Classification and Importance of Cost of Capital - Accountancy and Financial Management | Accountancy and Financial Management - B Com PDF Download

Classification of Cost of Capital

Cost of capital may be classified into the following types on the basis of nature and usage:

- Explicit and Implicit Cost.

- Average and Marginal Cost.

- Historical and Future Cost.

- Specific and Combined Cost.

Explicit and Implicit Cost

The cost of capital may be explicit or implicit cost on the basis of the computation of cost of capital.

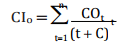

Explicit cost is the rate that the firm pays to procure financing. This may be calculated with the help of the following equation;

Where,

CIo=initialcashinflow

C = outflow in the period concerned

N=duration forwhich the funds are provided

T = tax rate

Implicit cost is the rate of return associated with the best investment opportunity for the firm and its shareholders that will be forgone if the projects presently under consideration by the firm were accepted.

Average and Marginal Cost

Average cost of capital is the weighted average cost of each component of capital employed by the company. It considers weighted average cost of all kinds of financing such as equity, debt, retained earnings etc.

Marginal cost is the weighted average cost of new finance raised by the company. It is the additional cost of capital when the company goes for further raising of finance.

Historical and Future Cost

Historical cost is the cost which as already been incurred for financing a particular project. It is based on the actual cost incurred in the previous project.

Future cost is the expected cost of financing in the proposed project. Expected cost is calculated on the basis of previous experience

Specific and Combine Cost

The cost of each sources of capital such as equity, debt, retained earnings and loans is called as specific cost of capital. It is very useful to determine the each and every specific source of capital.

The composite or combined cost of capital is the combination of all sources of capital. It is also called as overall cost of capital. It is used to understand the total cost associated with the total finance of the firm.

Importance of Cost of Capital

Computation of cost of capital is a very important part of the financial management to decide the capital structure of the business concern.

Importance to Capital Budgeting Decision

Capital budget decision largely depends on the cost of capital of each source. According to net present value method, present value of cash inflow must be more than the present value of cash outflow. Hence, cost of capital is used to capital budgeting decision.

Importance to Structure Decision

Capital structure is the mix or proportion of the different kinds of long term securities. A firm uses particular type of sources if the cost of capital is suitable. Hence, cost of capital helps to take decision regarding structure.

Importance to Evolution of Financial Performance

Cost of capital is one of the important determine which affects the capital budgeting, capital structure and value of the firm. Hence, it helps to evaluate the financial performance of the firm.

Importance to Other Financial Decisions

Apart from the above points, cost of capital is also used in some other areas such as, market value of share, earning capacity of securities etc. hence, it plays a major part in the financial management.

|

44 videos|75 docs|18 tests

|

FAQs on Classification and Importance of Cost of Capital - Accountancy and Financial Management - Accountancy and Financial Management - B Com

| 1. What is the meaning of cost of capital in accountancy and financial management? |  |

| 2. How is the cost of capital classified in accountancy and financial management? | |

| 3. Why is the cost of capital important in accountancy and financial management? | |

| 4. How is the cost of capital calculated in accountancy and financial management? | |

| 5. How does the cost of capital affect a company's financial performance? | |

|

4.94/5 Rating |

|

Dec 23, 2024 Last updated |

|

44 videos|75 docs|18 tests

|

|

Explore Courses for B Com exam

|

|

practice quizzes

,Classification and Importance of Cost of Capital - Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Extra Questions

,ppt

,Classification and Importance of Cost of Capital - Accountancy and Financial Management | Accountancy and Financial Management - B Com

,video lectures

,MCQs

,Previous Year Questions with Solutions

,Semester Notes

,Free

,Classification and Importance of Cost of Capital - Accountancy and Financial Management | Accountancy and Financial Management - B Com

,shortcuts and tricks

,Objective type Questions

,Summary

,mock tests for examination

,past year papers

,Viva Questions

,Sample Paper

,Important questions

,study material

,Exam

;

Classification and Importance of Cost of Capital - Accountancy and Financial Management Free PDF Download

Classification and Importance of Cost of Capital - Accountancy and Financial Management

Classification and Importance of Cost of Capital - Accountancy and Financial Management Notes

Classification and Importance of Cost of Capital - Accountancy and Financial Management B Com Questions

Study Classification and Importance of Cost of Capital - Accountancy and Financial Management on the App

|

© EduRev

|

Education Revolution

|

|