeds the amount of authorised capital by the subsequent issue of bonus shares, a resolution should be passed at the general body meeting to increase the amount of authorised capital, if necessary.

3. A resolution passed at the general body meeting for bonus issue should be furnished before an application is made to the controller of capital issue. At the same time, the directors’ intention regarding the rate of dividend to be declared in the year immediately after the bonus issue should also be mentioned.

4. Free reserves created out of real profits and share premium collected in cash may be utilised for the purpose of issuing bonus shares.

5. Reserve created by the revaluation of fixed assets is not permitted to be utilised for the purpose.

6. Development Rebate Reserve or Investment Allowance Reserve may be considered as free reserve and hence, may be capitalized.

7. The residual reserves after bonus issue should be at least 40% of the increased paid-up capital.

8. Capital Redemption Reserve, if any, for the computation of the said 40% of the residual reserve, is not to be taken into consideration.

9. Contingent liabilities which may have a bearing on net profits shall be turned into consideration for the calculation of minimum residual reserve of 40%.

10. 30% of the average profits (before tax but after providing preference dividend) for the previous 3 years should at least yield a dividend of 10% on the expanded equity capital.

11. Declaration of bonus issue in lieu of dividend is not permitted.

12. Further application for issue of bonus shares may be made only after 36 months from the date of an earlier bonus issue.

13. Unless the partly paid shares are made fully paid, bonus issues are not permitted.

14. If it is found that the company has defaulted the payment of statutory dues of the employees, e.g., contribution of P.F., bonus shares, in this case, is not permitted.

15. Capital Reserve which is created out of revaluation of assets without accrual of cash resources will neither be allowed to be capitalized (nor will it be allowed to be taken into consideration) for the computation of the said residual reserve of 40%.

16. At any one time, total amount of bonus issue out of free reserves shall not exceed the total amount of paid-up equity capital.

17. If the application is made both for the purpose of issuing bonus shares and right shares at the same time, permission should be given first f’- bonus issue and later for right issue.

18. An auditor’s certificate should be furnished stating that proper depreciation has been provided as per Income-tax Act.

Quantum of Bonus Issues Share:

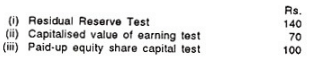

According to the above guidelines, the maximum amount of bonus issue at one time may be the least of the amount after considering the following three conditions, i.e., the least of the following should be considered:

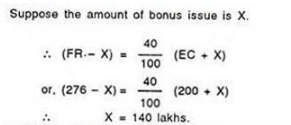

(i) Residual Reserve Test:

It means the residual reserve, after the bonus issue, should at least be 40% of the increased paid-up capital.

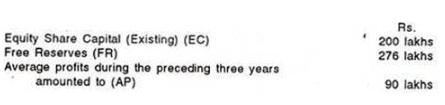

Consider the following illustration which will make the principle clear:

Illustration:

Considering the following data, ascertain the maximum permissible amount of bonus issue after applying the ‘residual Reserve Test’.

Solution:

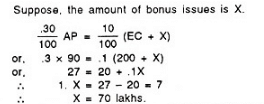

(ii) Capitalised value of earning test:

Assuming that 30% of the average profit before tax should yield a rate of dividend on the expanded capital base of the company is 10%.

Illustration 2:

Ascertain the maximum permissible amounts of bonus issue after applying ‘Capitalized value of earning test’ from the following data:

Solution:

(ii) Paid-up equity share capital test:

The bonus issue out of free reserve at any one time shall not exceed the amount of equity share capital (paid-up) of the company.

Thus, the maximum permissible amount of bonus issue, after considering the data contained in the above illustration, will be the least of the following:

Since, Rs. 70 lakhs is the smallest one, maximum amount of bonus issue can be issued to that extent only.

|

89 videos|52 docs|22 tests

|

FAQs on Bonus Shares: Meaning, Advantages and Disadvantages - Advanced Corporate Accounting - Advanced Corporate Accounting - B Com

| 1. What is the meaning of bonus shares? |  |

| 2. What are the advantages of bonus shares? | |

| 3. What are the disadvantages of bonus shares? | |

| 4. How are bonus shares different from regular shares? | |

| 5. How are bonus shares accounted for in a company's financial statements? | |

|

2K Views |

|

4.94/5 Rating |

|

Dec 23, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Objective type Questions

,Extra Questions

,video lectures

,Advantages and Disadvantages - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,shortcuts and tricks

,Bonus Shares: Meaning

,Free

,Important questions

,mock tests for examination

,MCQs

,Semester Notes

,study material

,Bonus Shares: Meaning

,Bonus Shares: Meaning

,Previous Year Questions with Solutions

,past year papers

,Advantages and Disadvantages - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,Advantages and Disadvantages - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,ppt

,Summary

,practice quizzes

,Viva Questions

,Exam

,Sample Paper

;

Bonus Shares: Meaning, Advantages and Disadvantages - Advanced Corporate Accounting Free PDF Download

Importance of Bonus Shares: Meaning, Advantages and Disadvantages - Advanced Corporate Accounting

Bonus Shares: Meaning, Advantages and Disadvantages - Advanced Corporate Accounting Notes

Bonus Shares: Meaning, Advantages and Disadvantages - Advanced Corporate Accounting B Com Questions

Study Bonus Shares: Meaning, Advantages and Disadvantages - Advanced Corporate Accounting on the App

|

© EduRev

|

Education Revolution

|

|